Download

1 / 20

200 likes | 346 Views

Value Premium in International REITs ERES Conference 2014 Ytzen van der Werf and Fred Huibers 27 June 2014 y.vanderwerf@asre.nl. Outline. Introduction Aim Literature review Methodology Data Results Conclusion. Introduction . Value investing attractive for common stocks

E N D

Value Premium in International REITs ERES Conference 2014 Ytzen van der Werf and Fred Huibers 27 June 2014 y.vanderwerf@asre.nl

Outline • Introduction • Aim • Literature review • Methodology • Data • Results • Conclusion

Introduction • Value investing attractive for common stocks • Value premium internationally accepted phenomenon • Value premium = excess return from buying cheap and selling expensive stocks • Extensively researched within common equities • Latest research into question whether it is a reward for risk or rather a result of behavioural inaccuracy

Aim of this study • To find out whether: • the value premium exists for REITs in international developed markets and • whether it is a reward for risk or a behavioural phenomenon

Literature review RE • Vast number of studies into US REITs • Some find consistent value premium in US REITs for the 90’s. Gentry et al. (2004) 11-22%. Ooi et al. (2007) 8.5%. • One study into direct real estate (Addae et al. 2013). Assume properties with low initial yield are growth investments. Find value premium of 6% p.a. for offices and 8% for retail. • No study so far into non-US REITs

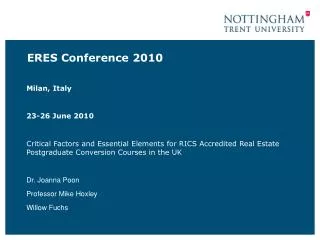

Methodology 30 June Highest Discount to NAV Book to Market multiple 1.00 Premium to NAV 0.00 Lowest

Methodology 30 June Highest Discount to NAV Book to Market multiple Q1 Q2 Q3 1.00 Premium to NAV Q4 Q5 0.00 Lowest

Methodology 30 June Highest Discount to NAV Q1 Value REITs annual portfolio return 1 July – 30 June 1.00 Premium to NAV Q5 annual portfolio return 1 July – 30 June Growth REITs Lowest

Data • International Developed REITs with viewpoint of European Investor (returns in Euro) • 23 countries with a total of 1,152 REITs • Use minimum daily trading volume of 0.5 m EUR to ensure liquidity and positive B/M

Results • Characteristics (Q1 = Value REITs) • *** significant at 1% level • Cumulative Total Returns (1,2,3 year holding) • ** significant at 5% level; *** significant at 1% level • TR1 is the average yearly return of holding a value (growth) portfolio for 1 year and then rebalance the portfolio with (possible) new REITs with high (low) book to market multiples. TR02/03 cumulative total return of 2/3 years after portfolio formation

Explanation (I) • Risk based school of thought (Fama and French) • Higher return is a reward for higher risk • Test whether volatility of value REITs is higher or whether beta within CAPM framework is higher for value stocks • * significant at 10% level • ** significant at 5% level • *** significant at 1% level

Explanation (II) • Behavioural school of thought (Lakonishok) • Higher return in value REITs is a result of naive extrapolation of results from the past to the future • Test whether growth REITs indeed show higher past performance and whether this changes after portfolio formation and vice versa • Performance measured as Total Return

Explanation (III) • Pre and post-formation total return performance • ** significant at 5% level; *** significant at 1% level

Conclusion • International developed REITs exhibit a significant value premium of 10.3% (1993-2013) compared to a 8.3% premium Ooi et al. (2007) found in US REITs (1993-2002) • Value premium is not a reward for additional risk (nor volatility or CAPM model) • Value premium seems to be a result of naive extrapolation of past performance

Average B/M • Average book value of Equity versus market value of Equity by Quintile (Q1=Value, Q5 = Growth)

Market Cap • Average Market Cap by Quintile

suggestions • Transaction costs • Net Asset Value vs Book Value of Equity • Stipulate contribution to the Literature • Keep it easy (step by step) • Controlled for difference in size?