Download

1 / 22

220 likes | 243 Views

Explore the dynamics of risk appetite in emerging markets post-2002, analyzing factors like US rates, debt crises, and capital flows. Delve into case studies like Brazil's debt burden and the impact of capital controls. Assess the shifts in creditor-debtor risks and contagion mechanisms. Is risk aversion truly a thing of the past in emerging markets?

E N D

Emerging markets: is risk aversion dead? David Lubin November 2002

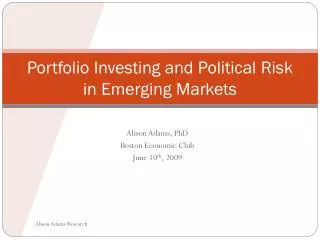

300 250 200 150 100 50 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1998 1997 1999 2000 2001 2002 Risk appetite collapsed in 2002 Total issuance of bonds, loans and equity by emerging markets (US$bn)

On what does risk appetite depend? Real US rates? Latin American debt crisis Lending boom to Latin America “Emerging markets” is born October 2001 “mini-boom”

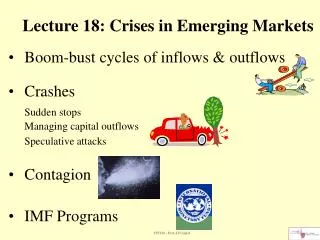

300 250 200 150 100 50 0 -50 -100 -150 -200 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 The fall in net private capital flows is long-lasting US$bn Net private direct investment Net private portfolio investment Other net private capital flows Total flows

42% 45% 36% 40% 35% 30% 25% 20% 15% 6% 10% 5% 0% Latin America Asia Europe FDI flows are at risk Privatisation as a share of total FDI flows, 1990-1999

FDI flows are at risk (cont’d) A T Kearney FDI Confidence Index Sep 02 Feb 01 Change since Feb 01 Brazil 1.1 1.5 Down Mexico 1.19 1.44 Down India 1.05 1.35 Down Poland 1.15 1.26 Down Thailand 0.93 1.21 Down Czech 1.09 1.2 Down South Korea 0.91 1.12 Down Hungary 1.02 1.02 Stable Hong Kong 0.95 0.95 Stable China 1.99 1.69 Up Russia 0.99 0.78 Up The index ranges from 0 (no confidence) to 3 Survey horizon is one to three years

200% 150% 100% 50% 0% -50% Peru Brazil China Turkey Russia Poland Mexico Uruguay Thailand Lebanon Colombia Indonesia Venezuela Philippines South Africa South Korea A measure of vulnerability Current account and amortisations (2003) divided by fx reserves (2002)

60% 50% 40% 30% 20% 10% 0% Peru Brazil China Russia Turkey Poland Mexico Thailand Colombia Indonesia Argentina Venezuela Philippines South Korea South Africa Brazil’s basic problem Exports as a share of GDP

50 0 40 -1000 30 -2000 20 10 -3000 0 -4000 -10 -20 -5000 -30 -6000 -40 Oct-00 Oct-01 Apr-00 Apr-01 Apr-02 Jun-01 Feb-00 Jun-00 Feb-01 Feb-02 Jun-02 Dec-00 Dec-01 Aug-00 Aug-01 ...it has depended on a collapse in domestic spending... Current account balance (right scale, US$ mn) Export growth (% y/y) Import growth (% y/y)

4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Jan-82 Jan-86 Jan-90 Jan-94 Jan-98 Jan-02 Jan-80 Jan-84 Jan-88 Jan-92 Jan-96 Jan-00 ...and a weak exchange rate... Brazil's inflation-adjusted exchange rate

...which makes the domestic debt burden grow... Brazil’s domestic debt Fixed rate 9% US$-linked 30% Floating rate 61%

70.00 60.00 50.00 40.00 30.00 20.00 10.00 0.00 Jun-02 Jun-98 Jun-99 Jun-97 Oct-97 Oct-99 Jun-00 Oct-00 Jun-01 Oct-98 Oct-01 Feb-99 Feb-98 Feb-00 Feb-01 Feb-02 ...creating a solvency risk % GDP Domestic debt External debt

Options for Brazil if things go wrong Capital controls? To ring-fence domestic interest rates Domestic debt restructuring? Probably not achievable without capital controls... Debt monetisation? Probably not achievable without capital controls... So: can capital controls work?

Is there ‘moral hazard’ in Turkey? IMF share of 2003-2006 external amortisations Turkey 24% Brazil 17% Can there be ‘creditor’ moral hazard without ‘debtor’ moral hazard?

200% 180% 160% 140% 120% 100% 80% 60% 40% 20% 0% 1993 1994 1995 1996 1997 1998 1999 2000 2001 Contagion mechanisms have changed Short term external debt divided by fx reserves Latin America Emerging Asia EMEA

Common creditor problems? Germany France Spain USA Turkey 28% 10% Russia 50% 6% Ukraine 31% 15% Romania 17% 24% South Africa 21% 9% Brazil 17% 24% Mexico 41% 35% Colombia 29% 25% Venezuela 37% 16% Argentina 23% 27%

160 400 140 350 120 300 100 250 80 200 60 150 40 100 20 50 0 0 Jan-98 Jan-84 Jan-86 Jan-88 Jan-90 Jan-92 Jan-00 Jan-02 Jan-80 Jan-82 Jan-94 Jan-96 Mexican peso isn’t cheap, but ability to pay is strong External debt/exports ratio, right scale Real exchange rate index, 1990=100, left scale

Emerging markets: is risk aversion dead? David Lubin November 2002