Download

1 / 13

130 likes | 216 Views

For professional clients only. Not for distribution to retail clients. The Growth in retail demand for AlternativeS. The growth in RETAIL demand for alternatives. What is the rationale for increased retail demand for alternatives ? Is it a temporary phase or a secular growth trend ?

E N D

For professional clients only. Not for distribution to retail clients. The Growth in retail demand for AlternativeS

The growth in RETAIL demand for alternatives • What is the rationale for increased retail demand for alternatives? • Is it a temporary phase or a secular growth trend? • Satisfying retail demand for alternative investments: • AlternativeUCITS– Europe, Latin America, Asia • Offshore Hedge Funds post-AIFMD – a “regulatory stamp of approval” ? • 40 ACT – accessing retail and DC investors in the US • Regulatory and Operational considerations • Distribution considerations in different regulatory regimes

Rationale for RETAIL demand for alternativeS • Fixed Income? “Duration can damage your wealth!” • Capital loss on 100bp and 200bp rise in rates in US TREASURIES* ‘Traditional’ asset classes are risky • Equities? • MSCI Europe down -43% in 2008….needed +76% to recover capital position! BETA CAN SERIOUSLY DAMAGE YOUR WEALTH DURATION CAN DAMAGE YOUR WEALTH • Cash? • Locking in Negative Real Returns • Guaranteed to have less spending power in retirement • * Source: Old Mutual/Factset. Data as as 30/11/2012

Temporary phase or a secular growth trend ? Demand curve has shifted • Demographic trends – “Baby boomers” moving from ‘accumulation phase’ to ‘consolidation’/’preservation phase’ as approach/reach retirement • Need for products which limit drawdown risk • Alternatives are a very small percentage of most portfolios Supply curve has shifted • Previously Alternatives were the perquisite of the upper classes • “Hedge Funds are bought by rich people and dead rich people” • i.e. High Net Worths and Endowments • “Liquid Alternatives” have “democratised” hedge funds • i.e. broadened access to this method of seeking superior risk-adjusted returns • Hedge Fund ‘manufacturers’ realising the business benefit of providing Liquid Alternatives

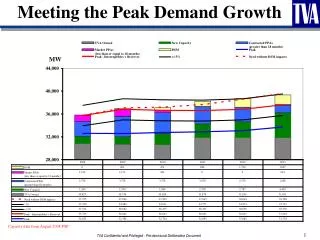

“Alternative UCITS” – Europe, Latin America, Asia • Alternative UCITS growing at 40% CAGR since 2008 to Euro 236 Billion in June 2014* • vs. CAGR of just 2% for UCITS industry overall, 13% for Hedge Funds* • If CAGRs continue “Alternatives UCITS” could be Euro 1.27 Trillion by 2019 i.e.14% of entire UCITS market* • Regulatory & Operational considerations • Most, but not all, strategies fit – e.g. commodities, distressed debt • Need Diversified and Liquid – ‘5/10/40 rule’, strong preference for Daily Liquidity • Distribution considerations • Platform vs self-sponsored • Domicile: Luxembourg, Dublin, other ? • Private Banks & Wealth Managers key drivers of demand • Requirement for Track Record (3yr+) and critical mass (Euro 100mm+) • Distribution agreements • ‘Cannibalisation’ risks, • Performance Fees • *Source: Deutsche Bank, Sept 2014

AUM in Old Mutual Global Equity Market Neutral Alternative UCITS fund • Source: OMGI Finance • Past performance is not a guide to future performance. The value of investments can go down as well as up and is not guaranteed.

