Download

1 / 12

130 likes | 393 Views

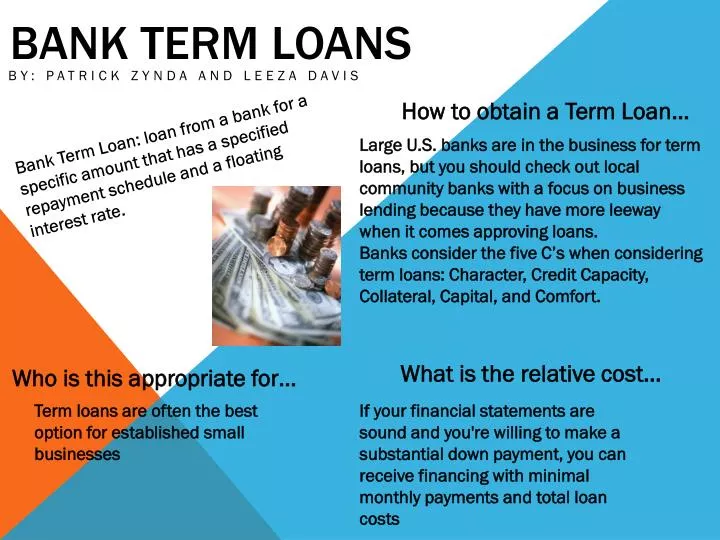

How to obtain a Term Loan…. Bank Term Loan: loan from a bank for a specific amount that has a specified repayment schedule and a floating interest rate.

E N D

How to obtain a Term Loan… Bank Term Loan: loan from a bank for a specific amount that has a specified repayment schedule and a floating interest rate. Large U.S. banks are in the business for term loans, but you should check out local community banks with a focus on business lending because they have more leeway when it comes approving loans. Banks consider the five C’s when considering term loans: Character, Credit Capacity, Collateral, Capital, and Comfort. Bank Term Loans By: Patrick Zynda and Leeza Davis What is the relative cost… Who is this appropriate for… Term loans are often the best option for established small businesses If your financial statements are sound and you're willing to make a substantial down payment, you can receive financing with minimal monthly payments and total loan costs

Description: Give new business’s loans to help start up their company. • You can get loans for real-estate, equipment, and working capital. • Cost: Interest rates fluctuate and are competitive due to SBA limitations • When its used: it is used when businesses need more time to pay back loans when they are starting up their company. • Downside : To file for a SBA loan requires mountains of paperwork and lots of red tape and is very time consuming. SBA Guaranteed Loans Thomas Fisher Brendon Noyes Michael Henriquez

Startup Financing • The initial infusion of money needed to turn the idea into something tangible. • The cost is however much all the expenses add up to. When you are just starting out investors won’t be interested in looking at you so you pay for everything yourself. Who should use Startup Financing and when is it used? It should be used by new business owners and new businesses. It is used after coming up with an idea for a business and you are ready to do the next step and actually start the business. How do I get Startup Financing? • You have to gather up all the money from various places. Such as savings, 401(k)s, relatives, etc. • You are in charge of how well the business starts at because you are using your own money. Jillian Geyer and Luke Downs

504 Loansby Robert & Christopher Description • Covers 40 percent of the expansion your business needs. • You must pay 10 percent of the expansion plan. • The bank (or private sector lender) covers the other 50 percent. • Relative cost is 10 percent out of your pocket. • Limit is five million dollars • the SBA will give a listing of the CDC’s that can give you a 504 loan • They are for long term fix rate financing for business that want to expand on the business. • Cannot be used for capital or purchasing inventory . • Only to help a business gain more assets.

Angel Investors • Description: They are wealthy and willing to invest hundreds of thousands of dollars in a business in return for a piece of the action. Examples: professionals such as doctors or lawyers. • When option is used: Securities Exchange Commission • Relative cost: around $600,000 • Summary of first steps taken in obtaining the loan: 1st Angel investors 2nd sell equity in the company 3rd fill the investment raise with the SEC

Asset-Based Loans • Asset-based loans are loans based on assets that are used as collateral. You are putting your future revenue on the line to gain access to money right now. • They can be a much needed source of capital for companies that are rapidly growing, highly leveraged, or undercapitalized. • Interest rates greatly vary, and banks will sometimes include additional “audit” and due diligence fees to the overall cost of the loan. • Finding an asset-based loan should be easy if your company has good financial statements, good reporting systems, commonly sold inventory, and customers who are known to pay their bills. Jake Mayhew

Initial Public Offerings Stock Issuing Sarah and Allison

Owen Stephenson Microloans • Provides loans up to $50,000 to help small businesses and certain non-profits start up and expand. • The average microloan is $13,000. • Microloans are commonly used for things such as: Inventory/supplies, furniture, and machinery/equipment. • Rates on microloans generally vary from 8 to 13% and are to be repaid in 6 years. • To apply for a microloan one must go through certain nonprofit, community organizations that are experienced in lending and business management assistance.

Royalty Financing Ross Wilburn and Matthew Ingram Description: Investors will lend money to companies and in return the business will give the lender a guaranteed percentage of their revenue for a certain period of time with interest. Usually 2% to 6% of revenue When its used: Business who need cash, but don’t want to give up equity in their company. Relative Cost: Expensive if you bring in a lot of revenue or not that expensive if you don’t make a lot of money. Depending on how much you bring in it could be not that expensive or very expensive. Summary in first Steps: Seek out advice on prospective royalty investors from your local Chamber of Commerce, area Small Business Development Center, a trusted banker, lawyer or accountant. And it might be worthwhile to explore a website such as The Royalty Exchange. The Royalty Exchange is a website in which investors peruse calls for royalty investing from companies producing everything from books to pharmaceuticals to solar energy technology.

Institutional Venture Capital By: Davis and Colton • Institutional Venture Capital includes venture capital from professionally managed funds that have between $25 million and $1 billion to invest in emerging growth companies. • This option is relatively expensive and hard to obtain, but the price depends on where your business is in the business cycle. • This option is appropriate for financing product development or expanding a proven and profitable product or service. • The first step taken is the shotgun approach. This is when a company sends out its information to as many venture capital firms as possible to get a loan in hopes that the business’ numbers will be appealing to one of them.

CDFIs • CDFIs provide credit and financial services to people and communities undeserved by mainstream commercial banks and lenders. • When should CDFIs be used? • CDFIs are used when benefiting a company that intends to help the local community to grow. CDFIs provide capital and services to people and communities. • Relative Cost: • Can vary depending on the business requesting one. • Steps taken to obtain a CDFI: • Most CDFIs involve a community that makes viable loans to businesses that can help the area grow and prosper. Good loan candidates involve money to acquire a business location, purchase equipment, or construct business additions, as well as any kind of funding that actually creates jobs.

401(k) Financing • 401(k) financing is when a business owner cashes in her 401(k) savings account to fund her new business. • The only cost of 401(k) financing is the tax on the withdrawn moneybut the investor has to risk her retirement savings! • Who should use 401(k) financing? • Small business owners who have 401(k) accounts. • Small business owners who are very confident about their business! • People who only need a relatively small amount of money, like a few thousand dollars. How do I get 401(k) financing? The first step is to consult an accountant or tax specialist to make sure that it is legal to take the money out of your 401(k), and what kind of taxes you should expect to pay.