Download

1 / 1

20 likes | 204 Views

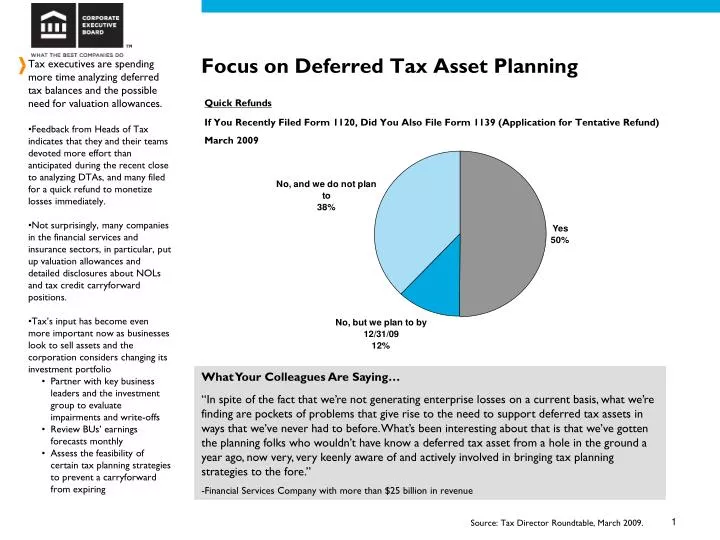

Focus on Deferred Tax Asset Planning. Quick Refunds If You Recently Filed Form 1120, Did You Also File Form 1139 (Application for Tentative Refund) March 2009. Tax executives are spending more time analyzing deferred tax balances and the possible need for valuation allowances.

E N D

Focus on Deferred Tax Asset Planning Quick Refunds If You Recently Filed Form 1120, Did You Also File Form 1139 (Application for Tentative Refund) March 2009 • Tax executives are spending more time analyzing deferred tax balances and the possible need for valuation allowances. • Feedback from Heads of Tax indicates that they and their teams devoted more effort than anticipated during the recent close to analyzing DTAs, and many filed for a quick refund to monetize losses immediately. • Not surprisingly, many companies in the financial services and insurance sectors, in particular, put up valuation allowances and detailed disclosures about NOLs and tax credit carryforward positions. • Tax’s input has become even more important now as businesses look to sell assets and the corporation considers changing its investment portfolio • Partner with key business leaders and the investment group to evaluate impairments and write-offs • Review BUs’ earnings forecasts monthly • Assess the feasibility of certain tax planning strategies to prevent a carryforward from expiring What Your Colleagues Are Saying… “In spite of the fact that we’re not generating enterprise losses on a current basis, what we’re finding are pockets of problems that give rise to the need to support deferred tax assets in ways that we’ve never had to before. What’s been interesting about that is that we’ve gotten the planning folks who wouldn’t have know a deferred tax asset from a hole in the ground a year ago, now very, very keenly aware of and actively involved in bringing tax planning strategies to the fore.” -Financial Services Company with more than $25 billion in revenue Source: Tax Director Roundtable, March 2009.