Download

1 / 10

100 likes | 112 Views

Delve into the regulatory perspective of risk in European pensions with insights on risk management strategies and addressing current risk worries.

E N D

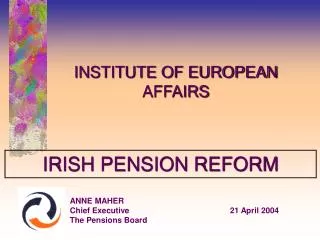

EUROPEAN PENSIONS 2006 RISK AND RISK SHARING – REGULATORY PERSPECTIVE Anne Maher Chief Executive London The Pensions Board 10 October 2006

Agenda • What is risk? • Influence of risk on regulation • Should pension provision include risk? • Current risk worries and how they might be addressed 2

What is risk? • The prospect of some event occurring which will cause disruption to the expected view of the future • Hazard, chance of bad consequences, loss etc, exposure to change or injury or loss 3

What is risk? For Pension Provision • Risk was always there but rarely mentioned until after 2000 • Focus was on investment returns/benchmark risk • Scheme liabilities or investment return/liability risk became high focus when accounting standards required disclosure • Main risks • Plan sponsor • Investment/market • Interest rate • Inflation • Longevity • Fraud or failure • ‘Risk’ is now recognized as big issue 4

Influence of risk on regulation Main reasons for pension regulation are about risk i.e. • Control of commercial relationships between parties whose knowledge or power is unequal • Avoid risk of market failure of a financial institution 5

Influence of risk on regulation Regulators/Supervisors • Need to identify and prioritise risk areas • Supervision strategies should be based on risk assessment • Use risk assessment to focus regulatory activity in way which achieves good cost/member protection balance • Most regulators (and European Commission) aspiring/moving towards more risk-oriented regulatory framework • But need to avoid trying to regulate risk out of the market 6

Should pension provision include risk? • All business is about risk and opportunity • Cash or bond funds provide most risk-free investment for pensions but greatly increase the cost • Trustees (or scheme management board) should: • Decide level of risk they can accept • Develop risk management framework • Managing risk should be priority for them 7

Current risk worries – How they might be addressed • Longevity Risk • Huge impact and great uncertainty • Longevity assumptions should be transparent • Prudent to fund for further expected improvements • Defined Benefit Risk • Funding standards and permitted recovery periods different in every country • Poorly matched investment and membership profiles common – driven by investment return motive without trustee understanding of ‘risk’ • Most funding standards include some acceptance of deficiencies and consequent risk • Tightening of funding standards would help (but have other consequences) 8

Current risk worries – How they might be addressed(continued) • Move to Defined Contribution • In DC individual bears salary, investment, inflation and longevity risk • Individual cannot take risks at same level as large entity • Individual will not have expertise/experience • Clarity of options and good explanatory material essential • Greater responsibility for employers/trustees to provide appropriate back-up for individuals faced with decisions would help • Alternative DB/DC solutions help accommodate shared risk • New Trends in Investment • Liability Driven Investment (LDI) being promoted as the great solution to controlling risk • But LDI involves unregulated investment • LDI could involve excessive concentration of risk in one issuer • Trustees (or advisers) likely to have little experience and may not understand the trade-offs and their costs • Handle with care! 9

Conclusion • Modern desire to avoid risk but • Group pension provision should continue to accept risk and give high priority to managing it • Individual pension provision should minimise risk • And regulators should monitor risk but not • Try to regulate it out of the market or • Frustrate pension operation or development by excessive risk regulation 10