Download

1 / 35

460 likes | 1.25k Views

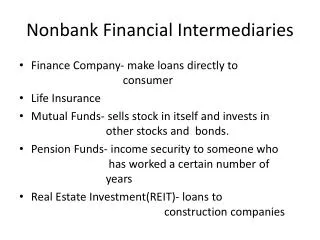

Non-Bank Financial Intermediaries. Chapter 12. Types of Intermediaries. Insurance Companies Pension Funds Finance Companies Mutual Funds Gov’t Agencies Securities Market Operations (psudeo-intermediary). Insurance Companies. 2 types Life Insurance Property/Causality Insurance

E N D

Non-Bank Financial Intermediaries Chapter 12

Types of Intermediaries • Insurance Companies • Pension Funds • Finance Companies • Mutual Funds • Gov’t Agencies • Securities Market Operations (psudeo-intermediary)

Insurance Companies • 2 types • Life Insurance • Property/Causality Insurance • Relative share of Intermediary assets decline • 1970: 19.1% • 2006: 16.6%

Life Insurance • Presbyterian Ministers Fund in Philly (1759) • Now there are 1700 companies • State Regulated: never experienced widespread failure • Adequate liquid assets • Limited risky assets • Honest sales practices

Stock and Mutual • Stock Companies, owned by stockholders, are 90% of companies • Mutual companies, owned by policy holders, are 10% of companies • However, mutuals (Met Life, Prudential) own 50% of assets in the market

Shifting Tactics • Weak returns in 1970’s forced companies to become innovative • Also 1974 legislation pushed pension funds to give management to life insurance comp • Also sell annuities, or investment vehicle similar to pension fund • Now 50% of insurance company assets

Sources/Uses • Payout statistically predictable • High yield, less liquid • Sources • High yield corporate stocks • Long term bonds • Commercial mortgages • Uses • Life insurance policies and annuities

Two type of policies • Temporary (Term) Insurance: premiums grow every year as chance of death increases • Permanent Insurance (Whole life, Universal Life): Constant premium • Accrues cash value early in life, declines later • Graph

Property/Causality Insurance • 3000 firms • Stock or Mutual • Examples: State Farm and Allstate • Regulated by states • Insure against ANYTHING for a price • Fires, malpractice, earthquakes, theft • For large risk, companies join together and co-insure

Shifting Tactics • Rates skyrocketed into the 90s • Double and triple rates, even refuse service • Low interest rates stopped flow of high investment income • Growth of lawsuits and size of awards • Elliot Spitzer • MMC and AIG, 2003-5 • Insurance broker rigging (moral hazard) • Regulation by states likely to increase

Sources/Uses • Payouts less predictable (e.g. nat. disasters) • Low yield, high liquidity • Sources • Municipal Gov’t bonds (tax-free) • U.S. gov’t bonds • More than half their assets • Uses • Policies • Reinsurance • Insure payments on bonds/securities

Insurance Issues • The downfall of the independent insurance agent • Banks • State banks entering market • Repeal of Glass-Steagal • Office of the Comptroller • Can sell annuities (20% of market) • Encourage entering to diversify

Insurance Mgmt • The Job: convert one asset into another (premiums to bonds/stocks) and then pay out claims by policyholders WHILE STILL MAKING A PROFIT • Also… • Adverse selection: those with higher insurance risk will seek it out the most • Moral Hazard: once insured, policyholder will increase risk-taking

Tools to manage risk • Screening • Adverse Selection • Gather information • Discrimination issues • Risk-based premiums • Adverse selection • Male drivers pay more • Restrictive provisions • Moral Hazard • Wear helmets on the job

More tools • Limits on Insurance • Moral Hazard • Coinsurance • Moral Hazard • Percentage amount of claim reduced • Deductible • Moral hazard • Fixed amount of claim reduced • Why a company require deductible over coinsurance? • Fraud Prevention • Moral hazard • Investigation on claims

Private Pension Funds • Relative share of intermediary assets increase • 1970: 13% • 2005: 24% • Because of employer and employee share tax deductible • Self employed open own tax-sheltered plan

Sources/Uses • Predictable payout • Sources • Employer contributions • Employee contributions • Uses • High interest bonds • Stocks • Mortgages

