Download

1 / 16

160 likes | 267 Views

SWISS GLOBAL ECONOMICS Macroeconomic Analysis November 24, 2012. Growth Miracles: Analytic Narratives From East Asia, China, and India.

E N D

SWISS GLOBAL ECONOMICS Macroeconomic Analysis November 24, 2012 Growth Miracles: Analytic Narratives From East Asia, China, and India

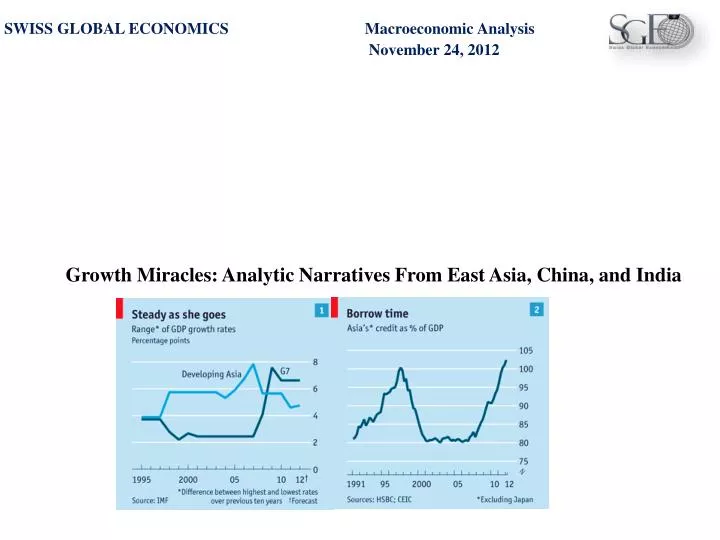

The Macroeconomic Context Three Defining Themes: Asia will remain the fastest-growing region The recovery in many countries has been driven by large fiscal stimulus and loose monetary conditions. With fiscal stimulus now being withdrawn and monetary policy tightened across the region, the onus is again switching to autonomous private-sector demand. This robust growth is due to two factors: Both levels of government and private debts are low, and most Asian countries’ banking sectors have little exposure to US sub-prime debt or to sovereign debt from the euro zone’s peripheral economies. The emergence of China as an independent engine of regional growth and a source of final demand for regional economies. China’s economy will continue to lead the Regional Pack Loose credit conditions; a government-backed stimulus package that has boosted investment were behind the acceleration of a 10.3% GDP growth in 2010. Growth is expected to fall back to 9% in 2011 due to the end of stimulus spending and a policy tightening that will slowdown investment in real estate. Strong income growth will support consumption with the government remaining prepared to switch to a more supportive stance. Inflation will continue to pose a serious risk to growth that could lead to a more volatile outcome. The Chinese government is adopting a series of monetary and administrative measures to cool the economy: Raising nominal interest rates. Hiking the one-year lending rate and the one-year deposit rate by 25 bp. Constraining prices by releasing stocks of food and fuel from government warehouses. Curbing bank credits to reduce the high levels of financing available in the economy. A scaling back of stimulus in ASEAN A rise in Capital inflows is raising the stakes of overheating and rising inflation. 2011 will witness a focus on rolling back fiscal stimulus measures and tightening monetary policy while minimizing the risks of appreciation that a higher interest rates could have on the exchange rates. Fiscal and monetary stimulus helped some economies to rebound from declines in output induced by the weakening of electronics demand during the global _____________________________________________________________________________________________________________________ A spike in inflation and a policy over-reaction could bring GDP growth down to an unexpectedly low levels

The Macroeconomic Context Asia XJ : Growth and Inflation (% change) • Asia’s Saving Glut • The high levels of domestic investment and large capital outflows resulting from across the board high domestic savings is causing large current account imbalances. • The expected rapid ageing of the population will lead to a sharp decline in domestic saving rates mitigating the need for government intervention to reduce the large account surpluses. • The domestic saving rates • Three main factors influences saving rates: • The age structure of the population. • The degree of financial sector development. • Income levels.

