Download

1 / 6

81 likes | 277 Views

Managing Overconfidence. Douglas J. Collins, FCAS, MAAA doug.collins@towersperrin.com Tillinghast London (Tel: 44 (0)207 170 2162) CAE Zurich – 23 April 2004. Many factors contribute to errors (and bias!) in pricing and underwriting.

E N D

Managing Overconfidence Douglas J. Collins, FCAS, MAAA doug.collins@towersperrin.com Tillinghast London (Tel: 44 (0)207 170 2162) CAE Zurich – 23 April 2004

Many factors contribute to errors (and bias!) in pricing and underwriting Common Sources of Pricing and Underwriting Error/Bias (Micro) Systemic Sources of Pricing and Underwriting Error/Bias (Macro) • Inadequate internal [historical] data upon which to develop estimates (e.g., old, incomplete or inaccurate data; inadequate/inappropriate sample) • Inability to collect and synthesize all relevant sources of data within the organization • Lack of reliable information about external market conditions and trends (e.g., inflation, tort costs) • Excessive concern for “competitive pressures” • Lack of adequate oversight over pricing decisions • Lack of “metaknowledge” — reinforces inherent overconfidence when making estimates, forecasts and predictions • Long feedback loop • No skin in the game

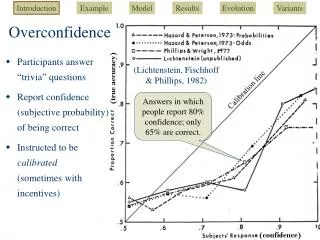

The results of a recent Tillinghast “Confidence Quiz” illustrate the prevalence of overconfidence Tillinghast Confidence Quiz The Quiz Raw Scores of Online Respondents • Objective: To test respondents understanding of the limits of their knowledge • Respondents were asked to answer ten questions related to their general knowledge of the global property/casualty industry • For each answer, respondents were asked to provide a range that offered a 90% confidence interval that they would answer correctly • Ideally (i.e., if “well calibrated”), respondents should have gotten nine out of ten questions correct Number of Respondents Note: based on 374 respondents as of 4/5/04.Profile of respondents: 86% work in P/C industry; 73% are actuaries.

1. Pricing and Underwriting Process Elements • Data required • Actuarial methods employed • Underwriting policies and rules • Decision authorities and reporting • Quality assurance 3. Formal Retrospective Performance Testing • Data accurate and adequate? • Pricing methods sufficiently robust? • Policies and rules effective? • Decision authorities appropriate? • Variances between projected and actual experience within tolerances? 1. Define/Refine Process 3. MeasurePerformance 2. ImplementProcess The best way to manage overconfidence is to implement a control cycle for pricing and underwriting The Control Cycle: Retrospective Test of Pricing/Underwriting • A control cycle for P/C pricing and underwriting entails identifying, testing and validating all of the assumptions that underlie the projection of future loss costs used to price and underwrite the business

While improving pricing/underwriting requires a sustained commitment over time, three near-term steps will jump start the process Retrospective Analysis • Analyze relevant sample of pricing and underwriting results to identify/pinpoint specific causes and sources of error Process Design/Refinement • Define (or refine) and institutionalize an ongoing process of continuous improvement (i.e., control cycle) for pricing and underwriting • Incorporate insights from retrospective analysis to address key challenges and deficiencies Case-study Training • Develop/institute case-study oriented training modules for underwriters and pricing actuaries to provide practical experience and rapid feedback • Base training materials on past business where results are already known