Download

1 / 56

560 likes | 711 Views

Reform of the banking system in 1995.

E N D

Reform of the banking system in 1995 The restructuring of the banking system in China has been an important step in dismantling the old State command economic system and creating a new market-driven economic system. The former State-owned banks which once acted merely as branches of the People’s Bank of China have now been transformed into commercial banks, with the People’s Bank of China acting as the central monetary authority.

Reform of the banking system in 1995 In 1995 the National People’s Congress passed the Central Bank Law. People’s Bank of China became independent in the implementation of monetary policies and would be free from the interference of local governments, departments and individuals. The Bank is under the leadership of the State Council and reports to the Standing Committee of the National People’s Congress on the monetary policy and financial management affairs.

Reform of the banking system in 1995 The Commercial Banking Law came into effect on 1 July 1995 which brought reforms on the banking system of China. The state-owned specialized banks would move towards commercialisation, so that from policy lending to commercial lending. The Bank of China, Industrial and Commercial Bank of China, Agricultural Bank of China and People’s Construction Bank of China became state-owned commercial banks and would be allowed to turn down credit extension or the issue of guarantees so as to restructure asset quality, improve accounting systems and set up internal risk management.

Reform of the banking system in 1995 The aim of the restructuring is to establish under the leadership of the State Council : 1.a macro-regulatory and control system under the central bank which is independent in implementing monetary policy; 2.a banking structure characterized by a separation of policy implementing banks from commercial banks; 3.State-owned banks as the mainstay and coexisting with the numerous banking institutions; and 4.a unified, open, orderly yet competitive monetary market system under strict administration.

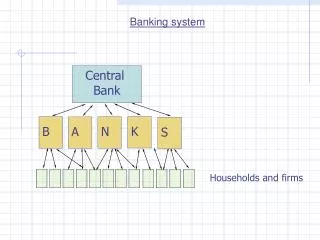

Banking System of the People’s Republic of China People’s Bank of China Policy Banks (3) State-owned Commercial Banks (4) National Shareholding Commercial Banks (6) Regional Shareholding Commercial Banks (4) City Credit Cooperatives (2,800) Rural Credit Cooperatives (41,755) Foreign Banks (177) City Shareholding Commercial Banks (90)

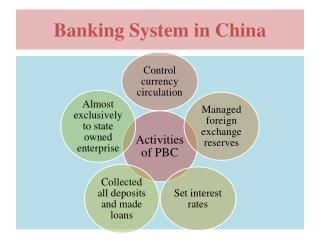

People’s Bank of China’s Central Bank Functions • To formulate and implement monetary policies, and promulgate regulations on financial business; • To issue Renminbi and control its circulation; • To propose the annual supply of banknotes, interest rates and foreign exchange rate for the approval by the State Council; • To hold and manage the state foreign exchange and gold reserves; • To examine, approve and supervise the banking institutions in China;

People’s Bank of China’s Central Bank Functions • To manage the state treasury; • To supervise and control the financial markets in China; • To engage in international banking operations in its capacity as the central bank of the country; • To maintain normal operation of the payment and settlement systems; and • To conduct research and forecast for the banking industry.

State-owned Policy banks In 1994, three State-owned policy banks were established to take over the policy loan obligations, thus leaving the retail side of the business in the hands of the commercial banks. They are subject to the supervision of the People’s Bank of China in their operations. However, they are responsible for risks on their own, operate on a no-profit no-loss basis and do not compete with commercial banks. The policy lending that they provide is made at the request of or strongly encouraged by the government to promote its economic, industrial and sectoral policies and to assure funding for priority activities.

State-owned Policy banks The State Development Bank would concentrate on financing large-scale infrastructure projects, the choice of which would be determined jointly by the Bank and the State Planning Commission. It also administers the China Construction Bank and some State-owned investment institutions.

State-owned Policy banks The Agricultural Development Bank’s key function would be to take over the policy loans of the Agricultural Bank of China, lend support to State purchases of foodstuffs and transfer budgetary funds for agricultural support and social improvements in rural areas.

State-owned Policy banks The Import and Export Credit Bank of China would assist Chinese trade corporations through the provision of import and export credits, insurance and credit guarantees. The bank would provide credit loans to buyers for the importation and to sellers for the exportation of complete plants of machinery and electrical equipment. The bank would also initially be underwritten by the State and would be able to raise funds through domestic and foreign borrowing.

Big Four State-owned Commercial Banks (previously called State-owned Specialized Banks) Bank of China was once an international banking arm of China with branches and representative offices throughout the world. It was a state-owned bank specializing in foreign exchange and foreign trade.

Big Four State-owned Commercial Banks The Industrial and Commercial Bank of China was set up in 1984 to cater for commercial and industrial development in the urban areas. It offered deposit accounts to urban households and finance for projects development.

Big Four State-owned Commercial Banks Agricultural Bank of China specialized in providing finance for the agricultural sector and rural development.

Big Four State-owned Commercial Banks People’s Construction Bank of China (now called China Construction Bank) specialized in providing finance for fixed asset investment and capital construction by the State. In 1994, it acquired 40% stake of the Hong Kong Industrial and Commercial Bank and gained access to the Hong Kong financial market.