The underpinnings of Financial Development • I. Infrastructure: • The stability and development of markets and institutions are based on adequate and appropriate infrastructure. • Well-functioning legal and governance frameworks are vital for a sound and competitive financial sector: • A high correlation exists between the variables of the rule of law; effective bureaucratic, judicial and governance process; defined and enforceable property rights; awareness and control of corruption. • Big spread between economies in East Asia. • On these indicators, some are getting beter (eg China, Laos), some are getting worse (eg Indonesia, Philippines). • II. Financial Markets: • Huge potential in the region because of productive capacity, population, saving, and wealth. • Market development is mixed: • By asset class: stocks, bonds, forex, derivatives. • Domestic growth and expanding FDI require local financing and so need better and bigger domestic stock and bond markets and access to derivatives to manage risk. • By economy: by size(japan dominates but less so) and by range of products and market sophistication(three groupings of economies) • Correlated with Indicators of “infrastructure” • Sound market infrastructure should be combined with international cooperation and capacity building. • III. Trends in Commercial Banks • Trends in Bank Credit: • Bank credit to GDP first peaked in the 1990s, peaked again in 2006/07 in selected countries. • Recovered most in Korea and Malaysia. • Banking Sector restructuring and consolidation • Systemic banking crisis in many countries. • Varying institutional frameworks for financial and corporate restructuring, with varying success. • In a broader context of financial consolidation for economiesof scale, competitiveness, safety in size.

Future Trends In Commercial Banks • Banking sector restructuring and consolidation • Reform of the regulatory and supervisory framework • Coordination/harmonization vs. unified super-regulator. • CAR based on risk more broadly defined, i.e. complexity. • Restrictions on leveraging. • Inclusion of non-bank financial institutions. • Improved corporate governance of firms, including financial institutions • Improvement in rules relating to transparency, disclosure, protection of minority rights, and consistent enforcement • Systemic risk • Focus on institution or product? • Too big To Fail= Too Big To Regulate? • The Unbaked Majority • The microenterprise sector and household savings are the foundations of most economies. • Do not have access to basic banking services, such as credit, savings, and transfer/payments. • Economically active poor, working poor. • Not the poorest of the poor. • Rural and urban.

Growth Miracles:Dissecting The CausesWhat explains these turning points? • Geography? • Natural resources? • Culture? • Level of human capital? • Low inequality? • Institutions? These are all slow-moving (or unchanging) variables • a constant cannot explain a sudden change • at best, these must have interacted with something else that changed

Growth Miracles: Dissecting The Causes Initial equilibrium (pre-reform) farmers: surplus: A - B urban workers: pu, surplus: C + E + F + G + H government surplus: J + K + B • Analytics of heterodox reform: dual-track pricing Post-reform equilibrium (two-track reform) farmers: surplus: A – B + M urban workers: (pu,, p*), q*surplus: C + E + F + G + H + N government surplus: J + K + B Equilibrium under complete liberalization farmers: p*, q* surplus: A + J + K + G + H + M urban workers: p*, q*surplus: C + E + F + N government surplus: 0 Government’s ability to extract output and to commit not to ratchet up deliveries are key.

What explains these turning points? • Changes in policy • Economic liberalization? • Certainly greater market orientation and larger incentives for private entrepreneurship and investments • Greater outward orientation • Big export push in KOR and TWN • Reduction in the role of the state at the margin • But hardly laissez-faire, and many elements of “heterodoxy” • Export subsidies and a range of industrial policies in KOR and TWN • Two-track reforms, lack of privatization, TVEs, SEZs in China • “License raj” and trade restrictions dismantled only gradually in India; big liberalization of 1991 comes a decade after the take-off

Interpretation (1) • Igniting growth requires a relatively narrow range of reforms, targeted at relaxing the “binding constraint” • KOR and TWN: investment externalities: low private return to investment in tradables • CHN: socialism, communes, and price controls: lack of incentives to exert effort and to engage in market activities • IND: (perception of) anti-business attitudes on the part of the government, against a relatively decent institutional background in terms of rule of law and property rights • Rapid growth is possible even in the midst of severe institutional or policy failings • CHN: continued state ownership and weak rule of law • IND: high trade barriers until early 1990s, continued “rigidity” in labor laws, poor infrastructure • When do those become the “binding constraint?” (see below)

