Download

1 / 21

210 likes | 283 Views

Explore formulas for present value & accumulated value of annuities & perpetuities in financial settings with increasing payments in geometric progression. Calculations include effective interest rates & varying payment scenarios.

E N D

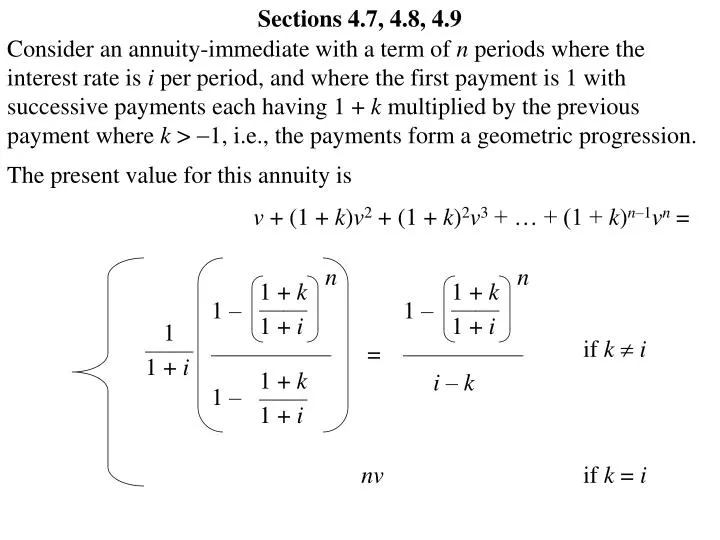

Sections 4.7, 4.8, 4.9 Consider an annuity-immediate with a term of n periods where the interest rate is i per period, and where the first payment is 1 with successive payments each having 1 + k multiplied by the previous payment where k > 1, i.e., the payments form a geometric progression. The present value for this annuity is v + (1 + k)v2 + (1 + k)2v3 + … + (1 +k)n–1vn = n n 1 + k —— 1 + i 1 + k —— 1 + i 1 – ————— = 1 – 1 – ————— i– k 1 —— 1 + i if ki 1 + k —— 1 + i nv if k=i

The accumulated value after n periods for this annuity-immediate is (1 + i)n– (1 + k)n ——————– i– k if ki and is n(1 + i)n 1 if k=i. i– k —— 1 + k Suppose k < i , and let i* = . If payments occur at the beginning of each period, the present value for this annuity-due is 1 + (1 + k)v + (1 + k)2v2 + (1 + k)3v3 + … + (1 +k)n–1vn–1 = 1 – (v*)n ———– = 1 –v* 1 – (v*)n ———– = d* .. a – n| i* 1 + v* + (v*)2 + (v*)3 + … + (v*)n–1 = We see that the present value of an n-period annuity-due with payments increasing in geometric progression with common ratio (1 + k) and effective interest rate i is equal to the present value of a level n-period annuity-due with interest rate i*. The accumulated value after n periods for this annuity-due is .. a – n| i* (1 +i)n

Consider a perpetuity with a payments that form a geometric progression where 1 < k < i. The present value for such a perpetuity with the first payment at the end of the first period is The present value for such a perpetuity with the first payment at the beginning of the first period is 1 —— i– k 1 + i —— i– k Observe that the value for these perpetuities cannot exist if 1 + k 1 + i.

The first of 30 payments of an annuity occurs in exactly one year and is equal to $500. The payments increase so that each payment is 5% greater than the preceding payment. Find the present value of this annuity with an annual effective rate of interest of 8%. 100k = 5% is the periodic (yearly) increase in payments. 30 1.05 —— 1.08 1 – ————— = 0.08 – 0.05 $9508.28 500 Suppose 100k = 5% is the periodic (yearly) increase in payments. Then the present value would be 30 0.95 —— 1.08 1 – ————— = 0.08 + 0.05 $3764.11 500

In exactly one year from today, a perpetuity-immediate begins making annual payments. The first payment is $600. With an effective rate of interest of 7%, find the present value of this perpetuity if (a) each future payment is increased by 3% more than the previous payment, (b) each future payment up to and including the 15th payment is increased by 3% more than the previous payment, and payments starting with the 15th payment remain level thereafter. 600 ————— = 0.07 – 0.03 For part (a), the present value is $15,000 For part (b), the present value is the sum of the present value for the first 15 payments and the present value for the remaining payments.

