Download

1 / 2

20 likes | 35 Views

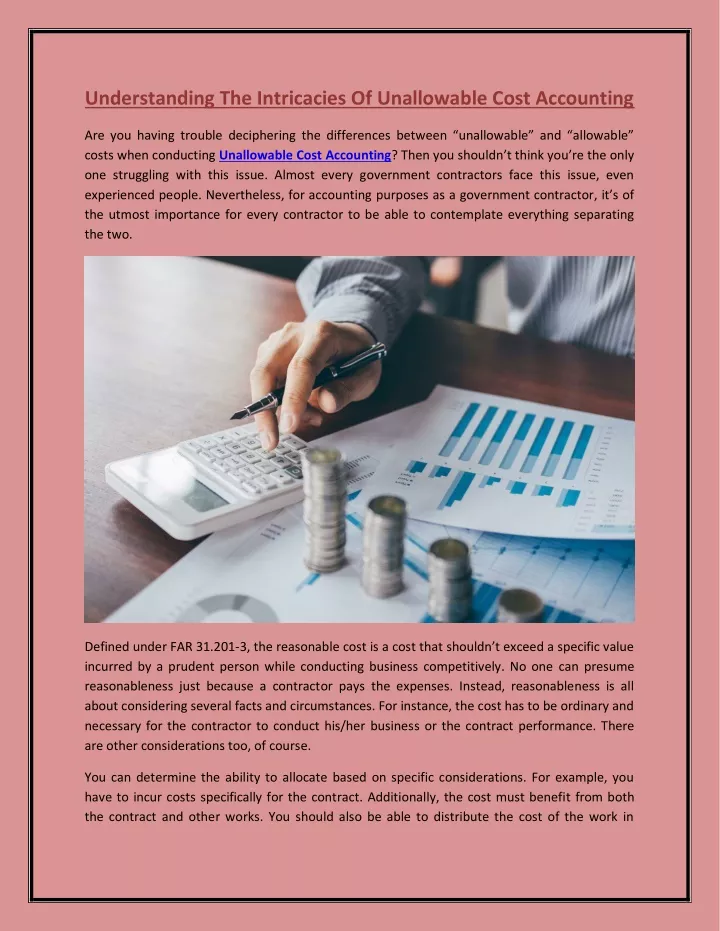

Are you having trouble deciphering the differences between u201cunallowableu201d and u201callowableu201d costs when conducting Unallowable Cost Accounting? Then you shouldnu2019t think youu2019re the only one struggling with this issue. Almost every government contractors face this issue, even experienced people. Nevertheless, for accounting purposes as a government contractor, itu2019s of the utmost importance for every contractor to be able to contemplate everything separating the two.

E N D

Understanding The Intricacies Of Unallowable Cost Accounting Are you having trouble deciphering the differences between “unallowable” and “allowable” costs when conducting Unallowable Cost Accounting? Then you shouldn’t think you’re the only one struggling with this issue. Almost every government contractors face this issue, even experienced people. Nevertheless, for accounting purposes as a government contractor, it’s of the utmost importance for every contractor to be able to contemplate everything separating the two. Defined under FAR 31.201-3, the reasonable cost is a cost that shouldn’t exceed a specific value incurred by a prudent person while conducting business competitively. No one can presume reasonableness just because a contractor pays the expenses. Instead, reasonableness is all about considering several facts and circumstances. For instance, the cost has to be ordinary and necessary for the contractor to conduct his/her business or the contract performance. There are other considerations too, of course. You can determine the ability to allocate based on specific considerations. For example, you have to incur costs specifically for the contract. Additionally, the cost must benefit from both the contract and other works. You should also be able to distribute the cost of the work in

reasonable proportions to the benefits received. Finally, the cost has to be mandatory for the business’s operation. However, you can’t show a direct relationship to a specific cost objective. More about unallowable costs According to a DCAA Accounting expert,the terms included in the contract may have specifically unallowable costs. Every contractor has to review their prime and subcontracts thoroughly to ensure they know which costs are unallowable. In doing so, they can refine their accounting chores concerning unallowable expenses. For instance, a contract may require the staff members of the contractor to work at a government-controlled site. However, the contract may assume that the members are local. Understandably, the government will include travel-related expenses among unallowable costs. Now, you may be wondering what happens to the unallowable costs. Well, explicitly unallowable costs or mutually agreed-upon unallowable costs require identification and exclusion from all billings, claims, or proposals that apply to a government contract. At this point, you should have a basic understanding of the subject. If not, speak to your accounting service provider about it.