Interpretation (2) • Growth-promoting reforms often take unconventional or heterodox forms • KOR and TWN: export subsidies, credit subsidies (KOR), tax incentives (TWN), public enterprises, socialized investment risk • CHN: dual-track reforms, HRS, TVEs, SEZs • IND: mild liberalization of import quotas and industrial licensing during 1980s, compensated by an increase in import tariffs • Conventional account: these are blemishes or necessary compromises made to “politics” • Implication: growth would have been even more rapid in the absence of these heterodox policies • Alternative account: Heterodox policies help overcome specific second-best complications or political constraints • So they are part of the explanation for success • See next slides • But these reforms also create specific downsides • See below

Analytics of heterodox reform: outward orientation with import protection • Import liberalization in theory releases labor to export-oriented activities, where its productivity is higher, generating economy-wide increase in y/l. • But in the real-world, new export-oriented activities may be slow to arise • either because of market imperfections inherent in structural transformation • or because of appreciating currencies • In which case, import liberalization would instead release labor into unemployment or informal activities, with negative consequences for economy-wide y/l. • LA in the 1990s • Protecting employment in import-competing industries, while subsidizing new export oriented activities at the margin (through direct subsidies or SEZ/EPZs) makes sense as a second-best strategy

Analytics of heterodox reform: socializing investment risk • “You invest, I will bail you out if you fail.” • Bad policy if private returns and social returns from private investment are closely aligned • Leads to excessive private risk-taking (“moral hazard”) • But consider a world where: • Investments are lumpy (scale economies) • Their profitability depends on existence of other, complementary investments (e.g., investing in shipbuilding design and engineering skills requires a shipbuilding industry, and vice versa) • The relevant economic activities cannot be costlessly imported or exported • Then, coordination failures can depress private returns (at the margin) below social returns. • And an investment guarantee can crowd in socially productive investments • At no or little cost to the government budget

Analytics of heterodox reform: the downsides • Dual-track reform • Incentive for the government to ratchet quotas up, and hence dynamic credibility issues • Incentive for farmers to evade plan quotas altogether • Maintains rents and groups that benefit from them, rendering eventual comprehensive reform (perhaps) more difficult • Continued import protection • Retains inefficient industries and their owners • Socializing investment risk • Moral hazard and “crony capitalism” (cf. financial crisis of 1997) • Hence the balance of risks and rewards are highly context-specific.

Interpretation (3) • Sustaining growth is perhaps harder, and requires ongoing institutional reforms • At least 83 cases of significant growth accelerations since the mid-1950s, very few of which are sustained • Institutional prerequisites for sustaining growth are of two types in particular • Institutions of conflict management to maintain resilience to shocks and prevent growth collapses • democracy, “rule of law,” social insurance,.. • SSA (mid- to late-1970s) • Latin America (1980s) • Indonesia (1997) • Institutions that maintain productive dynamism and prevent growth from fizzling out • Need for a framework of public policies that foster structural change • Continued IP in East Asia, (gradual) liberalization in India that fostered IT services • Cf. Latin America after the early 1990s • So in the long-run, institutions do rule! • But don’t confuse what is required to instigate growth with what is required to sustain it

General lessons • Binding constraints to growth differ across countries and over time • clear evidence that growth is unlocked in a large variety of ways • different strokes for different folks: CHN was constrained by poor supply incentives in agriculture; BRA is constrained by inadequate supply of credit, SLV by inadequate production incentives in tradables, ZAF by inadequate employment incentives in manufacturing, ZWE by poor governance … • Relaxing binding constraints requires well-targeted reforms that are cognizant of prevailing second-best and political complications • selectivity instead of a laundry list • pragmatism in lieu of “best practice” and rules of thumb • Over time, strengthening institutional underpinnings is critical • institutionalizing “diagnostics” • building resilience to external shocks • institutional reform is key, but to sustain rather than ignite economic growth