Download

1 / 39

390 likes | 598 Views

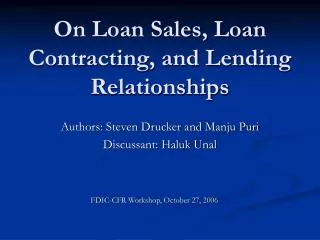

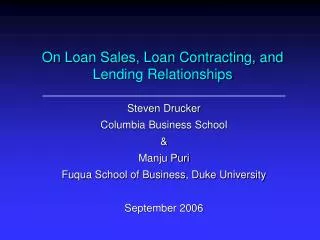

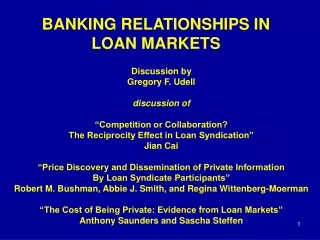

On Loan Sales, Loan Contracting, and Lending Relationships. Steven Drucker Columbia Business School & Manju Puri Fuqua School of Business, Duke University September 2006. Screening. Loan Seller. Upfront Fees. Borrower. Interest Payments. Loan Buyer. Monitoring, Funding.

E N D

On Loan Sales, Loan Contracting, and Lending Relationships Steven Drucker Columbia Business School & Manju Puri Fuqua School of Business, Duke University September 2006

Screening Loan Seller Upfront Fees Borrower Interest Payments Loan Buyer Monitoring, Funding Screening, Monitoring, Funding Borrower Lender Upfront Fees, Interest Payments Motivation • Loan selling is important for banks and the economy • Trading Volume: $154.8 billion in 2004 vs. $8.0 billion in 1991 • Diversification; Comply with Risk-Adequacy Regulations • Allows Origination even when Funding Constrained • Loan Selling Fundamentally Alters Lending

Main Issues • Loan Sales Separate Origination from Funding • Agency Problems • Moral Hazard (Pennacchi 1988; Gorton & Pennacchi 1995) • Adverse Selection • How do banks overcome these problems? • Loan Contracting • Access to Loans and Lending Relationships • Harm? • Reduce interaction that is critical to benefits (Diamond 1991) • Help? • Increased Capital From Non-Banks • Risk-Management Flexibility in Future Loan Origination

Outline • Data, Sample Selection, and Descriptive Statistics • Loan Sales and Loan Contracting • Secondary Market Sales and Covenants • Agency Problems or Signaling? • Loan Sales, Access to Loans, and Lending Relationships • Current Loans • Lending Relationships and Future Loans • Summary

Data and Sample Selection • Sample Period: 1999 - 2004 • Data from four sources with some data matched by hand • Loans & Lending Relationships (LPC DealScan) • Identify Traded Loans (LSTA Mark-to-Market Pricing) • Borrower Financial Characteristics (Compustat) • Equity Market Data (CRSP) • Sample Sizes (link)

Sold Loans and Information Asymmetry • Sold Borrowers are larger and rated (link) • Information Transparency • Sold Loans are Term Loans instead of Credit Lines • Monitoring • Lead Lender on Sold Loan has Higher Market Share • Reputation

Outline • Data, Sample Selection, and Descriptive Statistics • Loan Sales and Loan Contracting • Secondary Market Sales and Covenants • Agency Problems or Signaling? • Loan Sales, Access to Loans, and Lending Relationships • Current Loans • Lending Relationships and Future Loans • Summary

Screening Loan Seller Upfront Fees Borrower Interest Payments Loan Buyer Monitoring, Funding Secondary Market Sales and Covenants • Selling Loans Can Induce Agency Problems • Financial Covenants Reduce Reliance on Seller’s Information • Monitoring Mechanism • Buyer Exercises Control When Firm Performs Poorly

Secondary Market Sales and Covenants • Univariate Relationship Between Covenants and Loan Sales • Multivariate Logit Model (Table 4) (link) • Dependent Variable: Indicator for Loan is Sold • Key Independent Variables • # of Financial Covenants (+) • Net Worth Slack (-) • Control Variables • Lender Market Share; Borrower and Loan Variables

Secondary Market Sales and Covenants • Changes in Predicted Probabilities (link) • One Std. Dev Change Around the Mean (t-stats in parentheses) • Key Results: • More Covenants Increases Probability of Loan Sale • Tighter Covenants Increases Probability of Loan Sale

Are Loans Structured to Sell to Others? • Sold Loans are Nearly Always Syndicated (Primary Market) • Loans are Sold Close to the Loan Origination Date (link)

Are Loans Structured to Sell to Others? • Banks are not dumping poorly performing loans • Distribution of Initial Sale Prices • Performance of Sold Borrowers: Origination to Sale

Agency or Signaling? • Syndication: Primary Market Sales • Additional Mechanisms for Mitigating Agency Problems • Hold Larger Piece of Loan (e.g. Dennis & Mullineaux 2000) • Syndicate Structure and Composition (Lee & Mullineaux 2004; Sufi 2005) • Expect Smaller Agency Problems • Empirical Prediction • # of Covenants / Tighter Covenants have LESS influence on probability of loan syndication (compared to loan sale) • Empirical Model: Probability of Syndication (Table 5)link) • (

