Download

1 / 6

60 likes | 67 Views

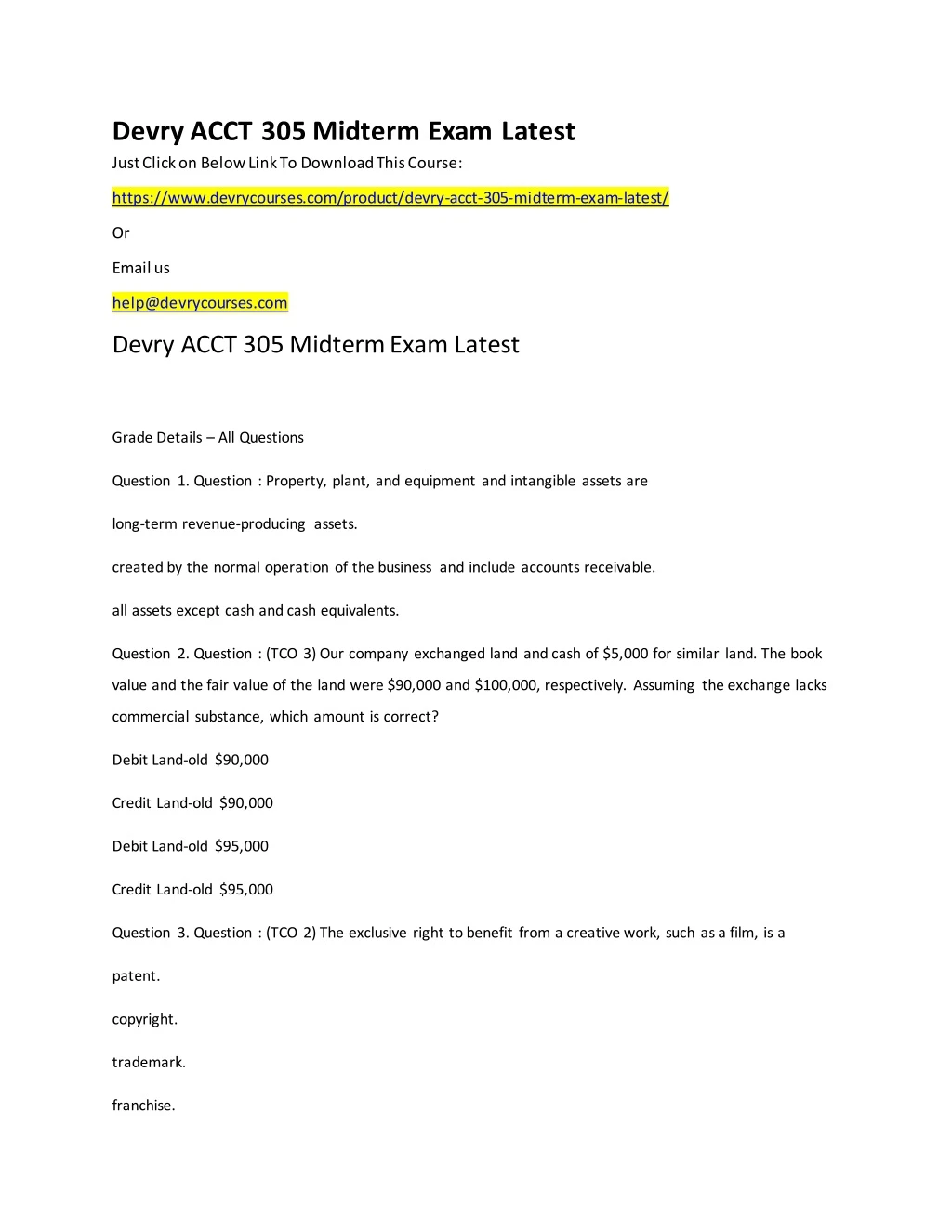

Just Click on Below Link To Download This Course:<br>https://www.devrycourses.com/product/devry-acct-305-midterm-exam-latest/<br>Devry ACCT 305 Midterm Exam Latest<br> <br>Grade Details u2013 All Questions<br>Question 1. Question : Property, plant, and equipment and intangible assets are<br>long-term revenue-producing assets.<br>created by the normal operation of the business and include accounts receivable.<br>all assets except cash and cash equivalents.<br>

