Download

1 / 28

280 likes | 288 Views

Learn about the basics, coverages, perils, exclusions, and conditions of homeowners insurance policies in the US. Explore different forms like HO-2, HO-3, HO-4, HO-5, HO-6, and HO-8 and understand the analysis of an HO-3 policy.

E N D

Agenda • Homeowners Insurance Basics • Analysis of Homeowners 3 Policy • Section I Coverages • Section I Perils Insured Against • Section I Exclusions • Section I Conditions • Section I & II Conditions

Homeowners Insurance Basics • Homeowners insurance forms, drafted by the Insurance Services Office (ISO) are widely used in the US • They are designed for the owner-occupants of family dwellings • A policy can be used to cover the dwelling, other structures, personal property, additional living expenses, personal liability claims, and medical payments to others • Six forms are available

Current Homeowners Policies • HO-2 (broad form): covers the dwelling, other structures, and personal property on a named perils basis • HO-3 (special form): covers the dwelling and other structures on a risk-of-direct-physical loss basis. • All direct physical losses are covered except those losses specifically excluded. • Personal property is covered on a named perils basis

Current Homeowners Policies • HO-4 (contents broad form): covers a tenant’s personal property on a named perils basis • HO-5 (comprehensive form): provides open perils coverage (“all-risks coverage”) on the dwelling, other structures and personal property. • All direct physical losses are covered except those losses specifically excluded

Current Homeowners Policies • HO-6 (unit owners form): covers personal property on a named perils basis. • A minimum of $5,000 of insurance is also provided on the condominium unit that covers improvements and additions • HO-8 (modified coverage form): designed for older homes. • Dwelling and other structures are based on the amount required to repair or replace using common construction materials and methods

Exhibit 20.1 Comparison of ISO Homeowners Coverages (continued)

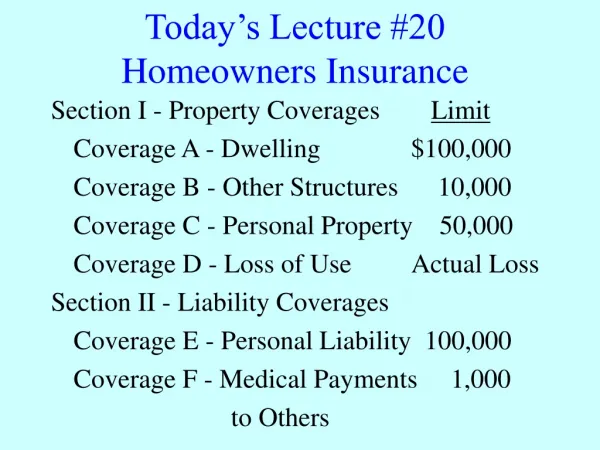

Analysis of the HO-3 Policy • Section I: Property Coverages • Coverage A: Dwelling • Coverage B: Other Structures • Coverage C: Personal Property • Coverage D: Loss of Use • Additional Coverages

Analysis of the HO-3 Policy • The following persons are considered “insureds” under the policy: • Named insured and spouse • Resident relatives • Other persons under age 21 • Full-time student away from home • Section II coverage also includes: • Any person legally responsible for covered animals or watercraft • With respect to a motor vehicle covered by the policy (e.g., a riding mower), persons employed by the named insured

Section I Coverages • Coverage A covers the dwelling on the residence premises and any structure attached to the dwelling • Materials intended for construction are included • The coverage specifically excludes land • Coverage B insures other structures on the residence premises • Includes a detached garage, tool shed, etc • Structures that are rented out or used for a business are excluded • The amount of coverage is based on the amount of insurance in Coverage A

Section I Coverages • Coverage C insures personal property owned or used by an insured • Personal property is covered anywhere in the world, both on and off the premises • The amount of coverage is 50% of Coverage A, but can be increased if desired • Coverage for personal property at another residence, such as a vacation home, is limited to 10% of Coverage C or $1000, whichever is greater • Certain types of personal property have maximum dollar limits on the amount paid for any loss

Section I Coverages • An insured can use a schedule to insure certain personal property for a specific amount • Coverage C also excludes certain types of property, for example: • Animals, birds, and fish • Motor vehicles • Aircraft and parts • Hovercraft and parts • Property of roomers, boarders, and other tenants • Property in a regularly rented apartment

