Download

1 / 50

500 likes | 664 Views

The Transmission Mechanisms of Monetary Policy. This paper presents in the first part the theoretical dimension of the transmission channels of monetary policy.

E N D

The Transmission Mechanisms of Monetary Policy • This paper presents in the first part the theoretical dimension of the transmission channels of monetary policy. • In the second part an econometric analysis of Romania’s channels of monetary policy transmission is performed using VAR and cointegration. • Conclusions.

Classifying the channels of monetary policy transmission If we imagine the economy like a large network of interconnecting institutions like banks, corporations, medium and small firms and households, finding a monetary transmission mechanism implies finding a connection starting at the Central Bank’s level and following the Central Bank’s transactions effect on the other players until the effect reach the real sector. All the paths have one similarity – they must pass thought some financial market. Using this criteria we can classify the channels of monetary policy transmission it two sections: The channels which involve the commercial lending market. The channels that pass thought other markets.

The channels which involve the commercial lending market The channels that operate through the commercial lending market are: The interest rate (or money) channel The credit channel Bank lending channel Balance sheet channel Households liquidity effects

The interest rate (or money) channel 1 / 2 • This channel is a classical theme of the present economic literature, the first researcher mentioning it was J.M.Keynes, and the first model that incorporated this channel was ISLM. The key assumptions in this transmission mechanism are: • there are only 2 classes of assets: money and the other assets • there is no substitute for money in the economy • An expansion in the money supply leads to a fall in interest rates which in turn lowers the cost of capital, causing a rise in investment spending, thereby leading to an increase in aggregate demand and a rise in output. • This channel doesn’t operate just thought businesses’ decisions about investment spending, consumer decision about durable goods are also being considered as investments. • The emphasis is on the real interest rates, rather than on nominal interest rates. In addition the long term interest rate and not those on short term are viewed as having the major impact on spending. • Also an expansion in money supply can raise the expected price level and thereby the expected inflation, which cause a drop in the real interest rates, with the consequences presented earlier.

The interest rate (or money) channel 2 / 2 • This mechanism indicates that monetary policy can be effective even when nominal interest rates are 0. • Examples of countries where econometrical studies found that the interest rate channel is important in conducting monetary policy: • Germany (Sigfried, 2000, Hamburg University) • Columbia (Carrasquilla, NA, BIS) • Hungary (Nemenyi, 1996, ONB) • Poland (Kokoszcznski, 1996, ONB)

The credit channel 1 / 4 • Dissatisfaction regarding the explications provided by the interest rate channel has led to a new theory involving asymmetric information in financial markets. This type of explication proposed two types of monetary transmission channels: • the bank lending channel • the balance sheet channels (involving decisions made by firms and households) • The starting hypotheses in the credit view are: • non monetary assets are not substitutable • the credit market presents problems generated by asymmetric information • This channel emphasize the role of the banking sector, the special role of banks in the economy given by their high expertise level, the small costs of such a process and the ability of banks to solve asymmetric information problems. This channel also emphasize the special relation between the Central Bank and the rest of the banks in the system. It’s obvious that a developed banking sector, with an important share in the total financial sector, is the primary requirement for the existence of a credit channel. • The credit channel is not a substitute but more a complement or enhancement of the interest rate channel.

The credit channel 2 / 4 • Econometrical studies have found operational credit channels in the following countries: • USA (Romer C., Romer D., 1993, Berkley University) presents an important credit channel in monetary policy transmission, rather surprisingly because alternative sources for financial resources exist, contradicting one of the hypothesis presented earlier. The authors stress the weakness of this monetary transmission mechanism in responding to small changes in monetary policy and the powerful response transmitted in case of radical changes in monetary policy, followed by massive intervention by FED. • Israel is another example, the study has been made by De Fiore (1998, IMF), and the author is explaining this finding by presenting the primordial role of the banking system in Israel’s financial system and the distortions created in the system by different rates of mandatory reserves requirements on different types of deposits. This distortion generate different interest rates at deposits in $ and shekels, and changes in monetary policy induce changes in internal credit’s price and variations in the volume of this credits versus the credits in foreign currencies.