“Alternative UCITS” – Europe, Latin America, Asia • Example of UCITS Investor base: Old Mutual Global Equity Absolute Return Fund, June 2014 By Country • Source: OMGI Finance

“Alternative UCITS” – Europe, Latin America, Asia • Example of UCITS Investor base: Old Mutual Global Equity Absolute Return Fund, June 2014 By INVESTOR TYPE • Source: OMGI Finance

Offshore Hedge Funds post-AIFMD - a “regulatory stamp of approval” ? • Did some politicians want to regulate the “locusts” out of existence ? • Regulatory and operational considerations • Full range of hedge fund strategies possible • AIFMD did not unduly handicap hedge funds (e.g. by limiting leverage) • Has AIFMD had an unintended consequence? • a “regulatory stamp of approval” for offshore hedge funds ? • Distribution considerations • ‘Reverse Inquiry’ regimes in Europe have been tightened up • Requires much more administration hassle for Platforms, end-Investors vs UCITS • “Regulatory stamp” not yet a market perception But: • Funds of One/Managed Accounts can solve governance and transparency concerns • North America / Institutions >60% of Hedge Fund AUM – need/prefer Offshore HFs • “$1 million net worth, income of $200,000” Accredited Investor definition: 2014 vs. 1933 • Avoiding hedge funds = negative selection bias

40 ACT – Accessing US Retail & DC PLAN Investors Funds that comply with the Investment Companies Act of 1940 can access the $15.7 Trillion US mutual fund industry* (circa 2x UCITS market) • Alternative Funds currently only 1% of 40 Act AUM** • Growth trajectory strong; CAGR of 33% since January 2009** • Regulatory and operational considerations • Leverage limited to 1.33x…higher leverage may be obtained via derivatives • Short-selling allowable, via tri-party arrangements • Daily liquidity is a requirement • Transparency – Quarterly, within 60 days of Quarter-end to SEC • Other straightforward requirements e.g. for diversification • Adviser/Sub-Adviser must be SEC Registered Investment Adviser • Robust operating platform with designated Chief Compliance Officer • Umbrella/Series trust vs. Stand-alone trust • *Source: SEI • **Barclays Hedge Fund Pulse, April 2014

40 ACT – accessing US RETAIL & DC PLAN investors • Distribution considerations • Allows access to non-”accredited investors” • Wide-scale marketing and advertising allowed • Marketing resources to support distribution Distribution access to: • Registered Investment Advisors (RIAs) • Wirehouses / Broker Dealer platforms e.g. Schwab OneSource, Merrill One • DC Plans • Brand • Track Record transferability • Minimum AUM “critical mass” thresholds in specific 40 Act Fund • Morningstar ratings • No Performance Fees (in practice) • Risk of cannibalisation

The growth in retail demand for alternative investments • Conclusions and questions • A Win-Win opportunity • Good for Investors • Giving Investors what they need • Good for Investment Managers • Diversifying and increasing Investor base • High margin • A note on Performance Fees • Generating truly uncorrelated alpha is hard to do • That skill is scarce, and merits premium prices • My Grandfather’s approach: “I can’t afford to buy ‘cheap’ shoes” • Funds without Performance Fees may still be “good”, even if not “optimal”

Important information Please remember that past performance is not a guide to future performance. The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Exchange rate changes may cause the value of overseas investments to rise or fall. Issued by Old Mutual Global Investors (UK) Limited (trading name, Old Mutual Global Investors), a member of the Old Mutual Group. Old Mutual Global Investors is registered in England and Wales under number 02949554 and its registered office is 2 Lambeth Hill London EC4P 4WR. Old Mutual Global Investors is authorised and regulated by the UK Financial Services Authority (“FCA”) with FCA register number 171847 and is owned by Old Mutual Plc, a public limited company limited by shares, incorporated in England and Wales under registered number 3591559. This communication is for information purposes only and does not constitute a financial promotion (as defined in the Financial Services and Markets Act 2000) or other financial, professional or investment advice in any way. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. It is distributed solely for information purposes, it does not constitute an advertisement and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments in any jurisdiction. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the document. Any opinions expressed in this document are subject to change without notice and may differ or be contrary to opinions expressed by other business areas or groups of Old Mutual Global Investors as a result of using different assumptions and criteria. Our asset allocation overlay is applied to some, but not all; Old Mutual Global Investors’ funds and is subject to interpretation based on specific fund objectives and risk tolerance as well as portfolio manager discretion. Therefore, such opinions are not necessarily reflected in Old Mutual Global Investors funds. This communication is for investment professionals only and should not be relied upon by private investors. OMGI 09_14_0065