Download

1 / 23

230 likes | 305 Views

Partnership Cash Distributions. Cash Distributions: 1. Reduce outside basis of partner. 733. 2. No gain or loss to extent of outside basis. 731(a). 3. If exceed outside basis, excess treated as gain from sale of partnership interest. 731(a)(1). Usually capital gain.

E N D

Partnership Cash Distributions Cash Distributions: 1. Reduce outside basis of partner. 733. 2. No gain or loss to extent of outside basis. 731(a). 3. If exceed outside basis, excess treated as gain from sale of partnership interest. 731(a)(1). Usually capital gain. 4. 752 twist – reduction in partner’s share of liabilities deemed cash distribution. Corporate & Partner Tax Instructor: Dwight Drake

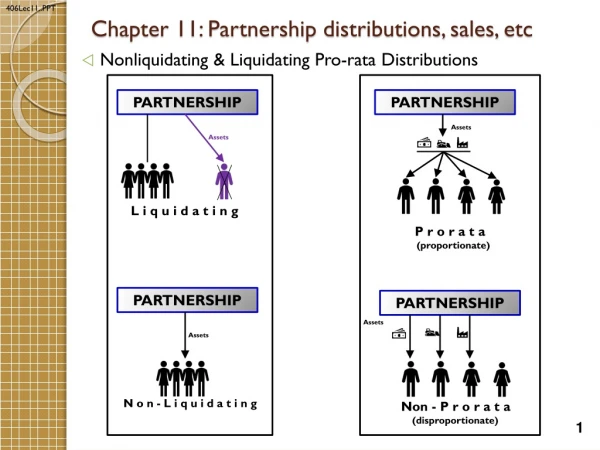

Partnership Property Distributions Property Distributions: 1. No gain or loss to partnership or partner unless: - Marketable securities distributed. - Property distributed is same property contributed by another partner within last 7 years – 704(c)(1)(B) exception. - Distributions of property to contributing partner within 7 years of contribution – 737 exception. - Unrealized receivables and substantially appreciated inventory is distributed – the 751(b) nightmare exception. Corporate & Partner Tax Instructor: Dwight Drake

Partnership Property Distributions – NoExceptions Apply Consequences: 1. No gain or loss to partnership or partner. 2. Partners basis in distributed property equals partnership’s basis, but can’t exceed partners basis in partnership reduced by money realized in same transaction. 732. New Partner Election: If partner who receives property distribution acquired partnership interest within last 2 yrs by purchase, exchange or inheritance, may elect to increase such partnership’s inside basis in property allocable to such partner to equal partner’s outside basis. Election only good for determining basis of distributed property. 732(d), 743(b). 3. Partner’s outside basis reduced by 732 basis of property to partner. 4. If unrealized receivables distributed, ordinary income taint always sticks to partner. 735(a). Corporate & Partner Tax Instructor: Dwight Drake

Partnership Property Distributions – NoExceptions Apply Consequences: 5. If inventory of partnership distributed, ordinary income taint to partner sticks for 5 years. 735(2). 6. Nonrecognition transaction cannot be used to remove the taint. 7. Depreciation recapture ordinary income taint (1245) carries over to partner who gets property. 8. Holding period of partnership tacked onto to partners holding period. 735(b). 9. Partnership’s distribution of property have no impact on inside basis of other property held by partnership. 734(a). Partnership may make 754 election and increase inside basis of assets for (1) any gain recognized by partner under 731(a)(1) ( money in excess of basis) and (2) excess of partnership’s adjusted basis in property before distribution over basis actually picked up by partner under 732. Corporate & Partner Tax Instructor: Dwight Drake

Partnership Property Distributions – NoExceptions Apply Consequences: 10. When property distributed to partners, inside capital accounts of all partners must be adjusted to reflect gain or loss that would be realized if property had been sold for its fair market value on date of distribution. This is to keep capital accounts in balance even though no gain or loss recognized. Corporate & Partner Tax Instructor: Dwight Drake