The credit channel 3 / 4 • Econometrical studies have found also countries in which the credit channel doesn’t appear to be important: • Germany (Sigfried, 2000, Hamburg University) provides proofs that the credit channel has no important effect in Germany. This is surprising because having in mind the importance of the German banking system in the financial system, and the key role played by the banks in financing enterprises (70% of the German firms external finance is provided by banks compared with just 25% in USA), and knowing the weakness of the German stock market as an alternative for raising financial resources, one could presume that Germany will be the obvious example of a credit channel at work. One of the explanations of this apparent contradiction given by the author is the traditional long term relationship between banks and enterprises, and another the bond insulated asset side of the banks balance sheet, capable of shielding the credit volume from changes produced in the liabilities side of the banks balance sheet by the monetary policy. Proofs of this practice are also provided by Kakes, Jan-Egbert, Maiery (1999, Groningen University). The authors reveal that the structure of the loans are changing in times of monetary policy tightening in favor of loans taken by big corporation.

The credit channel 4 / 4 • Europe as a whole is considered to be an example of the importance of the credit channel as demonstrated by Favero, Giavazzi, Flabbi (1999, NBER). The authors prove that banks in Germany, France and Italy are using different methods to shield the loans from variations in the liability side of the balance sheet. The large banks in France and Germany are using their security holding to offset any change in the monetary policy, and the small banks are using their excess liquidity to grant loans in times of a tightening monetary policy, taking advantage of the increased interest rates. The large banks in Italy have a solid position, generate by large holdings of public debt. • Netherlands is another example of a non functioning credit channel as proven by Kakes Jan (1998, Groningen University). The author reveals the large buffer stocks of securities held by banks in order to counterbalance any monetary policy change. • Columbia is another counter example of a credit channel. The author Carrasquilla (NA, BIS), is blaming the lack of reaction at the banks level to monetary policy changes for the bank crisis in 1985. The lack of reaction at the continuous restrictive monetary policy has lead to severe liquidity problems.

Bank lending channel 1 / 4 The bank lending channel (or credit channel in the strict sense) theory is based on the special role played by the banks, because they are very well suited to resolve asymmetric information problems in credit markets. Because of bank’s special role, certain borrowers will not have access to credit markets unless they borrow from a bank. So a central hypothesis of this channel is that credit is not substitutable with anything else. In fact this hypothesis is questioning the Miller – Modigliani theorem, because if this theorem is correct a tightening in monetary policy should have no effect on the banks and firms. Banks should be capable to raise alternative funds, for example issuing large CDs . So if Miler Modigliani theorem is correct a change in monetary policy is affecting only the structure of bank’s liability side of the balance sheet, and not the volume. The key hypotheses in the bank lending channel are: • banks cannot shield their portfolios versus changes in monetary policy • the borrowers cannot shield their real expenses form changes in credit volume • the banking system must be an important part of the financial system If mandatory reserve requirements are important, so are the chances that a monetary policy intervention will generate effect on the volume of credit. A reduction in

Bank lending channel 2 / 4 the liquidity will generate less opportunities to issue credit, because liquidity created by the Central Bank is more than legal money, is in a sense an issuing of credit right for the other banks in the system. A possible problem, that could have put a question mark in the bank lending channel’s existence, is mentioned by an important number of studies, revealing the synchronization between the fall in industrial production and the fall in credit volume. The problem is determining who cause the other: credit falls first and influence output or the fall in output leads to a fall in credit demand an to a reduction in credit volume. A possible answer at this answer is provided by Ramsey (1993, IMF) which determine that the credit volume after a tightening in monetary policy is not changing, the change is in the structure: less credit issued by banks and more commercial credit. He also presents the raising gap between interest rates of commercial credit and credit issued by banks in periods of tight monetary policy. Examples of a functioning bank lending channel is provided for the following countries: • USA (Kashyap, Stein, 1997, NBER) is considered as an good example for bank lending channel and the study performed had proven that the small banks that are

Bank lending channel 3 / 4 an important part of the system, are the ones responsible for the effectiveness of this channel because the small banks cannot shield large variation in resources volume. Another finding of this study is that small firms cannot shield their real expenses from bank credit fluctuations because they are denied the opportunity to use other sources for finance by the prohibitive costs. • Another example is Japan (Collins, Morsink, Bayoumi, 1999, IMF), where because of the lack of financing alternatives, small firms must endure the variations in the credit volume. In fact the dependency of banks upon the Central Bank and the dependency of the forms upon credit financing is so important that this is the most important channel, in the author’s opinion, of monetary policy transmission in Japan. • Another example is Spain (Hernando, 1998, BIS). In this paper the author is proving the increasing gap between the interest rates of commercial credit and bank credit in periods of tight monetary policy, and also the study accentuate the log lag between change in policy and the effect on output. Also the study reveals that the interest rate channel is very powerful in the short term. Hernando considers that in the existence of the bank lending channel a very

Bank lending channel 4 / 4 important element is the tools or instruments used by the Central Bank, as an example he gives countries as UK and Japan, with a relative important bank lending channel, as a result, in the author’s view, of the tools used to control the credit volume.

