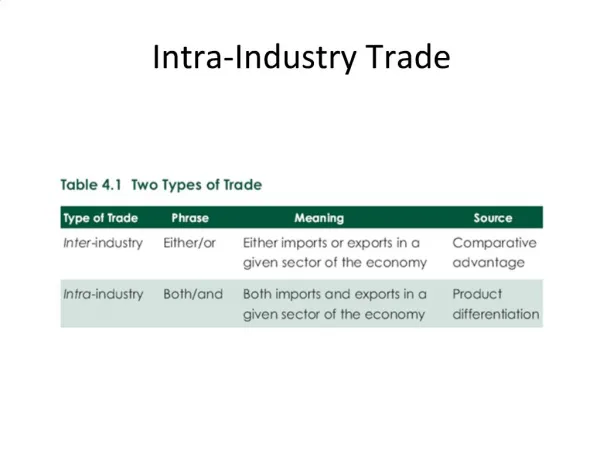

Download

1 / 26

260 likes | 278 Views

Portfolio Committee for Trade & Industry. National Credit Regulator Strategic Plans & Budgets. Mandate & Funding Strategic Focus & Challenges High level overview of operational performance since establishment Strategic objectives Budget allocation Challenges & risks. CHAIR COO CEO.

E N D

Portfolio Committee for Trade & Industry National Credit Regulator Strategic Plans & Budgets

Mandate & Funding Strategic Focus & Challenges High level overview of operational performance since establishment Strategic objectives Budget allocation Challenges & risks CHAIR COO CEO Structure of presentation …

Mandate & funding • NCR mandate Relevant sections of the Act:- • S13: Promote & support the development of a transparent, fair, efficient & accessible credit market • S14: Registration of Credit Providers, Credit Bureaus & Debt Counsellors • S15: Enforce the Act • S16: Through research, audits, monitoring & information dissemination, increase knowledge of the consumer credit market

Chair: Adv. P. Tlakula Deputy Chair: M Setiloane Designated Members S. Luka (Social Development) N. Mashiya (Finance) A. Osman (Housing) F. Sibanda (Trade and Industry) Other Members Y. Radinku C. Glover M. Maleka M. van Schalkwyk T. Store Committees (& chairpersons) Remuneration committee (C. Glover) Policy & strategy committee (Y. Radinku) Audit & risk committee (T. Ramano) (independent) Board of Directors … Board & Committees fully functional

Strategic progress, challenge Progress : registration, enforcement, consumer education, implementation of debt counselling, credit bureaus & statistics, all sound progress; Major achievements: effective action against Rudco Finance; publication of 1st credit bureau statistics; progress in registration of credit providers COO will provide further detail

Challenges • Debt counselling a major challenge … focus on (a) cooperation between debt counsellors & credit providers, (b) ongoing training, support and advice, (c) monitoring flow of cases to identify blockages & intervene where necessary • Lack of certainty on fees and on court processes a major weakness • Capacity & funding constraints … NCR has a huge task and have performed admirably, given the size of its staff complement and its budget As a Board, we are making every effort to support the NCR in the achievement of its mandate, and in giving guidance where required

Nomsa MotshegareChief Operations Officer High level overview of operational performance since establishment

Registration … Credit Providers • From 4230 applications, registration of 2340 entities with 26,440 registration certificates (branches) finalised • 1186 still temporary registered and 420 applications rejected Credit Bureaus • From 16 applications, 11 registered, including pre-registration inspection on each applicant) Debt Counsellors • From 516 applications, 287 registered, remainder in different stages of processing; Consistent inflow of new applications

Complaints & investigations Calls & complaints • 111,300 calls in the 11 months to Feb’08, of which 1,415 complaints Investigations • 213 investigations since June 2006, e.g. • Exemption Notice / Usury Act; Market Conduct; Marketing & Advertising; Pre-agreement Statements & Quotations; Credit Bureaus; Debt Counsellors Enforcement action • Balance adjustments and refunds to borrowers of approx R2m since Apr’07 • 20 Compliance Notices; 2 Referrals to Tribunal; action on Rudco Finance (Pty) Ltd Moneyweb:- NCR clobbers Rudco The credit regulator says Rudco contravened a number of provisions of the credit act.