Primary Market Sales and Covenants • Changes in Predicted Probabilities (link) • One Std. Dev Change Around the Mean (t-stats in parentheses) • Compared to Secondary Market Sales: • More Covenants – Similar Effect • Tighter Covenants – Weaker Effect Evidence is consistent with agency view

Agency or Signaling? • Lower Reputation Lender Increased Agency Problems • Gorton & Haubrich (1987); Pichler & Wilhelm (2001) • Empirical Prediction • Low Reputation Lender # of Covenants / Tighter Covenants have LARGER influence on probability of loan selling • Modify Loan Sales Model (Table 6)(link) • Interact Reputation Indicators with Covenant Variables

Lender Reputation • Changes in Predicted Probabilities of Selling Loans (link) • One Std. Dev Change Around the Mean (t-stats in parentheses) • Key Result: • Tighter Covenants Increases Probability of Loan Sale when lenders have LOW REPUTATION Evidence is consistent with agency view

Agency or Signaling? • Does Restrictive Covenant Package Signal Borrower Quality? • Empirical Prediction • High Risk Covenants have LARGER influence on probability of loan selling • Modify Loan Sales Model (Table 7) (link) • Interact Distance-to-Default Indicators with Covenant Variables • KEY RESULTS: Largest Effect on Loan Sale Probability • # of Financial Covenants: LOW RISK BORROWERS • Net Worth Slack: MID RISK BORROWERS Evidence is NOT consistent with signaling view

Outline • Data, Sample Selection, and Descriptive Statistics • Loan Sales and Loan Contracting • Secondary Market Sales and Covenants • Agency Problems or Signaling? • Loan Sales, Access to Loans, and Lending Relationships • Current Loans • Lending Relationships and Future Loans • Summary

Loan Sales and Access to Loans • Restrictive Covenants / Loan Sales Impose Costs on Borrowers • Managerial Flexibility • Additional Lenders Renegotiation Costs • Why do Borrowers Agree to Restrictive Covenants / Loan Sales? • EXPLORE: Access to Private Debt Capital • Loan Buyers are Usually NonBanks Additional Capital

Current Loans • Key Results • Sold Borrowers are Growing and Debt-dependent • Sold Year: Increase in Private Debt Issuance

Screening Loan Seller Upfront Fees Borrower Interest Payments Loan Buyer Monitoring, Funding Loan Sales and Lending Relationships • Loan Sales Separate Origination from Monitoring / Funding • Harm Access to Future Credit / Relationships? • Reduced Ongoing Interaction(Diamond 1991; Boot & Thakor 1994) • Help Access to Future Credit / Relationships? • New Source of Capital • Reduced Exposure to Individual Borrowers Flexibility

Loan Sales and Lending Relationships • Univariate Results (Table 9) • Sold Borrowers are • More Likely to Receive Future Loans • More Likely to Continue Lending Relationships

Loan Sales and Lending Relationships • Explore: Risk Management Lending Flexibility • Do Loan Sales Increase Relationship Durability for High Risk Firms? High Reputation Lenders? • Univariate Results (Table 9): • Conditional on Receiving Another Loan, % that Keep Same Lead Bank

Don’t BorrowAgain Borrow Again Keep Lender Don’t Keep Lender Loan Sales and Lending Relationships • Nested Logit Model (Table 10) (link) • Independent Variables: “Borrow Again” • Borrower Characteristics; Year Fixed Effects • Independent Variables: “Borrow Again” and “Keep Lender” • Loan is Sold; Lender Market Share; Prior Lending Relationship

Outline • Data, Sample Selection, and Descriptive Statistics • Loan Sales and Loan Contracting • Secondary Market Sales and Covenants • Agency Problems or Signaling? • Loan Sales, Access to Loans, and Lending Relationships • Current Loans • Lending Relationships and Future Loans • Summary

Summary • Loan Selling Separates Origination and Funding • Agency Problems Loan Contracting • Access to Loans and Lending Relationships • Sold Loans Have Additional, Tighter Covenants • Consistent With Covenants Used When Agency Problems Are Larger • Signaling Not Supported • Sold Borrowers: Debt-Dependent, Receive Additional Private Debt • Benefit to Offset Costs of Restrictive Covenants / Loan Sales • Sold Borrowers get Future Loans, Keep Lending Relationships • Additional Capital and Flexibility for Lenders

Table 2: Univariate Analysis- Sold Loans vs. Not Sold Loans)

Table 2 (continued):Univariate Analysis - Sold Loans vs. Not Sold Loans (link)

Table 3: Sold Loans – Timing, Pricing, and Performance) (link)

Table 6: Probability of Selling Loans - Lender Reputation (link)

Table 7: Probability of Selling Loans – Borrower Risk (link)

Table 10 (continued): Nested Logit Models – Borrowing Again (link)