Balance sheet channel The existence of this channel is die to asymmetric information. This channel is stressing the impact of the monetary policy on the balance sheet of the firms, and the relationship between the balance sheet of the firm and the problems of asymmetric information and the forms taken by this, the adverse selection and the moral hazard. If the monetary policy is relaxed it’s obvious that prices of the assets of the firms are increasing and so is the net value. A grater net value diminishes the risk generated by adverse selection and moral hazard. The lax monetary policy could also reduce the interest rate, which in time improves the cash flow of the firm, so this is another factor in diminishing the adverse selection and moral hazard problems. Another possible channel could involve as a result of a lax monetary policy an increase in the non anticipated price levels, reduces the value of the credits that firms have taken, increasing the net value of the firm, with the same consequences as presented before on adverse selection and moral hazard.

Households liquidity effects The effect of the monetary policy has been focused a long time on the effect on the balance sheet of firms, but effect are created in the balance sheets of households too. The asymmetry in this case is not in the credit market but in the market of durable goods, which generate a under pricing for this items. So, any decision involving durable good is viewed as an investment decision. A lax monetary policy leads to higher prices of the assets and an increase of the financial assets. This leads to a smaller probability of financial problems in the future and the households can spend more on durable goods and houses. The increased spending is leading to a rise in demand and ultimately in output. The reduced liquidity of this assets (durable good, houses) is due to the asymmetric information on these markets, and this reduced liquidity makes consumers reluctant in buying these types of assets. If the households have doubts about the probability of financial problems in the future they will invest their money in financial assets, with no consequence on output as previously presented. The difference between the balance sheet channel and this channel is that not the willingness of lenders to lend cause expenditure to rise but the willingness of consumers to spend.

The channels that pass thought other markets The channels that operate through other markets than the commercial lending market are: The exchange rate channel Stock market channel Tobin’s q theory Wealth effects Durable goods price channel

The exchange rate channel 1 / n The exchange rate channel, with the internationalization of economies throughout the world and the advent of flexible exchange rates, has received an increasing attention than in the past. This channel also involves changes in interest rates because the interest rate differential between the countries creates capital migration and exchange rate modifications. Fluctuations in the exchange rate leads to increased or decreased in the price of exports denominated in the foreign currency, and leads to increases or decreases in export production and of course in the output level. Also imports are cheaper or more expensive with exchange rate fluctuations, and domestic consumption can be persuaded by the change in prices to consume more domestic goods or more foreign goods. The exchange rate channel is very important in small open economies. Examples of countries with significant exchange rate channels are: • Mexico (Diaz, NA, BIS) is considered as an example, the changes in interest rates leading to changes in foreign investment and for this matter in output. The importance of the openness of the economy is also stressed in this paper. • Israel is another example of a country with a functional exchange rate channel (De Fiore, 1998, IMF). The classical path of exchange rate channel transmission

The exchange rate channel 2 / n is augmented, in the view of the author, with a wealth effect generated by changes in the exchange rate because the prices of the durable goods and houses are denominated in foreign currency. • Another example is Poland (Kokoszcznski, 1196, ONB) even if for a short period of time. The author considers that in the period of 1993-1995 positive net exports lead to a appreciation of the zlot with consequences in the asset structure of the firms, with effects on the output.

Stock marker channel 1 / 2 The stock market channel of monetary policy has been ignored a long period of time. This channel is based on variations of the equities (stock) prices. The main two sub channels of transmission are: the Tobin’s q theory and wealth effects. The stock market provides a very important function for firms – the possibility to raise capital. A change in the monetary policy has immediate and powerful effects on the equities prices. As the economies all over the world are in a process of deregulation, the importance of the stock market channel is increasing. Also the generalized involvement in the stock market of households and firms (40% of USA population are shareholders compared with just 27% in 1984, as revealed by Chami, Cosimano, Fullenkamp, 1999, IMF) is increasing the role the stock market is playing in monetary policy transmission. Another factor that accentuate the importance of this channel is the increased sensitivity of firms management at equities price variation in the market. Changes in price are followed by rapid and important investment policy changes. Another factor is the institutional nature of the stockholders (30% of the shares in USA is held by mutual funds and another 50% by other institutions like pension funds). This institutional nature of the stock holders leads to a rise in the frequency of management changes, this also making management more receptive to

