Download

1 / 82

820 likes | 958 Views

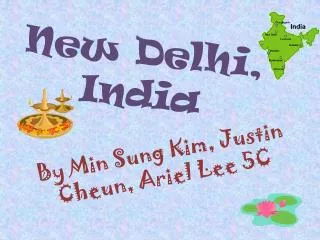

Critical Challenges for the Global Economy ICRIER New Delhi, India April 20, 2007. India: Difference Over A Decade (Index, 1996 = 100). U$12.4 billion. U$197.3 billion. U$4,159 billion. 48.8 % GDP. U$797. U$41.2 billion. U$1,822 billion. 25.7 % GDP. U$2.5 billion. U$406.

E N D

Critical Challenges for the Global Economy ICRIER New Delhi, India April 20, 2007

India: Difference Over A Decade (Index, 1996 = 100) U$12.4 billion U$197.3 billion U$4,159 billion 48.8 % GDP U$797 U$41.2 billion U$1,822 billion 25.7 % GDP U$2.5 billion U$406

Critical Challenges for the Global Economy • Coming in for a soft landing? • Bumps in the runway: • The U.S. housing market • Inflation concerns and the oil market • Financial risks facing emerging markets • Longer-term Challenges: • Unwinding global imbalances • Sustaining global productivity growth

Baseline GDP Growth Forecast Remains for Continued Strong Growth (Percent per annum) 2006 2007

The Housing Correction Has Cooled the U.S. Economy (Percent change from four quarters earlier) Exports Residential investment Investment Consumption Non-residential construction Output Business investment 2003 04 05 06 2003 04 05 06

...And the Slowdown Has Had Limited Impact on the Rest of the World(Percent change from four quarters earlier) Rest of the World United States

Spillovers to the Rest of the World from U.S. Slowdowns Have Been Limited(Change in GDP growth; median for region)

Impact of Growth Declines in the U.S. and Japan (Shading denotes one standard error confidence interval) Impact of U.S. Growth Declines on Growth in Latin America Impact of U.S. Growth Declines on Growth in Emerging Asia Impact of U.S. Growth Declines on Growth in Other Advanced Economies Impact of Japan’s Growth Declines on Growth in Emerging Asia

Investment and Exports are Strong in the Euro Area, But Consumption Lags (Percent change from four quarters earlier) Exports Investment Output Consumption 2003 04 05 06

Japan Remains on Track Despite Mid-06 Dip (Percent change from four quarters earlier) Investment Output Exports (left scale) Consumption 2003 04 05 06

Emerging Market and Developing Country Growth Has Been Strong(Percent; seven-year moving average) Asia Middle East Sub-Saharan Africa Latin America Emerging Europe

Growth in China Continues to Boom(Y/Y percent change) Real GDP Growth (left scale) Fixed Asset Investment (6-month m.a.; right scale)

Growth in India Also Remains Rapid(Y/Y percent change) Real GDP Growth Industrial Production Growth

Markets Go Up, Markets Go Down (Asset class returns; percent change)

But Overall Financial Conditions Remain Supportive of Global Growth Implied Volatilities (percent; 10-day mma) Industrial country equities Emerging Market Currencies Major currencies

Credit Markets Are Pricing in a Soft Landing Policy Rates (percent) Long-Term Rates (deviations from long-term average) United States Futures rates as of 4/10/07 United States Japan Euro area Euro area Japan

Despite Recent Bad News, Our Forecast For Global Growth Is Now More Evenly Balanced (Percent)

Upside risk to global growth Downside risk to global growth Most Global Risk Factors Have Improved Since September (Percentage points of global GDP growth over next 12 months)

Critical Challenges for the Global Economy • Coming in for a soft landing? • Bumps in the runway: • The U.S. housing market • Inflation concerns and the oil market • Financial risks facing emerging markets • Longer-term Challenges: • Unwinding global imbalances • Sustaining global productivity growth

U.S. House Price Increases Have Cooled Fast (Y/Y percent change; relative to CPI) Existing homes (OFHEO) Existing homes (NAR) New homes

Recent Data Paints an Uncertain Outlook for the U.S. Housing Sector Sales (units; millions) Starts and Permits (units; millions) Mortgage Applications for Purchase (index; four week moving average) Inventories (months of supply)

...But Problems in the U.S. Sub-Prime Mortgage Market Seem Contained Spreads (basis points) Housing Market Delinquencies (percent of total residential loans outstanding)

And Household Finances Remain in Good Shape Household Net Assets (ratio to disposable income) Household Liabilities (percent of disposable income) 06: Q4 06: Q4

Housing Is The Tail Not The Dog (Percent increase on previous year for foreclosures; percent for unemployment rate; 2006Q4)

