Download

1 / 18

180 likes | 201 Views

Explore the fundamental concepts of production and cost in the short run, including efficiency, input types, and cost analysis. Learn about factors affecting production and the various costs involved in business operations.

E N D

Theory of Firms • Production and cost in the Short Run.

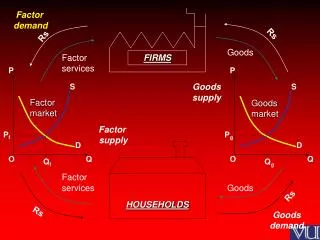

Production and Cost in the Short Run • What is production???? • What is a production function????? • What is technical efficiency????

Production and Cost in the Short Run • What is technical efficiency???? • What is economic efficiency???? • What is variable input????

Production and Cost in the Short Run • What is fixed input???? • What is quasi-fixed input???? • What is short run????

Production and Cost in the Short Run • What is long run???? • What is planning horizon???? • What is variable proportions production????

Production and Cost in the Short Run • What is fixed proportions production???? Q = f(L,K) • What is average product of labor???? • What is average marginal of labor????

Theory of Firms • Profit: • Difference between Revenue and Cost Π = TR - TC

Theory of Firms • Revenue = amount received from the sale of goods or services TR = P x Q

Theory of Firms • Total Cost is the sum of all costs – fixed, variable and semi-fixed • Fixed Costs– do NOT depend on quantity produced- Rent, Rates, Insurance, etc. • Variable Costs–vary directly with the amount produced – raw materials • Semi–Fixed Costs - may vary with output but not directly – some types of labour, energy costs

Theory of Firms • Factor Costs: • Labour– wages/salaries • Land– rent • Capital– interest • Enterprise - profit

Theory of Firms • Average Cost = Total cost divided by the number of units produced AC = TC/Q AVC = TVC/Q AFC = TFC/Q

Theory of Firms • Marginal Cost • The cost of producing one extra or one less unit of output MC = TCn units – TCn-1 / Q • If TC of 100 units = £500 and TC of producing 101 units is £505, MC = £5.00 • Important concept

Theory of Firms • Short and Long run: • Short run–some factors fixed and cannot be increased/reduced • Long Run– time taken to vary all factors of production • Short and long run vary in all industries:

Theory of Firms • Railways– short run –’easy’ to increase labour, long lead times for new rolling stock – 5 years? • Supermarkets– short run – can buy new shelving, hire staff, etc but opening of new stores takes several years • Local Builder– short run buys new tools, hires assistant; long run – purchasing a new van – a couple of months?

Theory of Firms • Diminishing Marginal Returns • Assumptions – some factors fixed (e.g. capital and land) • Adding variable factor – (labour) • Total Product • Average Product – TP / Q variable factor (Qv) • Marginal Product ΔTP/ΔQv

Theory of Firms • Increasing the variable factor: • TP rises at first, slows then falls • AP rises at first then starts to fall • MP rises, then falls, cuts AP at highest point of AP, cuts horizontal axis at point where TP starts to fall

Theory of Firms Objectives of firms: • Profit maximisation • Profit satisficing • Long term survival • Share price maximisation • Revenue maximisation • Brand loyalty • Expansion and market dominance

Theory of Firms • Profit: • Difference between Revenue and Cost Π = TR - TC