For part (b), the present value is the sum of the present value for the first 15 payments and the present value for the remaining payments. 15 1.03 —— 1.07 1 – ————— = 0.07 – 0.03 $6529.81 600 15 1 —— 1.07 1 —— = 0.07 600(1.03)15 $4840.11 $6529.81 + $4840.11 = $11,369.92

A participant in a pension plan will earn $40,000 salary in the upcoming year, and this salary will be increased by 4% each year after. For each of the next 25 years, a contribution of 3% of the salary for the year together with a matching amount from the employer is made to the pension fund at the end of the year. If the pension fund earns 8% effective per year, find the accumulated value of these contributions at the end of the 25-year period. 1.0825– 1.0425 —————— = 0.08 – 0.04 40000(0.06) $250,958.33

Consider annuities payable less frequently than interest is convertible. We let k = n = i = the number of interest conversion periods in one payment period, the term of the annuity measured in interest conversion periods, rate of interest perconversion period. It follows that n / k = the number of annuity payments made. Let A be the present value of a generalized increasing annuity with payments 1, 2, 3, etc. occurring at the end of each interval of k interest conversion periods. Then, n — – 1 k n — k A = vk + 2v2k + … + vn–k + vn n — – 1 k n — k (1 + i)kA = 1 + 2vk + 3v2k + … + vn–2k + vn–k

n — – 1 k n — k A = vk + 2v2k + … + vn–k + vn n — – 1 k n — k (1 + i)kA = 1 + 2vk + 3v2k + … + vn–2k + vn–k Subtracting the first equation from the second, we have n — k A[(1 + i)k– 1] = 1 + vk + v2k + … + vn–k–vn a – n| a – k| a – n| n — k This is the present value of an increasing annuity with payments 1, 2, 3, etc. occurring at the end of each interval of k interest conversion periods. – —————— i vn a – k| A = s – k| Similar derivations can be done when payments increase in some other arithmetic progression.

Page 9 of the Class Notes: With an effective rate of interest is 6%, find the present value of payments of $8 at the end of three years, $16 at the end of six years, $24 at the end of nine years, etc., if (a) the last payment is at the end of 27 years. a – n| a – 27| n — k 27 — 3 – —————— = i vn – —————— = (0.06) v27 a – k| a – 3| (8) (8) $128.82 s – k| s – 3|

Consider an increasing annuity payable more frequently than interest is convertible with constant payments during each interest conversion period. Let the annuity be payable mthly with each payment in the first period equal to 1/m, each payment in the second period equal to 2/m, etc. Letting i = rate of interest per period, we use i(m) to write a formula for the present value of the n-period annuity-immediate denoted by . (m) (Ia)– n| Making the mthly payments of k/m in period k is the same as making one payment equal to the accumulated value of the mthly payments at the end of the period, that is, one payment of k — m k — m (1 + i(m)/m)m – 1 ——————— = i(m)/m i k — i(m) = s – m| i(m)/m 1 — m 1 — m 1 — m 1 — m k–1 —– m k — m k — m k — m k — m n–1 —– m n — m n — m m — m n — m … … … … … 0 1 k– 1 k n – 1 n

Consequently, the increasing annuity payable mthly is the same as an increasing annuity with P = Q = , which implies i — i(m) .. a – n| i — i(m) – nvn ————— i(m) (m) (Ia)– n| (Ia)– n| = = i — i(m) (m) (Ia)–– | We may choose to write 1 1 — + — ii2 1 1 — + —— i(m) i(m) i = = i — i(m) i k — i(m) i n — i(m) 1 — m 1 — m 1 — m 1 — m k–1 —– m k — m k — m k — m k — m n–1 —– m n — m n — m m — m n — m … … … … … 0 1 k– 1 k n – 1 n

Page 10 of the Class Notes: With an effective rate of interest is 6%, find the present value of payments of $8 at the end of every 4 months in the first year, $16 at the end of every 4 months in the second year, $24 at the end of every 4 months in the third year, etc., if (a) the last payment is at the end of 27 years. .. a – 27| i — i(3) – 27v27 ————— i(3) (3) (Ia)– 27| (m) (Ia)– n| (Ia)– 27| = = 8m 24 = 24 24 = 14.003 – 5.599 ——————— 3[(1.06)1/3 – 1] = $3428.06 24 (b) the payments continue forever in perpetuity. (m) (Ia)–– | 8m 1 1 ——— + —————— 0.05884 (0.05884)(0.06) 1 1 — + —— i(m) i(m) i = 24 = 24 = $7206.17

