Download

1 / 21

220 likes | 423 Views

Chapter 20 Asymmetric Information and Market Behaviour. Asymmetric Information. This Chapter examines cases of asymmetric (differing) information in market exchanges.

E N D

Asymmetric Information • This Chapter examines cases of asymmetric (differing) information in market exchanges. • The goal is to predict how exchanges will be organized to best manage the subsequent transaction cost problems that arise when buyers and sellers have different information.

Sunk Costs • An interesting feature of the role of reputations is that they involve sunk assets (costs). • It is the actual commitment of a real resource that demonstrates goodwill. • With asymmetric information, the fact that sunk costs do not affect the level of output makes them the optimal method of developing a reputation.

The Hold-Up Problem • Whenever there is a large sunk cost (investment) involved in an exchange, there is the threat of a hold-up problem (customers or suppliers attempting to appropriate rents).

Vertical Integration and Long-Term Contracts • Two general solutions to the hold up problem are: • Vertical integration - a firm buying another firm that supplies its inputs or markets its outputs. • Long-term contracts-where firms contractually agree to a price for the entire life of the relationship.

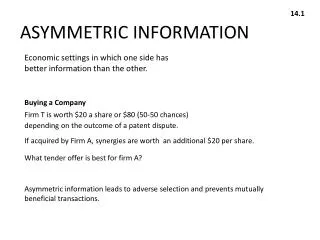

Adverse Selection • Adverse selection occurs when two parties have different information. • For example, the selection of people who purchase insurance is biased in favour of those who need it the most. • Sick people are more likely to apply for health insurance than are healthy people, but this characteristic may be hidden from the insurer.

Hidden Characteristics • Three assumptions are made in the analysis of the insurance industry: • The probability of loss from a collision is not uniform across drivers. • Each driver is completely informed about his/her own characteristics. • The driving characteristics of an individual (high/low risk) are hidden from the insurance company.

Full-Information Equilibrium • When identifying risk characteristics is prohibitively expensive, if all drivers buy insurance, low-risk drivers pay more than the equilibrium and high-risk drivers pay less. • Low-risk drivers subsidize insurance for high-risk drivers.

Full-Information Equilibrium • If the proportion of high-risk drivers is not too high, then in equilibrium, all drivers buy insurance and the low risk drivers subsidize the high risk drivers. • If the proportion of high-risk drivers is too large, then in equilibrium, only high-risk drivers will buy insurance, and low-risk drivers will be forced out of the market.

The Lemons Principle • Assume there are only two types of used cars, lemons and jewels, and that ascertaining whether a given car is a lemon or a jewel is prohibitively costly. • All persons who want to sell their cars put them on the market, so the price of a used car reflects the mix of lemons and jewels for sale.

The Lemons Principle • Some owners who want to sell their jewels at a “fair price” may decide not to sell at the market price (which includes lemons). • As a result the proportion of lemons on the market rises, further depressing the market price, and inducing other jewel owners to withdraw from the market.

The Lemons Principle • If all jewel owners make this choice, there will a market for lemons but not jewels. • Because of this hidden characteristic, the jewels are driven out of the market by the lemons (the lemon principle).

Signalling • Adverse selection is not a hopeless problem. Individuals who are disadvantaged can respond by signalling. • Signallingis a way for low-risk drivers to identify themselves to insurance companies. • One way to signal is to have some form of low-risk certification.

Low Risk Certification • If the certificate is to produce an equilibrium, 3 conditions must hold: • Insurance companies must be convinced the certificate does signal low risk. • The cost to low-risk drivers must be low enough so they have an incentive to acquire it. • The cost to high-risk drivers must be high enough so they have no incentive to acquire it.

Signalling Equilibrium • If it is very costly for high-risk drivers to obtain the signal and not too costly for low-risk drivers, then there will be a signalling equilibrium in which low-risk drivers acquire the signal in order to differentiate themselves from high-risk drivers and obtain a lower insurance rate.

Moral Hazard Problems: Hidden Action • Moral hazard comes from the insurance industry, where the probability of an accident increased when it was insured. • People are less careful when they are insured for loss.

Moral Hazard Problems: Hidden Action • Suppose all drivers are identical and have the same probabilistic loss (L). • If the driver spends some amount (C) on accident prevention, the probabilistic loss of L is reduced from q to q’. • The problem is that spending on C cannot be observed by insurance companies (it is hidden).

Moral Hazard Problems: Hidden Action • If all individuals could credibly promise to spend C on accident prevention, the price of full coverage would be q’L and he/she would be better off. • But, since the action is hidden, the promise is not credible, and the insurance companies will not offer insurance at this price.

Deductibles • One way for the insurance company to solve this moral hazard problem is through the use of deductibles. • Deductible means that the insured individual must pay some fraction of the cost of the accident. • This effectively prevents the person from having full insurance and people are willing to bear some costs (being more careful) to avoid having to pay the deductible.