Stock market behemoth • Pension funds own 25% of all stock • 70% of daily volume are by pension or mutual funds • 2/3 of pension assets are in stock market

Two types • Defined contribution plan: simply get what you put in • Defined benefit: set target in advance • Fully funded or underfunded • Why would be underfunded • Companies go under and can’t make payments • Market slows down and target can’t be met

ERISA • Disclosure of Information • Regulation by Dept. of Labor • Rules on investment • Vesting: length of time someone must be enrolled to receive interest (to have a vested interest) • Created Penny Benny (like FDIC) • $45 Billion underfunded (GM $12 billion) • Currently insures 1/3 of workers • Moral Hazard

Public Pension Plans • Similarly handled as private • EXCEPT for Social Security • Sources • FICA: Income taxes • Uses • Pensions • Medicare • Disability pensions

Problem • Underfunded by $1 trillion • Pay-as-you-go system (not invested) • Created as way around market shocks (Roosevelt) • Excess goes to gov’t bonds • Working/Retiree ratio decline • Was 17/1 • Now closer to 3/1 • Solutions: Higher tax deductions, lower pensions, or privatization

Finance Companies • Make specialty, highly ‘tailored’ loans • Virtually unregulated, gain advantage over banks • % of Intermediary market • 1970: 4.9% • 1990: 5.9% • 2005: 3.9%

Sources/Uses • Sources • Company issued stocks, bonds, and commercial paper • Uses • Sales Finance • Owned by company • Auto industry • Business Finance • Lease capital (planes, construction equipment) • Factoring: purchasing accounts receivable at a discount • Consumer Finance • Lender of last resort (high interest rates) • Particular consumer items

Mutual Funds • Pool resources of small investors to buy securities • Regulated by the SEC • Many of same companies as life insurance/inv. banking • In 1960 • 3% of financial intermediary assets • Only 6% of households owned a MF • Today • 25% of financial intermediary assets • 50% of households own MFs • Households hold 80% of MF

Sources/Uses • Sources • Sell shares to investors • Two types • Open-ended: redeemed any time • Closed-ended: traded like stock • OE more common • Uses • Buy high yield securities

Advantages • Institutional Investors • Expertise • Have cloud in market • Can afford to investigate, monitor (AS) • Can even force changes inside companies • Small investors can • Lower their transaction costs • Diversify

Disadvantages • Moral Hazard • Excessive risk taking • Favored customers/insider trading • Until 2003, untainted record • Spitzer again (late hour trading) • “Betting on the horse race after the horses have crossed the finish line”

Load vs.. No-load • No-load funds • Commission (0.5%) of asset value per year • Most common (obviously) • Load funds • Additional commission paid up-front to broker

Money Market Mutual Funds • Invests in low risk, short term debt instruments • T-bills • Commercial paper • Bank CDs • Shares redeemed at fixed value • Checkable deposits • 1/3 of all mutual funds

Hedge Funds • Special mutual fund for rich • Low regulation • Allows risk taking • Long term commitment • Allows strategy • High buy-in • $1 mil in assets, $200,000 in income • Federal regulation, otherwise too risky • Market neutral strategy

Federal Credit Agencies • Farm Credit Bureau • Issues securities • Makes loans to farmers • Home mortgages • FNMA (Fannie Mae), GNMA (Ginny Mae), and FHLMC (Freddy Mac) • Only Ginny Mae is actually federal • Sally Mae, student loans, private • Moral Hazard • Gov’t won’t let go under • Public vs.. Private allegiance • Small capital to asset ratio

Securities Market Operations • Not actually financial intermediary, but more like a ‘financial facilitator’ • Primary Securities • Investment Banks • Secondary Securities • Brokers • Dealers

Investment Banks • Merrill Lynch, Goldman Sachs, etc • Two jobs • Give advice on investment tool and price • Seasoned issue • IPO (Tech stocks, China) • Underwrite security • Guarantee price to corporation then sell it on the market for more • Joint underwriting for large issues • Moral Hazard

Brokers, Dealers, and Specialists • Brokers :Agents for investors in security deals • Dealers: Holder of securities that links buyers and sellers (higher risk) • Specialist: Dealer/Broker • Brokerage Firms: perform brokerage, dealing, and investment banking (Merrill Lynch) • Organized exchanges is where activity takes place • Internationalization • Technology