Find the present value of a perpetuity which pays 1 at the end of the third year, 2 at the end of the sixth year, 3 at the end of the ninth year, etc. Let i be the effective rate of interest, and treat 3 years as one period. Then i* = is the rate of interest for three years. (1 + i)3– 1 With P = Q = 1, the present value of the perpetuity is PQ — + — = i*i*2 1 1 ————— + ————— = (1 + i)3– 1 [(1 + i)3– 1]2 v3 ——— (1 –v3)2 (1 + i)3 ————— = [(1 + i)3– 1]2 Observe that if the payments are at the end of ever kth year (period), the general formula is Also, look at Example 4.15 in the textbook (page 139) for an alternative way to obtain this present value. vk ——— (1 –vk)2

Page 9 of the Class Notes: With an effective rate of interest is 6%, find the present value of payments of $8 at the end of three years, $16 at the end of six years, $24 at the end of nine years, etc., if (a) the last payment is at the end of 27 years. a – n| a – 27| n — k 27 — 3 – —————— = i vn – —————— = (0.06) v27 a – k| a – 3| (8) (8) $128.82 s – k| s – 3| (b) the payments continue forever in perpetuity. v3 ——— = (1 –v3)2 (8) $261.14

Find the accumulated value at the end of eight years of an annuity in which payments are made at the beginning of each quarter for four years. The first payment is $3000, and each of the other payments is 95% of the previous payment. Interest is credited at 6% convertible semiannually. 3000 (1.03)16 + (0.95)(1.03)15.5 + (0.95)2(1.03)15 +… + (0.95)15(1.03)8.5 = 3000 (1.03)16 1 + (0.95/1.03) + (0.95/1.03)2 +…+ (0.95/1.03)15 1 – (0.95/1.03)16 ——————— = 1 – (0.95/1.03) = 3000 (1.03)16 $49,134.18

Consider an increasing annuity payable more frequently than interest is convertible where the first mthly payment in the first period is 1/m2 with each mthly payment increasing by 1/m2 throughout and across all of the n interest conversion periods. Letting i = rate of interest per period, we use i(m) and the formula for to write a formula for present value of the n-period annuity-immediate denoted by . (Ia)– n| (m) (I a)– n| (m) .. a – n| – nvn ————— i (Ia)– n| Recall that where the annuity payments are 1, 2, 3, … n respectively at the end of n periods with interest rate i per period. With an interest rate of i(m) /m for each of nm periods and respective payments of 1/m2 , 2/m2 , 3/m2 , … nm/m2 at the end of each period, we have = .. a ––– nm | i(m)/m 1 —————— (1 + i(m)/m)nm nm – (m) (I a)– n| 1 — m2 (m) = = i(m) — m

.. a ––– nm | i(m)/m 1 —————— (1 + i(m)/m)nm nm – (m) (I a)– n| 1 — m2 (m) = = i(m) — m 1 — m 1 – 1/(1 + i(m)/m)nm ———————— (i(m)/m)/(1 + i(m)/m) 1 —————— (1 + i(m)/m)nm n – = i(m)

.. a ––– nm | i(m)/m 1 —————— (1 + i(m)/m)nm nm – (m) (I a)– n| 1 — m2 (m) = = i(m) — m 1 — m 1 – 1/(1 + i(m)/m)nm ———————— (i(m)/m)/(1 + i(m)/m) 1 —————— (1 + i(m)/m)nm n – = i(m) 1 – 1/[(1 + i(m)/m)m]n ———————— i(m)/(1 + i(m)/m) 1 —————— [(1 + i(m)/m)m]n n – = i(m)

.. a ––– nm | i(m)/m 1 —————— (1 + i(m)/m)nm nm – (m) (I a)– n| 1 — m2 (m) = = i(m) — m 1 — m 1 – 1/(1 + i(m)/m)nm ———————— (i(m)/m)/(1 + i(m)/m) 1 —————— (1 + i(m)/m)nm n – = i(m) 1 – 1/[(1 + i(m)/m)m]n ———————— i(m)/(1 + i(m)/m) 1 —————— [(1 + i(m)/m)m]n n – = i(m) 1 – 1/(1 + i)n —————— i(m)/(1 + i(m)/m) 1 ——— (1 + i)n ..(m) a – n| n – – nvn ————— i(m) = i(m)

Look at each of the following: In Section 4.9, find the symbol for, and definition of, the present value for an increasing n-period annuity with payments made continuously at the rate of t per period at exact moment t. In Section 4.9, find the formula for a general, continuous varying annuity, and look at Example 4.18. In Section 4.10, consider Table 4.1 (page 142) in the textbook.