Download

1 / 18

180 likes | 335 Views

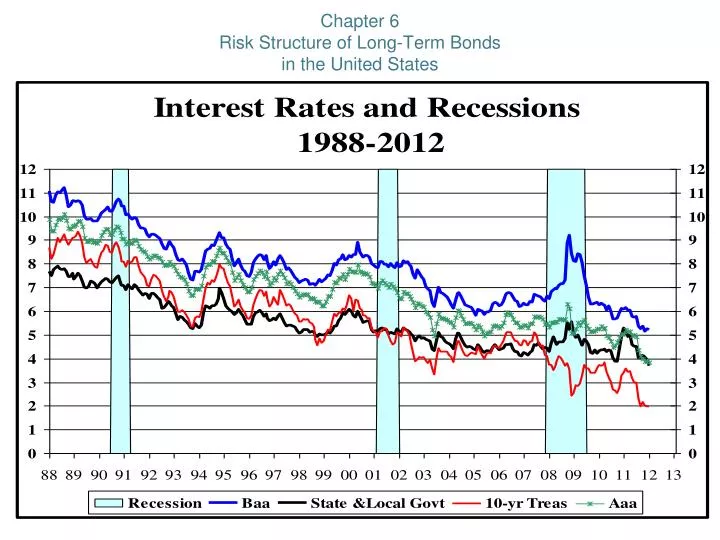

Chapter 6 Risk Structure of Long-Term Bonds in the United States. Default risk —occurs when the issuer of the bond is unable or unwilling to make interest payments or pay off the face value U.S. T-bonds are considered default free

E N D

Chapter 6Risk Structure of Long-Term Bondsin the United States

Default risk —occurs when the issuer of the bond is unable or unwilling to make interest payments or pay off the face value • U.S. T-bonds are considered default free • Risk premium—the spread between the interest rates on bonds with default risk and the interest rates on T-bonds • Liquidity—the ease with which an asset can be converted into cash • Income tax considerations

Fact 1: Interest rates for different maturities move together over time

Term Structure Facts to be Explained 1. Interest rates for different maturities move together over time 2. Yield curves tend to have steep upward slope when short rates are low and downward slope when short rates are high • Yield curve is typically upward sloping Three Theories of Term Structure 1. Expectations Theory 2. Segmented Markets Theory 3. Liquidity Premium Theory A. Expectations Theory explains 1 and 2, but not 3 B. Segmented Markets explains 3, but not 1 and 2 C. Solution: Combine features of both Expectations Theory and Segmented Markets Theory to get Liquidity Premium (Preferred Habitat) Theory and explain all facts

Fact 2: Yield Curves slope upward when short-term rates are low and downward when short-term rates are highFact 3: Yield Curves are typically upward sloping

5-year loan @ 7.5% Credit Spread Interest Rate Risk Spread Funding Spread 1-year CD @ 3.0%

Risk Sharing; Asset Transformation “Carry Trade” -Borrow short-term -Lend long-term Selling low-risk assets to fund the purchase of higher-risk assets $1 Million example (wholesale market) Borrow 1 Year at 4% ($40,000) Lend 5 Years at 6% ($60,000) Earn $20,000 5-year loan @ 7.5% Credit Spread Return Interest Rate Risk Spread Funding Spread Tradeoffs 1-year CD @ 3.0% Risk

Expectations Theory Key Assumption: Bonds of different maturities are perfect substitutes Implication:RETe on bonds of different maturities are equal Investment strategies for two-period horizon 1. Buy $1 of one-year bond and when it matures buy another one-year bond 2. Buy $1 of two-year bond and hold it Expected return from strategy 2 (1 + i2t)(1 + i2t) – 1 1 + 2(i2t) + (i2t)2 – 1 = 1 1 Since (i2t)2 is extremely small, expected return is approximately 2(i2t)

Expected Return from Strategy 1 (1 + it)(1 + iet+1) – 1 1 + it + iet+1 + it(iet+1) – 1 = 1 1 Since it(iet+1) is also extremely small, expected return is approximately it + iet+1 From implication above expected returns of two strategies are equal: Therefore 2(i2t) = it + iet+1 Solving for i2t it + iet+1 i2t = 2 More generally for n-period bond: it + iet+1 + iet+2 + ... + iet+(n–1) int = n In words: Interest rate on long bond = average short rates expected to occur over life of long bond

Example: 5 year holding period, $100 2 options: Buy 5-yr CD at 4.64%,…FV = 100*(1+.0464)5 = $125.45 Buy 1-yr CD at 4.45% and a 4-yr CD next year FV = 100*(1.0445)(1.0469)4 = $125.45 Yield to Maturity 5% 4.69 4.64 4.59 4.55 4.50 4.45 4% Term to Maturity If perfect substitutes (1+i1)(1+i4,t+1)4 = (1+i5)5 i4,t+1 = [(1+i5)5]1/4 - 1 [ 1+i1 ] i4,t+1 = [(1.0464)5]1/4 - 1 [ 1.0445 ] i4,t+1 = 4.69%

In General in,t+1 = [(1+in+1)n+1]1/n - 1 [ 1+i1 ]

Segmented Markets Theory Key Assumption: Bonds of different maturities are not substitutes at all Implication: Markets are completely segmented: interest rate at each maturity determined separately Explains Fact 3 that yield curve is usually upward sloping People typically prefer short holding periods and thus have higher demand for short-term bonds, which have higher price and lower interest rates than long bonds Does not explain Fact 1 or Fact 2 because assumes long and short rates determined independently

Segmented Markets Theory Weak Demand Yield to Maturity Strong Demand 5% 4.64 4.59 4.55 4.50 4.45 If bond maturity = holding period Then no IRR, no DPB , no uncertainty So Return = YTM = i 4% Term to Maturity 1 yr 2 yr 3 yr 4 yr 5 yr Different investors have different holding periods • Banks have S.T. holding periods • Insurance Co.s have L.T. holding periods

Liquidity Premium Theory Key Assumption: Bonds of different maturities are substitutes, but are not perfect substitutes Implication: Modifies Expectations Theory with features of Segmented Markets Theory Investors prefer short rather than long bonds must be paid positive liquidity (term) premium, lnt, to hold long-term bonds Results in following modification of Expectations Theory it + iet+1 + iet+2 + ... + iet+(n–1) int = + lnt n

Relationship Between the Liquidity Premium and Expectations Theories

Econ 330 Homework 4Due Thursday, February 20, Before Exam Chapter 6 Questions & Applied Problems 15, 17, 18, 21, 22, 23, 25