Download

1 / 13

160 likes | 294 Views

Inventory accounting. Maintained at Cost Maintained at retail value @Cost FIFO/LIFO For goods whose market value is not fluctuating Eg:Cars,durables. @Retail Maintained at retail value Accounts for markdowns and adjustments to prevailing market prices Suitable for hi fashion goods

E N D

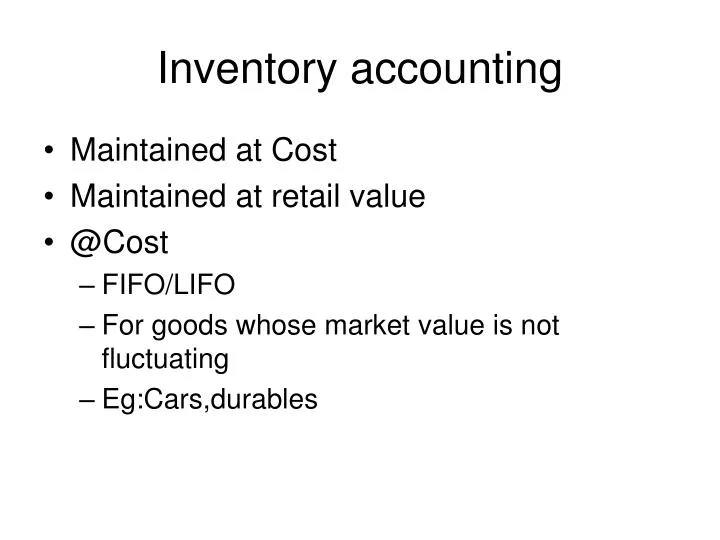

Inventory accounting • Maintained at Cost • Maintained at retail value • @Cost • FIFO/LIFO • For goods whose market value is not fluctuating • Eg:Cars,durables

@Retail • Maintained at retail value • Accounts for markdowns and adjustments to prevailing market prices • Suitable for hi fashion goods • Fashion garments , jewellery

@Cost • Easy to maintain • Inventory can be tracked daily by book entry • Physical inspection may give a diff pic • EOM Inv=BOM inv@cost+Purch –Sales@Cost

@ Retail value • 3 steps • Calculate cost component • Calculate deductions from ret sales value • Converting retail value of inv to cost

Sample Exercise for calculation The above is done @beginning of the month

Merchandise Forecasting and Budgeting • Sales forecasting (At decision unit level) • Could be category , sub category or SKU • Estimate Planned reductions • Planned markdowns • Planning Purchases to be made

Sales forecasting BASIC STOCK METHOD Beg of month planned inv= planned mth sale +Basic stock(@retail)

Inventory level planning • Percentage variation method • Week’s supply method • Avg week’s sale * no of weeks to be stocked • Stock to Sales ratio • Maintaining stock as a ratio of sales @retail value

Step II – Planning for permanent, regular reductions • Markdowns for price correction • Discounts given to Employees, senior citizens etc • Pilferage/Errors • Planned markdowns have to estimated as annual amount then indexed monthly

Step III Planning Purchases Planned Pur(@Ret)= Planned Sales (@Ret) +Planned reductions +Planned closing stock(@Ret) -Planned Opening Stock(@Ret) Open to Buy =( Planned Pur-Actual Pur)*Cost Component Open to buy is always recorded at Cost not retail

Inventory Control Systems • Unit control Systems • Maintains physical stock in units • Physical Inventory Systems • Maintains physical stock in value terms • Perpetual Inventory Systems • Continuous maintenance of records through entries for sales/returns and reductions

Measurement • Inventory Turnover • Sales to Stock ratio • Gross Margin Ratio • GMROI

Financial assessment of Retail business • Asset Turnover = Net sales / Total assets • Ret on Assets=NPAT/Total assets • Net worth= (NA- NL) • Fin leverage = Net Assets/Net worth • Strategic Profit Model= NP Margin *Asset TO*Fin leverage = Return on Networth