Download

1 / 7

70 likes | 203 Views

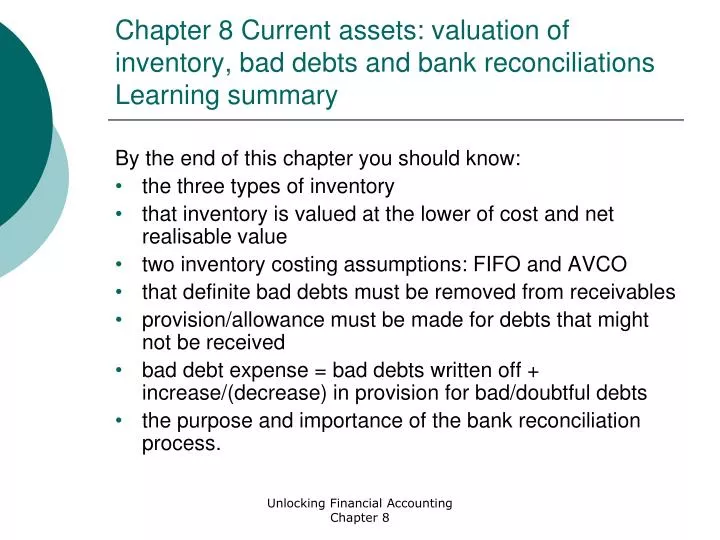

Chapter 8 Current assets: valuation of inventory, bad debts and bank reconciliations Learning summary. By the end of this chapter you should know: the three types of inventory that inventory is valued at the lower of cost and net realisable value

E N D

Chapter 8 Current assets: valuation of inventory, bad debts and bank reconciliationsLearning summary By the end of this chapter you should know: • the three types of inventory • that inventory is valued at the lower of cost and net realisable value • two inventory costing assumptions: FIFO and AVCO • that definite bad debts must be removed from receivables • provision/allowance must be made for debts that might not be received • bad debt expense = bad debts written off + increase/(decrease) in provision for bad/doubtful debts • the purpose and importance of the bank reconciliation process. Unlocking Financial Accounting Chapter 8

Inventory • Three types of inventory: • raw materials • work in progress • finished goods. • Two possible assumptions in costing inventory: • FIFO (first in, first out): assumes the units of inventory that the company buys first are sold first. • AVCO (average cost): values units at an average of recent cost prices. Unlocking Financial Accounting Chapter 8

Net realisable value • Inventory should be valued in the accounts at the lower of cost and net realisable value (NRV). • NRV = the price which the inventory is now expected to fetch, minus all expenses needed to complete the sale. Unlocking Financial Accounting Chapter 8

Receivables and bad debts • Receivables: amounts due from customers. • Bad debts: where it is highly unlikely that an amount will be received then that debt is known as a bad debt. • Bad debts must be written-off (removed from receivables). • Doubtful debts: where the eventual payment by the customer is possible, but there is some doubt. • Doubtful debts remain in receivables but a provision (or allowance) must be made. Unlocking Financial Accounting Chapter 8

Example of bad and doubtful debts X has total receivables of £900. A customer who owes £100 has just gone bankrupt. There is doubt over 10% of the remaining debts. There was a provision for doubtful debts of £50 last year. Solution: Unlocking Financial Accounting Chapter 8

Bank reconciliation • Involves checking the information on the bank statements against the information in the accounting records. • Is a vital control procedure to identify errors and omissions. • Once all errors have been corrected, a bank reconciliation statement is produced. Unlocking Financial Accounting Chapter 8

Example of a bank reconciliation statement Unlocking Financial Accounting Chapter 8