Download

1 / 10

110 likes | 138 Views

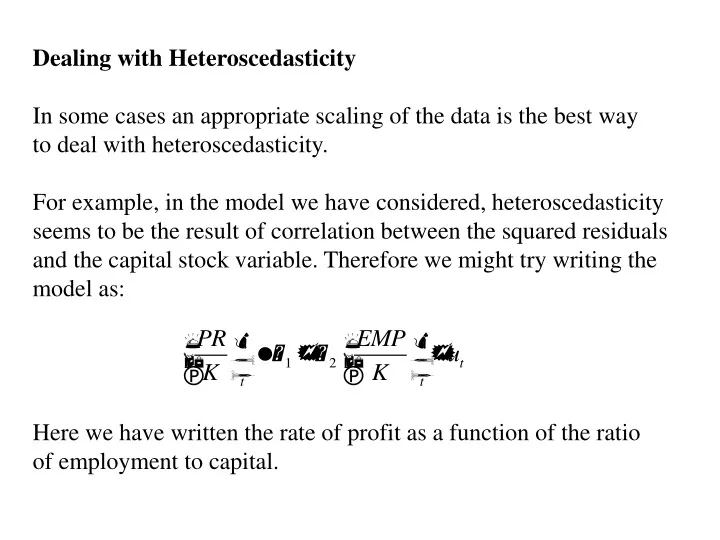

Dealing with Heteroscedasticity In some cases an appropriate scaling of the data is the best way to deal with heteroscedasticity. For example, in the model we have considered, heteroscedasticity seems to be the result of correlation between the squared residuals

E N D

Dealing with Heteroscedasticity In some cases an appropriate scaling of the data is the best way to deal with heteroscedasticity. For example, in the model we have considered, heteroscedasticity seems to be the result of correlation between the squared residuals and the capital stock variable. Therefore we might try writing the model as: Here we have written the rate of profit as a function of the ratio of employment to capital.

More importantly, there is no longer any evidence of heteroscedasticity.

White’s heteroscedasticity consistent covariance matrix If the model we are estimating takes the form: Then White argues that a consistent estimator of the covariance matrix for the OLS estimator can be obtained using the following expression. Where is an NxN matrix with the squared OLS residuals on the diagonal and zeros elsewhere.

The advantage of this approach is that it allows us to get consistent estimates of the standard errors of the regression parameters in cases where the form of the heteroscedasticity is not obvious. Note that OLS will still be inefficient when we use the White covariances (in fact the parameter estimates don’t change at all). However, we can conduct reliable statistical inference even when heteroscedasticity is present.

Example: The profits model with White standard errors is shown below: Note that the standard errors are higher and the t-statistics lower than when we use the OLS variance matrix.

Autoregressive Conditional Heteroscedasticity ARCH So far the type of heteroscedasticity we have considered has been applicable to cross-section models. ARCH is a type of heteroscedasticity which is relevant for time series models and particularly for financial time-series models. ARCH models the variance of the error as a function of the size of random shocks hitting the model and its own past values. The effects of ARCH are that periods of volatility can last for some time and the OLS residuals may not follow a normal distribution.

To test for ARCH effects we take the OLS residuals and perform the following auxiliary regression. We then test for the significance of the lagged squared residuals in this equation. This is a first-order ARCH process More generally, we could include any number of lags in the auxiliary regression. For example, a second order ARCH process would take the form.

Example: OLS estimation of a market model for Vodafone shares yields the following estimates. (Data is daily from 1995 to 2000).

Testing for a first-order ARCH process yields the following: