Download

1 / 7

70 likes | 81 Views

Learn how to calculate option prices using the Binomial and Black-Scholes models. Explore case studies and formulae for European Call and Put options in financial decision-making.

E N D

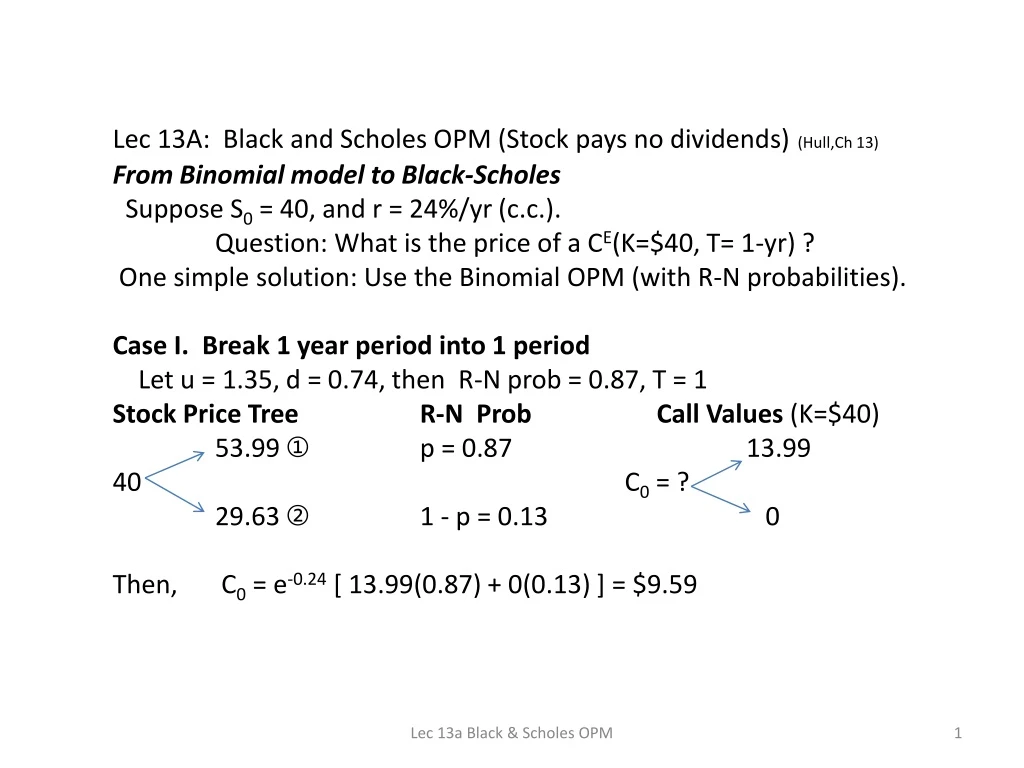

Lec 13A: Black and Scholes OPM (Stock pays no dividends)(Hull,Ch 13) From Binomial model to Black-Scholes Suppose S0 = 40, and r = 24%/yr (c.c.). Question: What is the price of a CE(K=$40, T= 1-yr) ? One simple solution: Use the Binomial OPM (with R-N probabilities). Case I. Break 1 year period into 1 period Let u = 1.35, d = 0.74, then R-N prob = 0.87, T = 1 Stock Price Tree R-N Prob Call Values (K=$40) 53.99 ➀ p = 0.87 13.99 40 C0 = ? 29.63 ➁ 1 - p = 0.13 0 Then, C0 = e-0.24 [ 13.99(0.87) + 0(0.13) ] = $9.59 Lec 13a Black & Scholes OPM

Case II. Break 1 year into 2 sub-periods. Set u = 1.236, d = 0.8089; then p = 0.7454 Stock Price Tree R-N Prob Values at Expiration 61.138 ➀ p2 = 0.556 ➀ 21.14 ➀ 49.45 40 40 ➁ 2p(1-p) = 0.380 ➁ C0 = ? 0 ➁ 32.35 26.17 ➂ (1-p)2 = 0.065 ➂ 0 ➂ Call Value C0 = e-0.24 [ 21.14(0.556) + 0(0.380) + 0(0.065) ] = $9.24 Lec 13a Black & Scholes OPM

Case III. Break 1 year into 3 sub-periods. u =e0.30√(1/3) =eσ√T/n = 1.189, d= 1/u i.e. d=e-0.30√(1/3) =e -σ√T/n = 0.841, and p ={e0.24(1/3) -d}/{u-d} = {1.0833 -0.841} /{1.189-0.841}= 0.696 Call Value C0 = e-0.24 [ 27.26(0.3372) + 7.56(0.4418) + 0 ] = $9.86 Lec 13a Black & Scholes OPM

Limit Case: Black-Scholes European Call Option formula(p. 4) as n → ∞, the binomial model becomes C0 = S0 N(d1 ) – K e-rT N(d2 ) d1 = [ ln(S0 /K) +(r+σ2/2) T ]/(σ √T) , and d2 = [ ln(S0 /K) +(r-σ2/2) T ]/(σ √T) T = time to expiration in years (or fraction of a year) σ2 = annualized variance of stock returns N(d1)= area under graph of standard normal cumulative prob ( -∞ to d1 ) N(d2)= area under graph of standard normal cumul. probability (-∞ to d2) in Excel =NORMSDIST(d1) r= c.c. risk-free rate Lec 13a Black & Scholes OPM

Limit Case: Black-Scholes European Call Option formula(p. 4) C0 = S0 N(d1 ) – K e-rT N(d2 ) Example: Use same data as in cases I, II etc. to price a European Call S0 = $40, K = $40, T = 1 (1 year), σ2 = 0.09/year ⇒ σ = 0.30/yr d1 = [ ln(40/40) +(0.24+0.09/2) 1 ]/(0.30 √1) = 0.950 d2 = [ ln(40/40) +(0.24-0.09/2) 1 ]/(0.30 √1) = 0.65 N(d1) = Area up to 0.95 = 0.8289, N(d2) = Area up to 0.65 = 0.74215 ∴ C0 = 40 (0.8289) - 40(e-0.24 (1)) (0.74215) = $9.81 Compare to Binomial prices: n = 1, Binomial price = $9.59 n = 2, Binomial price = $9.24 n = 3, Binomial price = $9.86 n = 4, Binomial price = $9.51 NOT BAD!! Lec 13a Black & Scholes OPM

Black-Scholes model for European Puts(p. 4) Recall the Put-Call relationship: +S +P = +C +B. Solve for the price of the put: P0 = S0 [1-N(d1 ) ] – K e-rT [1-N(d2 ) ] Alternatively, use the fact that N(K) + N(-K) = 1, then P0 = -S0 N(-d1 ) + K e-rT N(-d2 ) Example: Use same data to price a European Put S0 = $40, K = $40, T = 1 (1 year), σ2 = 0.09/year ⇒ σ = 0.30/yr P0 = -40(1-0.8289) + 40(e-0.24 (1)) (1-0.74215) = $1.27 Lec 13a Black & Scholes OPM

Thank You (A Favara) Lec 13a Black & Scholes OPM