Assets Distribution of the Financial Institutions in the Year 2000

National, Regional and City Shareholding Commercial Banks There are 6 national commercial banks and their largest shareholder is the central government. • Bank of Communications • CITIC Industrial Bank • China Everbright Bank • China Merchants Bank • China Mingshen Bank • Huaxia Bank

National, Regional and City Shareholding Commercial Banks • There are 4 regional commercial banks and their largest shareholders are the provincial or municipal governments. • Shenzhen Development Bank • Shanghai Pudong Development Bank • Guangdong Development Bank • Fujian Industrial Bank

National, Regional and City Shareholding Commercial Banks • There are 90 city commercial banks, e.g. Bank of Shanghai, Beijing Commercial Bank, Shenzhen Commercial Bank, etc. and their largest shareholders are usually the city governments.

Market Share of Banks in China at the end of 1999 (RMB billion)

Market Share of Banks in China at the end of 1999 (RMB billion)

Foreign banks At the end of the Year 2000, there were 177 foreign banks in China, which had established 155 branches and 429 representative offices. Geographically foreign banks are concentrated in developed coastal cities like Shenzhen, Shanghai and Beijing.

Foreign banks Since 1999, the People’s Bank of China opened up the Renminbi businesses to foreign banks in China. Currently 32 foreign banks in Shanghai and Shenzhen have been granted the license to conduct RMB businesses.

Foreign banks However, foreign banks still face both heavy entry barriers and hefty business restrictions in China. As a result, the market share of foreign banks in China in terms of total financial assets is below 2%. Although foreign banks enjoy a 15% income tax rate as compared to 33% for Chinese banks.

The Impact of WTO Entry on China’s Banking Sector The Sino-US WTO Agreement stipulates that foreign banks will be allowed to conduct all the banking businesses in China, in both RMB and foreign currencies, with both corporate and resident customers, for both Chinese entities and foreign entities, and in any place of the country, 5 years after China’s WTO entry.

The Impact of WTO Entry on China’s Banking Sector This will be phased in by two major steps: the opening-up of corporate banking business in RMB with Chinese enterprises in 2 years, and the opening-up of consumer banking business with Chinese residents in both RMB and foreign currencies in 5 years.

The Impact of WTO Entry on China’s Banking Sector Geographic restriction for foreign banks on RMB business will be phased out as follows: Upon WTO entry, Tianjin and Dalian; 1 year after entry, Guangzhou, Qingdao, Nanjing and Wuhan; 2 year after entry, Jinan, Fuzhou, Chengzhou and Chongqing; 3 year after entry, Kunming, Zhuhai, Beijing and Xiamen; 4 year after entry, Shantou, Ningbo, Shenyang and Xian; 5 year after entry, there will be no geographic restriction.

Closer Economic Partnership Arrangement between Hong Kong and the Mainland (CEPA) In addition to the mainland's WTO liberalisation meansures, Hong Kong's banking sector is one of those that would benefit significantly under CEPA. Under CEPA, n A Hong Kong bank needs to have total assets of over US$ 6 billion to establish a branch on the Mainland. n Removes requirement for setting up representative office before establishing a joint-venture bank. Lower requirements for conducting RMB business:

Closer Economic Partnership Arrangement between Hong Kong and the Mainland (CEPA) • Reduced minimum requirement for prior business operation on the Mainland to 2 years; • Profitability assessment is made on basis of overall position of all branches instead of individual branch.

Closer Economic Partnership Arrangement between Hong Kong and the Mainland (CEPA) • Under CEPA, Hong Kong banks will be allowed to open a branch on the Mainland if they have total assets of US$ 6 billion or more, significantly lower than the entrance requirement under WTO commitments. This will effectively allow almost all eight medium size Hong Kong banks to enter the Mainland market, and for those who have already had branches, to expand their network nationwide.

Closer Economic Partnership Arrangement between Hong Kong and the Mainland (CEPA) • The easing of restrictions for operation of RMB business benefits not only Hong Kong newcomers to the Mainland market, but also the Hong Kong banks that have already operated on the Mainland to have better access to RMB business. As of end-May 2004, five Hong Kong banks had obtained Hong Kong Service Suppliers certificates.

Closer Economic Partnership Arrangement between Hong Kong and the Mainland (CEPA) • CEPA not only opens the Mainland door for Hong Kong's medium size banks, its "Financial Services Cooperation" provisions may also bring significant benefits to Hong Kong's status as an international banking centre. Mainland banks are encouraged to relocate their international treasury and foreign exchange trading centres to Hong Kong and to develop networks in Hong Kong through acquisition.

Explain the importance of the 1995 Banking Reform The 1995 Banking Reform was an important step to restructure the banking system in China for moving into a market-driven economic system. The state-owned banks would be transformed into commercial banks and the People’s Bank of China would rectify its roles as the central bank.

Explain the importance of the 1995 Banking Reform In 1995 the National People’s Congress passed the Central Bank Law. People’s Bank of China became independent in the implementation of monetary policies and would be free from the interference of local governments, departments and individuals. The Bank is under the leadership of the State Council and reports to the Standing Committee of the National People’s Congress on the monetary policy and financial management affairs.

Explain the importance of the 1995 Banking Reform The Commercial Banking Law came into effect on 1 July 1995 which brought reforms on the banking system of China. The state-owned specialized banks would move towards commercialisation, so that from policy lending to commercial lending. The Bank of China, Industrial and Commercial Bank of China, Agricultural Bank of China and People’s Construction Bank of China became state-owned commercial banks and would be allowed to turn down credit extension or the issue of guarantees so as to restructure asset quality, improve accounting systems and set up internal risk management.

Describe the functions of the PBOC as the central bank • To formulate and implement monetary policies, and promulgate regulations on financial business; • To issue Renminbi and control its circulation; • To propose the annual supply of banknotes, interest rates and foreign exchange rate for the approval by the State Council; • To hold and manage the state foreign exchange and gold reserves; • To examine, approve and supervise the banking institutions in China;

Describe the functions of the PBOC as the central bank • To manage the state treasury; • To supervise and control the financial markets in China; • To engage in international banking operations in its capacity as the central bank of the country; • To maintain normal operation of the payment and settlement systems; and • To conduct research and forecast for the banking industry.

Distinguish between state-owned policy banks and commercial banks Three state-owned policy banks were established in 1994 to take over the policy lending obligations of the state-owned commercial banks, so that the big-four state-owned commercial banks could Concentrate on the retail side of their business. The policy banks are responsible for their own risks, operate on a no-profit-no-loss basis and do not compete with the commercial banks. They obtain funds from the government or by issuing securities. The policy lending is made at the request of the government to promote its economic, industrial and sectoral policies and to assure funding for priority activities.

Distinguish between state-owned policy banks and commercial banks The State Development Bank would concentrate on financing large-scale infrastructure projects, the choice of which would be determined jointly by the Bank and the State Planning Commission. It also administers the China Construction Bank and some State-owned investment institutions.

Distinguish between state-owned policy banks and commercial banks The Agricultural Development Bank’s key function would be to take over the policy loans of the Agricultural Bank of China, lend support to State purchases of foodstuffs and transfer budgetary funds for agricultural support and social improvements in rural areas.

Distinguish between state-owned policy banks and commercial banks The Import and Export Credit Bank of China would assist Chinese trade corporations through the provision of import and export credits, insurance and credit guarantees. The bank would provide credit loans to buyers for the importation and to sellers for the exportation of complete plants of machinery and electrical equipment. The bank would also initially be underwritten by the State and would be able to raise funds through domestic and foreign borrowing.

Distinguish between state-owned policy banks and commercial banks The state-owned commercial banks were previously the state-owned specialized banks. Bank of China was once an international banking arm of China with branches and representative offices throughout the world. It was a state-owned bank specializing in foreign exchange and foreign trade.

Distinguish between state-owned policy banks and commercial banks The Industrial and Commercial Bank of China was set up in 1984 to cater for commercial and industrial development in the urban areas. It offered deposit accounts to urban households and finance for projects development. Agricultural Bank of China specialized in providing finance for the agricultural sector and rural development.

Distinguish between state-owned policy banks and commercial banks People’s Construction Bank of China (now called China Construction Bank) specialized in providing finance for fixed asset investment and capital construction by the State. In 1994, it acquired 40% stake of the Hong Kong Industrial and Commercial Bank and gained access to the Hong Kong financial market.

Why did foreign banks in China capture only a small market share ? Foreign banks in China captured only a small market share because they were only allowed to conduct foreign currency banking business. Since 1999, the PBOC opened up the Renminbi businesses to foreign banks and up to now 32 foreign banks in Shanghai and Shenzhen have been granted the license to conduct RMB businesses.

Why did foreign banks in China capture only a small market share ? However, foreign banks still face both heavy entry barriers and hefty business restrictions in China. As a result, the market share of foreign banks in China in terms of total financial assets is below 2%. Although foreign banks enjoy a 15% income tax rate as compared to 33% for Chinese banks.

The impact of China’s WTO entry on foreign banks’ development in China The Sino-US WTO Agreement stipulates that foreign banks will be allowed to conduct all the banking businesses in China, in both RMB and foreign currencies, with both corporate and resident customers, for both Chinese entities and foreign entities, and in any place of the country, 5 years after China’s WTO entry. This will be phased in by two major steps: the opening-up of corporate banking business in RMB with Chinese enterprises in 2 years, and the opening-up of consumer banking business with Chinese residents in both RMB and foreign currencies in 5 years.

The impact of China’s WTO entry on foreign banks’ development in China Geographic restriction for foreign banks on RMB business will be phased out as follows: Upon WTO entry, Tianjin and Dalian; 1 year after entry, Guangzhou, Qingdao, Nanjing and Wuhan; 2 year after entry, Jinan, Fuzhou, Chengzhou and Chongqing; 3 year after entry, Kunming, Zhuhai, Beijing and Xiamen; 4 year after entry, Shantou, Ningbo, Shenyang and Xian; 5 year after entry, there will be no geographic restriction.