Stock marker channel 2 / 2 stockholder’s interests. This evolutions also lead to more efficient stock markets and to rapid reactions by management, usually anticipating the stockholders decision. With an ever increasing number of individuals and institutions buying shares, with the influence of the shareholders on the management increasing, and with decisions in investment policies of the firms closely followed by the owners, the stock market channel has an important role to play in the transmission mechanism of monetary policy in the future.

Tobin’s q theory James Tobin developed a theory that explains how monetary policy can affect the economy through its effects on the valuation of equities. Tobin defines the q coefficient as the market value of firms divided by the replacement cost of the capital. If q is high the market price of firms is high relative to its replacement costs and a new plant and equipment is cheap relative to the market value of the firm. Companies are able to issue stock and get a high price. Investment spending will rise because firms can buy a lot of new investment goods with only a small issue of stock. If q is low the firms will not made new investments but buy another firm cheaply and acquire old capital instead. The link of this theory with the monetary policy is through the prices of equity in the stock market. An increase of money supply will lead to a rise demand for stock, to higher prices and to high q coefficient. This theory was tested by Chami, Cosimano, Fullenkamp (1999, IMF) and the results were disappointing. The problems could be the way the q coefficient is defined or the inability to measure it correctly.

Wealth effects The balance sheet of households can be an important explicative factor in monetary transmission mechanism and the life cycle theory of F. Modigliani provides the theoretical base. Modigliani’s theory emphasize that consumers are optimally adjusting their consumption taking into account the resources that are available now as well as the resources that will be available in the future. The financial wealth is an important part of the consumer’s resources and an increase in the price levels of equity, generated by an increasing money supply, can lead to a rise in resources available in the future, and to a rise in the present consumption.

Durable goods price channel Tobin’s q theory can be applied to other markets too, for example the housing market or land market. A rise in the q coefficient on this markets, as a result of higher prices determined by a lax monetary policy, will stimulate the production of houses. Land prices are a very important part of the wealth of an individual or firm, and an increase generates an shift in the consumption behavior, with effects on aggregated demand and output.

Econometric analysis of Romania’s channels of monetary policy transmission. Time series utilized Granger causality tests Variations in IP and the importance of the other variables Response functions – unrestricted VAR 3 variable - unrestricted VAR 6 variable - unrestricted VAR Tests of stationarity Cointegration relationships 3 variable 4 variable Mandatory reserves requirements Real evolution of Crng, M2, Ref Refinancing Crowding out

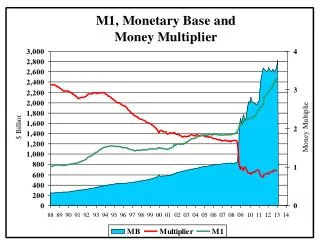

Mandatory reserves requirements 1 / 2 Knowing the degree of control of the monetary base by the NBR, the effect of each monetary instrument, we can assess the force and the implications of the instruments that can be used by the Central Bank. One instrument, very powerful and intimately linked with the credit channel is the mandatory reserve requirements. The frequent change in the rates of the mandatory reserves is another important proof in supporting the existence of a strong credit channel in Romania. The purpose of these changes is to influence the liquidity available to banks and the level of credit available to the economy.

Mandatory reserves requirements 2 / 2 Because mandatory reserves are applied only on certain types of deposits, it may be important to calculate the evolution of the percent of reserves in money base and broad money. It is important to notice that every change in reserve requirements has a powerful impact on the profit and loss account of the bank, and if the changes are very swift and very wide, the consequences could be a very difficult situation for the banking system, especially for the banks with less liquidity. So the use of reserve requirement must be gradual and combined with an increase of the interest rate used to remunerate the reserve requirements.

Refinancing Also the instruments of monetary policy had changed from refinancing credit to deposits attracted by the NBR. Refinancing credit was abandoned; the volume has dropped in nominal terms, and the change in real terms was more abrupt. The graph is a short representation of refinancing credit in real terms having the start of 1991 as a mark. The change in the structure of refinancing credit is very significant, especially the drop in auctions credit and the raise of special credits, which are uses mainly to save bank in a poor financial situation.