The Marketable Securities Exception – 731(c) Rule: Distribution of marketable securities treated like distribution of cash. - Marketable securities are financial instruments and foreign currencies that are actively traded. - Gain recognized by partner if FMV exceeds outside basis. - Partner’s basis is 732 basis plus gain recognized by partner. - Amount deemed distributed to partner reduced by decease in partner’s distributive share of net gain in partnership’s marketable securities. Corporate & Partner Tax Instructor: Dwight Drake

Mixing Bowl Exception – 704(c) When Apply: Property contributed by one partner distributed to another within 7 years. Impact under 704(c): Contributing partner must recognize 704(c) built-in gain as if property had been sold for FMV on date of distribution to other partner. Corporate & Partner Tax Instructor: Dwight Drake

Contributing Partner Exception – 737 When Apply: Partner contributes property with built-in gain and partnership distributes other property to partner within 7 years. Impact under 737: Contributing partner must recognize gain equal to lesser of : - FMV of distributed property over outside basis, or - Pre-contribution gain” – gain that would be recognized under 704 if contributed property had been distributed to other partner within 7 yrs. Corporate & Partner Tax Instructor: Dwight Drake

Problem 296 - 1 Facts: ABC Partnership distributes 10k cash and land (value 10k, basis 10k) to each partner. A o/s basis 20k: B 10k, C 5k. Tax impact each partner. A has 10k return of capital on cash (731), no income on land receipt (733), land basis of 5k transfers to A (732), A outside basis reduced to 5k. B receipt of cash tax free, o/s basis reduced to zero by cash, basis in land is zero. C has 5k capital gain per 731(a)(1) because cash exceeds basis. C basis in land and outside basis reduced to zero per 732(a)(2). What impact if C received land first, then cash? Land receipt would reduce outside basis to zero per 733 and C takes 5k basis in land. All 10k of cash later received would be taxable LTCG per 731(a)(1). What impact in (b) if 10k cash is draw against income for year? Deemed cash distribution on last day of year per Reg. 1.731-1(a). Offset by income basis increase for year. Smart to couple with repay obligation if income not enough to cover. Corporate & Partner Tax Instructor: Dwight Drake

Problem 296 - 2 Facts: Partner with 40k basis receives in pro rata distribution Asset #1 (basis 40k, value 10k) and Asset #2 (basis 20k, value 10k). What will be partner’s basis in assets under 732(c) if: #1 is inventory, #2 is capital asset? Per 732(c)(1)(A), outside basis first allocated to inventory. So inventory has 40k basis, capital asset has zero basis. #2 is inventory, #1 is capital asset. Inventory gets first 20k basis, and capital asset is allocated next 20k. Both assets inventory. Carryover basis reduced by 20k excess of inventory basis over outside basis. Allocated based on unrealized depreciation. #1 basis reduced from 40k to 25k; #2 reduced to 15k. Both assets capital. Same reduction allocation and answer as (c). Both assets inventory. #1 has value of 60k; #2 has value of 50k. No depreciation to allocate basis reduction. Thus 20k reduction allocated by asset basis (each 1/3). #1 basis is 26.667k; #2 basis is 13.333k. Corporate & Partner Tax Instructor: Dwight Drake

Problem 296 - 3 Facts: NP buys 1/3 interest for 40. Partnership has receivables (basis 0, value 30k) and land (basis 60k, value 90k). 10k of receivables distributed to each partner. NP impact on receivable distribution if no 732(d) election? NP takes zero basis in receivables, retains 40k o/s basis, and recognizes 10k ordinary income on collection per 735. Receivable distribution impact if NP make 732(d) election? 743(b) adjustment would give NP 10k basis in receivables so no income on collection. NP outside basis after 10k AR distribution if 732(d) election made? Outside basis goes from 40k to 30k per 733. Partnership approval required for 732(d) election? No. Personal to partner. Very different than 754 election. 732(d) election impact on land basis? No immediate impact on basis. If land distributed to NP within 2 years of acquisition, then election would impact. Corporate & Partner Tax Instructor: Dwight Drake