Education & stakeholder communication April ’07 to Feb’08:- • 460 workshops aimed at industry, community, & employers, in which 39,630 people participated • Media exposure valued at R45m (AVE), 40 TV interviews, 298 radio interviews • 3 booklets for registrants, brochure on S73, explanatory booklet on Act (all official languages) • 660,507 “hits” on the NCR website

NCR publications … in all official languages, available on www.ncr.org.za

Statistics • NCR published first statistics from credit bureau reports (as at Sept’2007):- • 16.9m credit active consumers • 62% = 10.5m “in good standing” • 3 accounts per consumer • overall credit worthiness slightly down between June & Sept’07, with middle income consumers most affected, enquiries 23% down • more than 6 million consumers benefited from S73 data cleansing • Credit provider returns being processed

Gabriel DavelChief Executive Officer Strategic objectives, targets, budget allocation Challenges & risks

Budgeted operational expenditure: 2008/09 • Expenditure of R77m, up by 2% on 2007/08 budget (R75m), and up by 36% on 2007/08 actual expenditure (R56m) • Re budget surplus in 2007/08, note that NCR still in establishment phase, thus not able to spend at budgeted levels (e.g. staff still below desired level) • Specific items • Personnel the biggest expense; • Debt counselling re creating of sufficient capacity, supporting infrastructure; covering the cost of low income consumers • Professional fees include cost of external investigators & legal fees – including provision for potential legal challenges

Operational expenditure per department – 2008/09 • Debt counselling support single biggest item (18%), followed by consumer education & stakeholder awareness (14%) • Executive includes CEO, COO, legal support & professional fees • Most of debt counselling support is external payments, to develop supporting infrastructure & to cover debt counselling cost for low income consumers

Budgets revisions were required to respond to (a) registration fees falling short of expectations (R5m pa), and reduction in funding from DTI (R7m pa) Until 2008/2009 the impact mitigated by draw-downs from MFRC reserves. However, MFRC transfer of R19.8 million will be depleted by 2009/2010 This impacts upon all items of a “variable nature”, (a) investigations, (b) consumer education, (c) debt counselling support, (d) legal & professional fees, (e) research Over the next 2 years we will make every attempt to secure further funding in order to prevent a reduction in funding in these critical areas Funding & budget revisions

Challenges & risks • Debt counselling Volumes expected to grow substantially, thus critical that magistrates court problems be addressed & fee regulations finalised. Also, to provide ongoing training & support; effective engagement with credit providers and to implement appropriate supporting infrastructure, in particular regarding payment distribution. Failure would undermine credibility of Act & leave over-indebted consumers without any escape. • Enforcement Potential contraventions include dazzling array of matters: pre-agreement disclosure; direct marketing; credit bureau information; contraventions on interest & fee limitations (micro-lending), credit life insurance, ‘bond origination’, mortgage re-financing and others. Also a number of ‘fraudulent schemes’. High risk that a ‘scheme’ would slip through the cracks and extreme need to prioritize. • Funding The current level of funding places significant constraints on the NCR’s capacity to deal with the demands that it is facing.

Conclusion • NCR has already had a significant impact in the short time since its establishment • The reckless credit (and related) conditions are even receiving international attention, as an innovative approach of preventing the types of crises such as the ‘sub-prime mortgage crisis’ in the US • There are indications of positive changes in the credit market and of increasing levels of competition, due mainly to the standardised disclosure having an impact, and to the changes in respect of credit life insurance and other charges • Visible, pro-active inspections & enforcement also played an important role • However, we still have a way to before we will have full compliance with the Act, and for the credit market to operate more effectively in respect of both cost and allocation of credit

Thank You ! www.ncr.org.za