Crowding out Another important element in the changes that has happened in Romania is the crowding-out effect, the substitution by the state of the private enterprises as borrowers. The nongovernmental credit is replaced by governmental credit. Also nongovernmental credit denominated in lei is replaced by nongovernmental credit denominated in a foreign currency.

Conclusions 1 / 4 • The transmission mechanisms of monetary policy in Romania are heavily determined by the structure of the Romanian economy, by the structure of the financial system and by the legal framework. As a result of the study conducted in the previous chapter, and as a result of the study of other channels of monetary policy transmission, the following conclusions appeared: • The traditional interest rate channel is one of the channels used in Romania, but the influence of this channel is very weak, a possible explication being the need for resources at any cost from the economic sector, as a result of chronic under capitalization. This is why an interest rate change leads to small changes in industrial production and another factor suggesting a relative small usage of this instrument is the relative stability of the real interest rates. • The other assets price channel is also a mechanism of monetary policy transmission with little importance in Romania. There are several reasons why its importance is so small: • The stock market is poorly developed, the volume of stock market capitalization and the volume of transactions is very small as percent in GDP. Also de stock market is mainly used to privatize state enterprises, and less used to raise capital or to evaluate the financial situation of a firm.

Conclusions 2 / 4 • The exchange rate channel has some influence on industrial production, but only on a short term, for several reasons. The first is the rigidity of Romania’s production for export at changes in exchange rate or foreign demand. Another reason, and a possible explanation for the first is the use of foreign materials to produce exported goods, so the cost of the exported products incorporate the exchange rate used to value the imported raw materials. An example of this situation is the textile industry, which represents 30% of both imports and exports, a clear indication of the use of lohn system. Another example is the petrochemical industry, etc. A change of the real exchange rate leads to a short term change of the industrial production volume because the relative cheaper imported raw materials and the bigger price received are short lived, till the next import of raw materials. In the next period when the firm will import raw material at the new exchange rate the costs will be higher, and the prices will increase too. So the inflation will rise and the real exchange rate will return at the previous level. The time period in which an effect of the exchange rate devaluation will persist is proportional with the length of the average production process in sectors that realize exports, and the proportion of imported raw materials in the finished product.

Conclusions 3 / 4 • The credit channel is probably the most powerful mechanism of monetary policy transmission. There are several reasons for this situation. The first the reliance of firms upon credit for replacing inexistent working capital. Another reason is the heavy reliance of the commercial banks upon the Central Bank at least for refinancing credit. For the firms, the interest rate is not a problem, the only problem being implicit quantitative restrictions in the credit supply, which are frequently generated by Central Bank’s policy. The use of the mandatory reserve requirements, the frequent change of this rates and the rapid change in methodological aspects in this domain, illustrate the importance of the credit channel. A separation between the various secondary channels, which compose the credit channel, is difficult, but adverse selection and moral hazard have an important role to play in an instable economy. The bank-lending channel is probably equally important. The large contribution of nongovernmental credit variations at changes in output has been demonstrated in this paper. On the other hand maybe the simultaneous reduction of real nongovernmental credit and industrial production in recent years is not a coincidence. The channel of the household’s liquidity is also very weak considering the poor development of consumption credit and the continuous fall in the sales of durable goods.

Conclusions 4 / 4 Of course the present paper can be improved, the usage of VAR methods can be criticize in some respects, so future studies should use structural VARs, or another quantitative methods needed to offset the “Lucas critique”. In the following years one can expect the Central Bank to continue to use monetary aggregates as intermediary objectives, moreover due to the ceilings on NDA and floors on NIR imposed by the agreements with the IMF. In the log term the structural changes in the Romanian economy will lead to changes in monetary transmission mechanisms, as in other countries had already happened. The credit channel will decrease in role and other channels will take its place. Significant steps in this transformation will be a real liquid secondary market for bonds, a more efficient stock market, a smaller degree of dependence upon the Central Bank for the commercial banks, etc. In order to achieve the ambitious objectives that Romania presented to the EU, the monetary policy will retain it’s importance, and the topic of the transmission mechanism will be a central problem, because only knowing the most efficient transmission mechanism the optimal decisions can be made and implemented. In order to understand the transmission mechanism a methodic and periodic study of this problem is needed, and in a rapidly changing economy the problem is more acute.