Download

1 / 13

130 likes | 145 Views

Economics. El Dorado High School Spring, 2015 Mr. Ruiz. Economics Chapter One. What is Economics? Section One : Scarcity and the Factors of Production Section Two : Opportunity Cost Section Three : Production Possibilities Curve. Key Terms to Remember throughout This Chapter. Economics

E N D

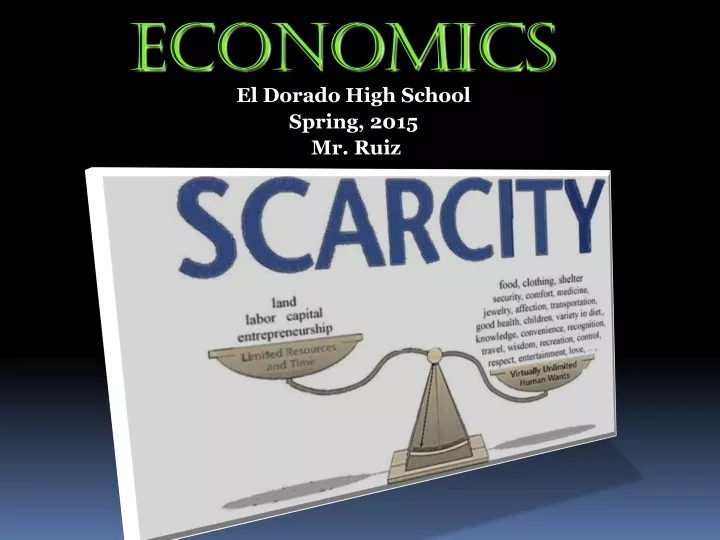

Economics El Dorado High School Spring, 2015 Mr. Ruiz

EconomicsChapter One What is Economics? Section One: Scarcity and the Factors of Production Section Two: Opportunity Cost Section Three: Production Possibilities Curve

Key Terms to Remember throughout This Chapter • Economics • Needs • Wants • Scarcity • Shortage • Goods • Services • Factors of Production • Land • Labor • Capital • Human Capital • Physical Capital • Entrepreneur • Trade-off • Guns or Butter • Opportunity Cost • Thinking at the Margin • Production Possibilities Curve (PPC) • Production Possibilities Frontier • Efficiency • Underutilization • Cost • Law of Increasing Costs

Section 1: What is Economics? • Economics is the study of how people seek to satisfy theirneeds and wants by making choices. Needs vs. Wants: • Needs:Things that are necessary for survival. (Water, air, food, shelter) • Wants:Things not essential for survival. (IPod, TV, cell phone, Xbox, etc..)

The Economic Perspective(The economic way of thinking) • Scarcity and Choice: • Human/property resources are scarce. • Goods and services we produce must also be limited, “We can’t have it all.” • We must decide what we will have and what we must forgo. • The economic axiom, “ There is no free lunch.”

Scarcity vs. Shortage • Scarcity: There are limited quantities of resources to meet unlimited wants. Limited quantities vs. Unlimited wants • All the goods(physical objects) and services ( actions or activities performed) that are produced are scarce. • Scarcity vs. Shortage • Shortage occurs when production of goods/services will not or cannot be provided at the same price; can be temporary or long term. • On the other hand, scarcityexist when needs/wants exceed the resource supply.

Factors of Production:The (3) groups of resources used to make all goods and services (aka, Factor resources) • Land • Labor • Capital • Natural resources (water, forests, coal, etc..) • Efforts devoted by people to a task for compensation (payment) • Human made resources used to produce other goods/services • (2) categories: • Physical capital: Buildings, tools, & machinery • Human capital: Knowledge & skills gained through education & experience

Entrepreneurs • Entrepreneur: Ambitious individuals willing to combine the factors of production (land,labor, & capital) to create new goods and services

Opportunity cost: The most desirable alternative given up as a result of a decision. Example: Buying new shoes instead of going to the movies and dinner. The opportunity cost is the movies/dinner. Guns or Butter: Concept that explains the trade-offs countries may face. ( A country that decides to apply its resources for more military goods (guns) will sacrifice its resources devoted to consumer goods (butter) and vice versa. Section 2:Opportunity Cost Retrieved from: http://www.investopedia.com/terms/g/gunsandbutter.asp

Trade-Offs & Thinking at the Margin • Trade-Offs: • The alternatives that we give up whenever we choose one course of action over another. • Example: If you spend more time at work, you give up spending time with your friends and/or going to see a movie. • Thinking at the Margin: • Deciding and whether to do or use one additional unit of some resource • Good example provided (Figure 1.3, pg. 11) : One hour extra study time =C Two hours extra study time =B Three hours extra study time=A

Production Possibilities Curve • Production Possibilities Curve (Graph) PPC: • Basically, shows alternative ways to make use of an economy’s resources; it help relate, (compare) the value of one thing from the value of another. • An example of PPC with point A reflecting the area that is unattainable. • The blue line on the graph displaying the possible combinations is know as the Production Possibilities Frontier.

Efficiency, Growth, and Cost • The PPC graph may point out vital information regarding the status of any given economy: • It can identify if the efficiency of an economy’s resources are being maximized in the production of goods and services or recognize an economy’s underutilization of resources ( i.e., any point inside the frontier line). • It can also identify unattainable production as a result of limited resources • It can recognize economic growth by an entire shift to the right of the PPC • It can help illustrate the cost (not in money, but in opportunity cost) of the decisions made with regards to the use of resources.

Rational behavior in a world ruled by scarce resources and opportunities? “It doesn’t have to end like this!”