Download

1 / 17

170 likes | 427 Views

University Budget and Finances. A guide for TUFA members. University finances oversight committee, 2010. Remit: To provide accurate information to the TUFA membership and Executive on University finances. To document the budget structure and decision-making procedures within the University.

E N D

University Budget and Finances A guide for TUFA members

University finances oversight committee, 2010 Remit: • To provide accurate information to the TUFA membership and Executive on University finances. • To document the budget structure and decision-making procedures within the University. • To identify and highlight issues that affect the membership in relation to University finances. • To provide support to the membership and Executive through these activities, in preparation for collective bargaining and responses to specific financial issues that affect working conditions. • To employ financial specialists on an ad hoc basis to fulfill the remit. To this end, we have identified questions for the administration on the budget (UFOC 1), received a response (UFOC 2) and provided an assessment of that response (UFOC 3)

Budget decision making • The Trent University Administration is responsible for deciding what, how, and when budget information is presented. It is important to recognize that the ADMINISTRATION is not a neutral provider of budget information. Their own agenda will influence their preparation, approval and presentation of budgets.

Budget decision making • Who decides the budget? • Senior management decide the budget and send it to the Board of Governors for approval • Currently, it seems that the Provost’s Planning Group is responsible: • Acting Provost and Vice President Academic (chair) • VP Admin • VP Research • VP External Relations • Acting Dean • Dean of Grad Studies • University Librarian • Director of Public Affairs

Budget decision making • It is not clear how often the budget planning is done, who scrutinizes it at what stages (although perhaps Academic Planning committee does this) and whether the Board of Governors (the ultimate authority), scrutinizes it in relation to the University’s mission. • Eg, see UFOC 2 – 2.1 - There is an acknowledgement that the current budget making processes do not operate in integration with the University’s stated mission. The future procedures they discuss are presumably the current Integrated Planning process run out of the President’s Office. Update letter no. 5 on Integrated Planning (President’s website) promises planning cycles that integrate budgets to overall strategic goals – something which is missing right now (remember that we had a financial crisis in 2008 that was apparently going to resolve issues). There is also a promise for clear and transparent information – something which is again absent right now.

Budget decision making • What is the mechanism for getting budget information from ADMINISTRATION? • Nothing clearly stated in terms of the processes described above: • Transparency is therefore a serious issue, as is clarity of the information presented • These are promised in the current proposal for Integrated Planning (see update letter 5 on President’s website).

Budget presentation • In Ontario, there are no accounting policies or principles that govern how budget information is presented to stakeholders. Within the budgeting context, the ADMINISTRATION will choose among different acceptable ways to present budgets i.e. loose, tight, etc. depending on their motive. This flexibility allows significant room for interpretation and discussion around what is fair presentation of accounting information (including substantial estimates) at Trent University. In essence, budgeting is more of an art than a science.

Budget presentation • Padding happens when operational revenues are underestimated and operational expenses are overestimated. This "padding" is done so if revenues come in higher than the budgeted number, the ADMINISTRATION will look especially productive. The difference between the padded amount and the realistic amount is called budgetary slack. • Current budget is padded (see UFOC 1- 1.1) and administration’s response was vague, justifying their estimates but without any indication of how extra revenues that might appear would be allocated (see UFOC 3 – section 1)

Budget presentation • A balanced budget is the requirement from the Board of Governors (UFOC 2) • We are pursuing whether running a deficit is possible given the generation of future income – from hydro generation, new residences and possibility of staff renewal through VER (see UFOC 3 – section 3) • Again, there seems no strategic planning from the administration on these issues.

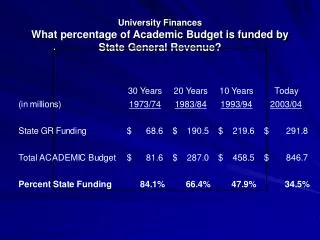

Budget definitions • The operating budget is the account of revenues and expenses and is therefore the relevant issue for discussion. • Remember, that it remains a future estimate when presented each year. • 97% of Trent salaries are sourced from the operating budget (see recent OCUFA report) • Revenue for operating budget is federal, provincial grants and tuition (72% 08-09 average in ON in OCUFA report)

Initial 2010-11 “Budget” Presented at Joint Committee: 2010-01-21

Updated version • The publication by the Provost’s Planning Group proposes a 2.6m shortfall – and lists costs of 2.2m for pension contributions, 0.4 for fringe benefit inflation, 0.9m for increased operating costs of buildings and scholarships and some new staff costs. Increased revenue is estimated at 2.4m from enrolment. One time funding is included but we are told they do not expect it this year.

Revenues and expenses • We have asked for clarity in TUFA salaries as a proportion of overall salaries (which the Admin consistently tells us is 84% of operating expenses – see UFOC 3). • We are pursuing whether the operating budget has been used to pay off other expenses (such as building costs – see UFOC 3)

Revenues and Expenses • Trent University Statement of Operations and DeficitYear Ended April 30, 2009 • REVENUE 2009 2008 • Government grants 60,092 59,694 • Tuition fees 38,454 37,614 • Ancillary sales and services 18,527 19,027 • Donations and grants 3,529 2,425 • Investment income 1,763 1,961 • Miscellaneous 2,666 2,533 • Totals 125,031 123,254 • EXPENSE • Salaries and benefits 88,406 85,266 • Scholarships and bursaries 7,762 8,083 • Utilities 2,671 2,850 • Supplies 22,713 22,633 • Interest amortizations 1,365 1,406 • Library acquisitions 658 723 • Other capital assets 7,734 7,631 • Change in fair value of financial (53) 728 • Totals 131,256 129,320

Revenues and Expenses • EXCESS OF EXPENSE OVER REVENUE FOR THE YEAR (6,225) (6,066) • Change in internally restricted 2,254 4,170 net assets • Change in investment in 488 865 Capital assets • INCREASE IN DEFICIT FOR THE YEAR (3,483) (1,031) • DEFICIT – beginning of year (9,933) (8,902) • DEFICIT – end of year $ (13,416) $ (9,933)

Salaries and benefits • Once we have some requested information, we will add to this slide, but this is from Trent’s latest report card • Academic/instructional Support Library Student services Total • 2004-05 52.54% 7.90% 4.65% 14.40% 79.5% • 2005-06 53.31% 7.59% 4.65% 13.13% 78.7% • 2006-07 52.99% 7.64% 4.41% 12.75% 77.8% • 2007-08 54.81% 8.28% 4.34% 12.25% 79.7% • 2010-11 53.00% 8.00% 5.00% 13.00% 79.0%

Key issues • Transparency of process and accountability • Transparency of instructional budget versus other expenses in operating budget • Integration of University mission and strategic goals to budgeting procedures • Recognition of the importance of instructional staff and research to University delivery of its mission and its reputation • Long term planning on key financial cost issues affecting TUFA