Critical Challenges for the Global Economy • Coming in for a soft landing? • Bumps in the runway: • The U.S. housing market • Inflation concerns and the oil market • Financial risks facing emerging markets • Longer-term Challenges: • Unwinding global imbalances • Sustaining global productivity growth

Inflation Risks Are Down as Headline Inflation Has Moderated (Y/Y percent changes) Headline inflation Core inflation U.S. (PCE) U.S. (PCE) Euro area (HICP) Euro area (HICP) Japan (CPI) Japan (CPI) Feb. 07 Feb. 07

The Elephant in the Room: Rising Levels of Capacity Utilization, Everywhere Output Gap (percent of potential GDP) Non-Fuel Import Prices (December 2005 = 100) Advanced economies United States Euro area World Japan Emerging markets

U.S. Labor Costs Have Accelerated as Productivity Has Slowed (Non-farm business sector; percent change from four quarters earlier) Compensation Productivity Unit labor costs 1996 98 2000 02 04 06

Unemployment Rates Are Declining Across the Major Advanced Economies (Percent) Euro area United States Japan 06 1998 2000 04 02

Growth of World Oil Demand and Non-OPEC Supply Are in Better Balance (2002–06)

But Global Spare Oil Production Capacity Remains Limited (Millions of barrels a day)

Expected Oil Prices Show Continued Potential for a Spike(From futures options; as of April 2nd 2007; U.S. dollars per barrel)

Critical Challenges for the Global Economy • Coming in for a soft landing? • Bumps in the runway: • The U.S. housing market • Inflation concerns and the oil market • Financial risks facing emerging markets • Longer-term Challenges: • Unwinding global imbalances • Sustaining global productivity growth

Capital Flows to Emerging Markets Have Been Strong and Spreads Have Continued to Compress Emerging Market Financing (billions of U.S. dollars) EMBI Global Composite (basis points) 2002 03 04 05 06

But Is It Too Good To Be True? (Billions of U.S. dollars) Emerging Europe and CIS Capital Flows – All Regions FDI Flows to the private sector excl. FDI Flows to the private sector excl. FDI FDI Flows to the public sector Flows to the public sector

If Liquidity Conditions Tighten, Will Capital Flows to Emerging Markets Slow?(Billions of U.S. dollars) Industrial Country Liquidity Index1 (advanced one year; right scale) Financial Flows to Emerging Markets (left scale) 1Computed as the change in base money (measured in U.S. dollars).

Large Current Account Deficits May Be A Source Of Vulnerability (Emerging market country current accounts in 2006; percent of GDP)

Inward Capital Flows to India and China Are Also Surging (Billions of U.S. dollars) Emerging Asia excluding China and India Emerging Asia India China

Critical Challenges for the Global Economy • Coming in for a soft landing? • Bumps in the runway: • The U.S. housing market • Inflation concerns and the oil market • Financial risks facing emerging markets • Longer-term Challenges: • Unwinding global imbalances • Sustaining global productivity growth

Global Imbalances Have Widened (Percent of GDP) United States Saudi Arabia Oil trade Net income Oil trade Net income Current account Non-oil trade Non-oil trade Current account Euro Area China Non-oil trade Non-oil trade Current account Current account Net income Oil trade Oil trade Net income

U.S. Dollar Has Depreciated, But No Real Appreciation in Key Surplus Countries U.S. dollar(2000=100) Euro Yen Renminbi

Global Imbalances Are Likely to Remain Large (Percent of GDP) United States Saudi Arabia Net income Oil trade Oil trade Net income Current account Non-oil trade Non-oil trade Current account Euro Area China Current account Non-oil trade Current account Non-oil trade Net income Oil trade Net income Oil trade

Net Foreign Assets (Percent of world GDP) Emerging Asia Japan Oil Exporters euro area United States

Meeting U.S. Financing Needs (Four-quarter moving average; percent of GDP) Foreign private sector Foreign official sector

Adjustment of Global Imbalances— How Could India Be Affected? • Smooth unwinding led by rebalancing of domestic demand remains the most likely outcome • Potential for “disorderly adjustment”—rapid movement in exchange rates worldwide, volatile financial conditions • Demand rebalancing in the United States could imply a prolonged period of sub-par global growth • Risk of rising protectionist pressures

Critical Challenges for the Global Economy • Coming in for a soft landing? • Bumps in the runway: • The U.S. housing market • Inflation concerns and the oil market • Financial risks facing emerging markets • Longer-term Challenges: • Unwinding global imbalances • Sustaining global productivity growth

World GDP Growth Remains at the Fastest Sustained Pace Since the Early 1970s (Annual percent change) Trend, 1970–2005

Global Productivity Has Accelerated Led by Emerging Market Countries (Annual percent change; three-year moving average)

And China, India, and Emerging Europe Have Been in Front (Annual percent increase; three-year moving average) 1 Excludes China and India.