E N D

Devry ACCT 305 Midterm Exam Latest Just Click on Below Link To Download This Course: https://www.devrycourses.com/product/devry-acct-305-midterm-exam-latest/ Or Email us help@devrycourses.com Devry ACCT 305 Midterm Exam Latest Grade Details – All Questions Question 1. Question : Property, plant, and equipment and intangible assets are long-term revenue-producing assets. created by the normal operation of the business and include accounts receivable. all assets except cash and cash equivalents. Question 2. Question : (TCO 3) Our company exchanged land and cash of $5,000 for similar land. The book value and the fair value of the land were $90,000 and $100,000, respectively. Assuming the exchange lacks commercial substance, which amount is correct? Debit Land-old $90,000 Credit Land-old $90,000 Debit Land-old $95,000 Credit Land-old $95,000 Question 3. Question : (TCO 2) The exclusive right to benefit from a creative work, such as a film, is a patent. copyright. trademark. franchise.

Question 4. Question : (TCO 4) The overriding principle for all depreciation methods is that the method must be systematic and rational. conservative and economic. consistent and conservative. significant and material. Question 5. Question : (TCO 4) On September 30, 2013, our company purchased a machine for $100,000. The estimated service life is 10 years, with a $10,000 residual value. Our company records partial-year depreciation based on the number of months in service.Depreciation for 2013, using double-declining balance, would be $20,000. $5,000. $18,000. $4,500. Question 6. Question : (TCO 4) A change from the straight-line method to the sum-of-years’-digits method of depreciation is handled as a retrospective change back to the date of acquisition as though the current estimated life had been used all along. a prospective change from the current year through the remainder of its useful life. a cumulative adjustment to income in the current year for the difference in depreciation under the new versus old useful life estimate. None of the above Question 7. Question : (TCO 5) Fair value and appreciation of the investee are not as relevant for investments in which of the following categories? Securities reported under the equity method

Held-to-maturity securities Trading securities Securities available-for-sale Question 8. Question : (TCO 5) Consolidated financial statements are prepared when one company has accounted for the investment using the equity method. control over another company. accounted for the investment as securities available-for-sale. None of the above Question 9. Question : (TCO 4) Interest is not capitalized for inventories routinely and repetitively produced in large quantities. assets that are constructed as discrete projects for sale or lease. assets constructed for a company’s own use. None of the above Question 10. Question : (TCO 2) Goodwill is amortized over the greater of its estimated life or 40 years. amortized over 20 years. amortized over 70 years. not amortized. Question 11. Question : (TCO 4) Depreciation, depletion, and amortization all generally utilize the same methods of cost allocation. are all handled the same in arriving at taxable income. all refer to the process of allocating the cost of long-term assets used in the business over future periods. All of the above

Question 12. Question : (TCO 5) Which of the following types of securities only includes debt securities? Securities available-for-sale Held-to-maturity securities Trading securities Consolidated securities Question 13. Question : (TCO 1) The capitalized cost of equipment excludes sales tax. shipping. insurance for the first year. installation. Question 14. Question : (TCO 3) When selling property, plant, and equipment for cash the seller recognizes a gain or loss for the difference between the cash received and the fair value of the asset sold. the seller recognizes losses but not gains. the seller recognizes a gain or loss for the difference between the cash received and the book value of the asset sold. None of the above Question 15. Question : (TCO 2) Research and development (R & D) costs may be expensed or capitalized, at the option of the reporting entity. must be capitalized and amortized. generally pertain to activities that occur prior to the start of production. None of the above Question 16. Question : (TCO 4) The depreciable base for an asset is its service life.

the excess of its cost over residual value. the difference between its replacement value and cost. the amount allowable under MACRS. Question 17. Question : (TCO 5) Trading securities are most commonly found with oil companies. manufacturing companies. banks. foreign subsidiaries. Question 18. Question : (TCO 5) All investments in debt and equity securities that don’t fit the definitions of the other reporting categories are classified as trading securities. held-to-maturity securities. securities available-for-sale. consolidated securities. Question 19. Question : (TCO 5) If Company 1 exercises significant influence over Company 2 and owns 38% of its common stock, then Company 1 would record dividends received from Company 2 as investment revenue. would increase its investment account when Company 2 declares dividends. would record 38% of the net income of Company 2 as investment income each year. All of the above Question 20. Question : (TCO 2) Please explain how software development costs are treated. How is this different from other types of R & D? Question 21. Question : (TCO 4) How is a change in depreciation method accounted for?

Question 22. Question : (TCO 1) What are the costs that are included in the purchase of equipment? What costs would be excluded? Download File Now