Problem 299 - 1 Facts: A, with 10k o/s basis in ABC Partnership, receives as part of pro rata distribution land inventory (basis 2k, value 3k) and receivable (basis 0, value 3k). Six years later, collects receivable, sells land for 3k. Tax results? On distribution, A takes carryover basis of 0 in receivables and 2k in land per 732(a) and A’s o/s basis reduced to 8k per 733. On collection of receivables, A has 3k ordinary income as taint is permanent under 735 (a). On sale of land in year 6, A has 1k of LTCG. Five year inventory taint has expired. (b) Will 5 year inventory taint apply if A immediately gift land to daughter and then daughter sells as a capital asset? Yes – 5 year taint will stick with any gift. 735(c)(2)(A), 7701(a)(42), 7701(a)(45). Corporate & Partner Tax Instructor: Dwight Drake

Problem 299 - 2 Facts: A, with 1k o/s basis in two person taxi partnership, receives as part of pro rata distribution a taxi (basis 2k, value 3k) purchased one year ago for 5k. A immediately sells taxi for 3k? Tax results? A’s basis in taxi is limited to 1k, his o/s basis before distribution. 732(a)(2). On sale, 2k of income recognized, of which only 1k is 1245 recapture because that is max 1245 partnership would have realized on 3k sale. 1245(b)(6)(A). Thus, A has 1k of 1245 ordinary income and 1k of 1231 or LTCG income. S Corporate & Partner Tax Instructor: Dwight Drake

Problem 305 Facts: A, 1/3 partner in ABC partnership with 70k basis capital account valued at 80k, receives asset #1 with 90k basis and 60k value and reduces interest to one-ninth. Impact if no 754 election? A takes #1 with basis of 70k per 732(a)(2) and his o/s basis reduced to zero. Partnership recognizes no loss per 731(b) and makes no adjustments under 734. Post distribution balance sheet as follows: A.B FMV A.B FMV Cash 60k 60k A 0 20k Asset #2 40k 60k B 70k 80k Asset #3 20k 60k C 70k 80k Totals 120k 180k 140k 180k S Corporate & Partner Tax Instructor: Dwight Drake

Problem 305 Facts: A, 1/3 partner in ABC partnership with 70k basis capital account valued at 80k, receives asset #1 with 90k basis and 60k value and reduces interest to one-ninth. (b) Impact if 754 election? Same impact to A - takes #1 with basis of 70k per 732(a)(2) and his o/s basis reduced to zero. Partnership recognizes no loss per 731(b) but makes asset adjustments under 734. Post distribution balance sheet as follows: A.B FMV A.B FMV Cash 60k 60k A 0 20k Asset #2 46.7k 60k B 70k 80k Asset #3 33.3k 60k C 70k 80k Totals 140k 180k 140k 180k S Corporate & Partner Tax Instructor: Dwight Drake

Problem 305 Facts: A, 1/3 partner in ABC partnership with 70k basis capital account valued at 80k, receives asset #1 with 90k basis and 60k value and reduces interest to one-ninth. (c) How should 20k 743 allocation be allocated among partners? Asset#1 had 30k built-in loss that would have been allocated equally (10k) each if sold. A may still net 10k loss because his basis in asset is 70k and value is 60k. Since B and C can no longer recognize any loss on that asset, best to allocate the upward asset basis adjustment to them so they may recognize 20k less income (or more loss) down the road. S Corporate & Partner Tax Instructor: Dwight Drake

Problem 310 Facts: ABC partnership formed with A contributing land “1 (basis 2k, value 10k) B contributing land #2 (basis 5k, value 10k) and C contributing land #3 (basis 10k, value 10k). Tax impact if: ABC sells #1 for 10k? 8k allocated to A per 704(c); A’s outside basis goes to 10k per 705(a)(1)(A). ABC distributes #1 to C six years post formation? Per 704(c)(1)(B), A recognizes 8k income, A’s o/s basis goes to 10k, and ABC’s basis in asset goes to 10k prior to distribution to C. Normal distribution rules for C. ABC distributes #3 to A six years post formation? Per 737 seven year rule, A must recognize of lesser of FMV of #3 over o/s basis (8k) or built-in gain on #1 (also 8k). So A has 8k LTCG, A o/s basis before distribution increased to 10k, A’s basis in #3 is 10k following distribution, A’s o/s basis after distribution is zero, and partnership’s basis in #1 increased to 10k. 737(c)(2). S Corporate & Partner Tax Instructor: Dwight Drake

Problem 310 Facts: ABC partnership formed with A contributing land “1 (basis 2k, value 10k) B contributing land #2 (basis 5k, value 10k) and C contributing land #3 (basis 10k, value 10k). Tax impact if: ABC distributes #2 to A six years after formation? Double whammy. Per 704, B has 5k LTCG, B o/s basis goes to 10k, and partnership’s basis in #2 goes to 10k. Per 737, results to A are same as in (c) – 8k income to A and associated basis increases. ABC distributes #2 to A one year post formation? Results same to B as in (d). But for A, transfer with 2 years deemed exchange of #1 for #2. 707(a)(2)(B). This could produce higher income if values have increased. ABC distributes #1 to B and #2 to A six years out and properties like kind? Like kind exchange trumps 704(c)(1)(B) and normal distribution rules apply. Neither A or B recognize income. A’s basis in #2 is 2k and A’s o/s bais goes to zero. B’s basis in #1 is 2k and B’s o/s basis goes to 3k. S Corporate & Partner Tax Instructor: Dwight Drake

Problem 310 Facts: ABC partnership formed with A contributing land “1 (basis 2k, value 10k) B contributing land #2 (basis 5k, value 10k) and C contributing land #3 (basis 10k, value 10k). Tax impact if: (g) ABC distributes like kind property to A six years post formation? Does like kind exchange change application of 737 if there is not related distribution to another partner that would trigger 704(c)(2)? No per Reg. 1.737-1(d). A would recognize 8k income, basis in exchange property would be 10k. S Corporate & Partner Tax Instructor: Dwight Drake

Problem 319-1 Facts: A, 1/3 partner in ABC partnership with 3k basis capital account valued at 6k, receives in non pro rata distribution receivables with 0 basis and 3k FMV and A’s interest reduced to one-fifth. Triple tax impact. - A deemed to have received 2k phantom distribution of 741 assets – 800 cash (40%) and 1200 capital asset (60%). A’s basis in capital asset is transferred 400 and A’s o/s basis reduced 1200 to 1800. - A then deemed to have sold cash and capital asset for 2k of receivables. A recognizes 800 capital gain and B and C recognizes 1k each on receivable transfer. B and C o/s basis each go up 1k. Partnership’s basis in capital asset goes to 1200. - Partnership deemed to have distributed 1k of receivables to A in pro rata distribution. A takes basis in these receivables of zero. A’s o/s basis remains at 1800. S Corporate & Partner Tax Instructor: Dwight Drake

Problem 319-1 Facts: A, 1/3 partner in ABC partnership with 3k basis capital account valued at 6k, receives in non pro rata distribution receivables with 0 basis and 3k FMV and A’s interest reduced to one-fifth. Balance sheet at end is as follows: A.B FMV A.B FMV Cash 6k 6k A 1.8k 3k Capital Asset 3.8k 9k B 4k 6k C 4k 6k Totals 9.8k 15k 9.8k 15k S Corporate & Partner Tax Instructor: Dwight Drake

Problem 319-1 Facts: A, 1/3 partner in ABC partnership with 3k basis capital account valued at 6k, receives in non pro rata distribution receivables with 0 basis and 3k FMV and A’s interest reduced to one-fifth. (b) How is increase in partnership’s asset basis from deemed purchase allocated to partners? Since purchase, there really should be no need for special allocation of basis increase. No 704(c) allocation because not contributed. Nevertheless, some think should be allocated to non-distributee partners (B and C) here because they are taxed on the deemed transfer of the excess receivables for the 741 assets. See Reg. 1.704-1(b)(5)-Example 14(i). S Corporate & Partner Tax Instructor: Dwight Drake

Problem 319-2 Facts: A, 1/3 partner in ABC partnership with 12k basis capital account valued at 18k, receives accounts receivables with 0 basis and 9k FMV and other two partners each receive 9k inventory which has basis of 9k. (a) Does 751(b) apply? No. Each partner received equal share of 751 assets. Fact that all appreciation went to A is not controlling. Big factor is that there was no misallocation of 751 and 741 assets. (b) Lesson is that 751 does not stop assignment of income among partners. It works to prevent disproportionate allocations of classes of property among partners. S Corporate & Partner Tax Instructor: Dwight Drake