Download

1 / 23

230 likes | 324 Views

3. Business Cycle Theories (Survey). History : pre-Keynesian vs. modern theories Principal : real vs. monetary theories Stability : endogenous instability vs. exogenous shocks („ rocking chair “) Price flexibility : new Keynesian vs. new classical Macroeconomics.

E N D

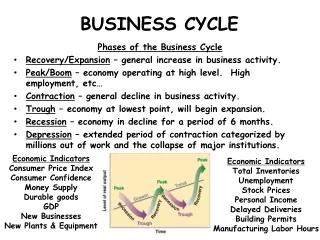

3. Business Cycle Theories (Survey) • History: pre-Keynesian vs. modern theories • Principal: real vs. monetarytheories • Stability: endogenousinstability vs. exogenousshocks („rockingchair“) • Price flexibility: newKeynesian vs. newclassicalMacroeconomics KuB 4 1 U van Suntum, Vorlesung KuB 1

KuB 3.1 2 KuB 4 2 U van Suntum, Vorlesung KuB 2

Interdependency of Macroeconomics M * V : P = monetary/monetaristic theories C + S = Y = C + I + E + EX - IM = Lnet + Gnet + T underconsumption theories Keynesian theories distribution theories KuB 3.1 3 U van Suntum, Vorlesung KuB 3 KuB 4 3

Basic idea of monetary theories HP = Mv = MB * m * v (quantityequation) • v dependent on i anddP/dt)/P => instability • m dependent on behaviorofbanksandhouseholds => instability KuB 3.1 4 U van Suntum, Vorlesung KuB 4 KuB 4 4

Central bankbalance (simplified) Assets Liabilities • currency in circulation • reserves • credit claims • bonds • foreign currency • other monetary base MB monetary base MB KuB 3.1 5 U van Suntum, Vorlesung KuB 5 KuB 4 5

Velocity of circulation v in Euro-Zone (1980 – 2000) ln [GDPnom/M3] source: ECB KuB 3.1 6 U van Suntum, Vorlesung KuB 6 KuB 4 6

Pure monetary theory by Ralph Hawtrey (1928) (I) • inventories are sensible to interest rate • Inventoryboughtat 1000.- • leveraged 900.- • equity: 100.- • inventorysoldat 1100.- • => Profit beforeinterest 100.- Rate of return (i = 11%): 1% Rate of return ( i = 10%): 10% KuB 3.1 7 U van Suntum, Vorlesung KuB 7 KuB 4 7

Pure monetary theory by Ralph Hawtrey (1928) (II) • inventories are also sensible to inflation Interest rates decline Interest rates rise inventory and commodity demand increase Inflation Inflation rising velocity of money circulation (Hawtrey effect) KuB 3.1 8 U van Suntum, Vorlesung KuB 8 KuB 4 8

Criticism on Hawtrey`s theory • Inventory less important today • Explanation of cycle is one-sided • Stimulus of initial interest rate decline unclear • However: leverage effect was relevant in recent financial crisis KuB 3.1 9 U van Suntum, Vorlesung KuB 9 KuB 4 9

Monetary over-investment theory (Knut Wicksell 1922, F.A. von Hayek 1934 ) upswing downswing S + d(M/P) S S + d(M/P) S imon inat imon I I Interest rate spread causal for disparity between investment and consumption goods KuB 3.1 10 U van Suntum, Vorlesung KuB 10 KuB 4 10

Criticism on Wicksell`s theory • Stimulus of initial interest rate spread unclear • Neglect of real effects (e.g. accelerator) • However: interest rate spread was also relevant in recent crisis KuB 3.1 11 U van Suntum, Vorlesung KuB 11 KuB 4 11

Theories of under-consumption (Lauderdale, Malthus, Lederer) • technical progress and capital accumulation • pressure on wages and rising unemployment • sales crisis and depression • Critisicm: • real wage increasebytechnicalisprogressneglected • turningpointsare not sufficientlyexplained • onesidedtheory, no formal exposition • exportdemandneglected KuB 3.1 12 U van Suntum, Vorlesung KuB 12 KuB 4 12

Non-monetary theory of excess investment (Aftalion u.a.) • Acceleratoreffect: • K/GDP = 300/100 • d = 10% • => D = 30 • supposedemandrisesat 10% in t1 • => I1 = 60 + 100% • I2 = 33 -45% • => extreme instability Aggregate Demand Investment • Criticism: • cause of initial rise in aggregate demand? • no formal exposition • one sided KuB 3.1 13 U van Suntum, Vorlesung KuB 13 KuB 4 13

Accelerator effect in East German Housing Market After unification today previous Demand (110) adds (11) Demand (110) adds (1,1) Housing stock ./. outs (108,9) Demand (100) adds (1) Housing stock ./. outs (99) Housing stock ./. outs (99) • increase in aggregate demand by 10% => rise in investment by 1100% ! • after completed construction of new houses drop in investment KuB 3.1 14 U van Suntum, Vorlesung KuB 14 KuB 4 14

Orders in East-German ConstructionIndustry KuB 3.1 15 U van Suntum, Vorlesung KuB 15 KuB 4 15

Dynamics of the business cycle GDP Investment GDP Investment KuB 3.1 16 U van Suntum, Vorlesung KuB 16 KuB 4 16

Is there an equilibrium of aggregate demand and investment? (Harrod-Domar 1939): Supply Demand KuB 3.1 17 U van Suntum, Vorlesung KuB 17

lnY Y* = 1/(1-c)Iaut Dynamics in Harrod/Domar-model: lnI t U van Suntum, Vorlesung KuB 18

Numerical example I: s = 0,2 x = 0,5 => g* = 0,2 * 0,5 = 0,1 a) equlibrium: gI = g* = 0,1 lnY lnI t I = sY = 0,2*100 = 20 Steady-state: all variables grow at the same rate U van Suntum, Vorlesung KuB 19

Numerical example II: s = 0,2 x = 0,5 => g* = 0,2 * 0,5 = 0,1 b) disequilibrium: gI = 0,2 > g* lnY t Excess investiment leads to under-utililization of capacities (Domars-Paradoxon) U van Suntum, Vorlesung KuB 20

Numerical example III: s = 0,2 x = 0,5 => g* = 0,2 * 0,5 = 0,1 c) disequilibrium: gI = 0,05 < g* lnY t Lack of investmentleads to excess capacity! U van Suntum, Vorlesung KuB 21

Criticism of Harrod/Domar • model does not reflect reality • s, x bzw. v need not be constant • no cycles • model is far too simple (no consumption, no public sector, no money, no labor market…) U van Suntum, Vorlesung KuB 22

Learning goals/Questions • How do we classify business cycle theories? • Which pre-Keynesian theories do we know? • To what extent are they still relevant today? • Explain why we cannot forecast GDP for more than two years at best! • Explain the Harrod-Domar condition for a balanced growth! KuB 3.1 23 U van Suntum, Vorlesung KuB 23 KuB 4 23