Download

1 / 8

90 likes | 317 Views

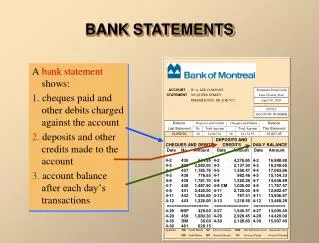

CHAPTER 11 BANK STATEMENTS I.E. UPDATING THE CASH BOOK AND BANK RECONCILAIATION STATEMENTS. Bank statements. A bank statement is a copy of the bank’s record of a customer’s transactions with the bank. It is sent to the customer periodically by the bank.

E N D

CHAPTER 11 BANK STATEMENTS I.E. UPDATING THE CASH BOOK AND BANK RECONCILAIATION STATEMENTS

Bank statements A bank statement is a copy of the bank’s record of a customer’s transactions with the bank. It is sent to the customer periodically by the bank. This should be compared with the customer’s cash book. R. Delaney

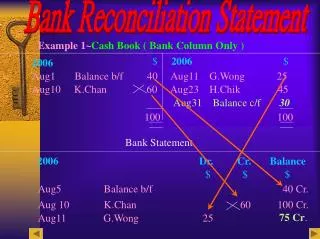

Comparing Bank Statements with Cash Book When comparing the bank statement with the cash book you should draw up two lists: A list of the items that are in the bank statement that are not in the cash book. This is used to bring the cash book up to date A list of the items that are in the cash book that are not in the bank statement. This is used to draw up the Bank Reconciliation Statement R. Delaney

Example: Question No. 6 page 112 The list of the items that are in the bank statement but not in the cash book 3rd. Direct Debit ESB, €95 (Dr) 7th. Paypath €1,000 (Cr) 9th. Credit transfer €500 (Cr) 12th. Bank charges €15 (Dr) The debit items are entered on the credit side of the Cash Correction A/C (Updated Cash Book) while the credit items are entered on the debit side R. Delaney

Cash Correction A/C or Updating the Cash Book • 1st Closing balance as per cash book €2,435 • 3rd. Direct Debit ESB, €95 (Dr) • 7th. Paypath €1,000 (Cr) • 9th. Credit transfer €500 (Cr) • 12th. Bank charges €15 (Dr) 1 Balance as per cash book €2,435 3 DD ESB €95 7 Paypath €1,000 12 Bank charges €15 €3,825 9 CT €500 14 Correct cash bal €3,935 €3,935 R. Delaney

Bank Reconciliation Statement (1) The list of the items that are in the cash book but not in the bank statement 10th. Cheque No. 3 €350 12th. Cheque No. 4 €215 14th. Lodgement €1,000 R. Delaney

Bank Reconciliation Statement (1) 14th. Lodgement €1,000 10th. Cheque No. 3 €350 12th. Cheque No. 4 €215 Balance as per bank statement €3,390 Plus lodgements not credited Lodgement of 14th €1,000 €4,390 Less cheques not yet presented Cheque No. 3 €350 Cheque No. 4 €215 €565 Correct cash balance €3,825 R. Delaney

Bank Reconciliation Statement (2) 14th. Lodgement €1,000 10th. Cheque No. 3 €350 12th. Cheque No. 4 €215 Correct cash balance €3,825 Less lodgements not credited Lodgement of 14th €1,000 €2,825 Plus cheques not yet presented Cheque No. 3 €350 Cheque No. 4 €215 €565 Balance as per bank statement €3,390 R. Delaney