Section I Coverages • Coverage D provides protection when the residence premises cannot be used because of a covered loss • Coverage is 30% of Coverage A • Additional living expense is the increase in living expenses actually incurred by the insured to maintain the family’s standard of living • The policy pays the fair rental value for that part of the residence that is rented to others, but is not fit to live in • Coverage applies if the home is not damaged, but a civil authority prohibits the insured from using the premises

Section I Coverages: Additional Coverages • Additional coverages in Section I include: • Removal of debris following an insured peril • Reasonable repairs to protect the property from further damage • Trees, shrubs, and plants, for a limited set of perils • Fire department service charge • Removal of property that is endangered by an insured peril • Unauthorized use of credit card, electronic funds transfer card or access device; forgery and counterfeit money

Section I Coverages: Additional Coverages • Additional Coverages, continued • Loss assessment charged against the named insured by a corporation or association of property owners because of the direct loss of property collectively owned by all members. • Collapse of a building, for certain perils • Breakage of glass or safety glazing material • Landlord’s furnishings • Increased costs of construction or repair because of a law • Grave markers

Section I Perils Insured Against • The dwelling and other structures are insured for all direct physical losses unless specifically excluded • Personal property is insured for a direct physical loss if it is caused by one of the perils listed in the policy • Named perils include fire, windstorm or hail, explosion, riot or civil commotion, aircraft, vehicles, smoke, vandalism, theft, etc. • The peril must be the proximate cause of the loss

Section I Exclusions • The policy excludes: • Concurrent causation losses • Any loss due to an ordinance or law, except as described in the Additional Coverages • Losses due to earth movement • Certain water losses • Losses due to neglect, power failure, or faulty design • Losses which are intentional • Losses due to war, government action, failure to act, or nuclear hazard • Losses due to certain weather conditions

Section I Conditions • The insurer’s liability for a loss is limited to the insured’s insurable interest at the time of loss • A deductible of $250 applies to any loss covered by Section 1 coverages • Premiums can be reduced by increasing the deductible • In states that are vulnerable to natural catastrophes, insurers can use percentage deductibles

Section I Conditions • The insured must perform certain duties after a loss occurs: • Give prompt notice to insurer • Protect the property from further damage • Prepare an inventory of damaged personal property • Exhibit damaged personal property • File a proof of loss with 60 days after the insurer’s request

Section I Conditions • Losses to personal property are paid on the basis of actual cash value • If the insured purchases a replacement cost endorsement, there is no deduction for depreciation • After giving notice to the insured, the insurer has the right to repair or replace any part of damaged property with like property

Section I Conditions • Losses to the dwelling and other structures are paid on the basis of replacement cost with no deduction for depreciation • If the dwelling is insured for at least 80% of replacement cost at the time of loss, partial losses are paid in full • Replacement cost is the amount necessary to repair or replace the dwelling with material of like kind and quality at current prices

If the dwelling is insured for less than 80% of the replacement cost, the insured receives the larger of: the actual cash value of that part of the building damaged, or Section I Conditions

Section I Conditions • Some insurers offer an extended replacement cost endorsement, which pays 20% or more above the policy limits • Under a guaranteed replacement cost policy, the insurer agrees to replace the home exactly as it was before the loss even if the replacement cost exceeds the amount of insurance stated in the policy • In the event of a loss to a pair or set, the insurer can elect either repair or replace any part of the pair or set or to pay the difference between the actual cash value of the property before and after the loss

Section I Conditions • The appraisal clause is used when the insured and insurer agree that the loss is covered, but the amount of loss is in dispute • If other insurance covers a Section I loss, the insurer will only pay the proportion of the loss that is limit of liability bears to the total amount of insurance covering the loss • No legal action can be brought against the insurer unless all policy provisions have been met • Legal action must be started within two years

Section I Conditions • The insurer has the right to repair or replace any part of the damaged property with like property • The insurer is generally required to make a loss payment directly to the named insured • The mortgage clause is designed to protect the mortgagee’s insurable interest • Only losses that occur during the policy period are covered • Concealment or misrepresentation of any material facts, fraudulent conduct, and false statement relating to the insurance will void insurance coverage

Section I and II Conditions • Conditions that apply to both Section I and Section II include: • A liberalization clause to address issues with broadening coverage • A waiver or change of policy provisions • Terms and conditions for cancellation • Terms for nonrenewal of the policy • Assignment of the policy to another party • A subrogation clause to address recoveries from third parties • Extension of policy terms to a legal representative upon the death of the named insured or spouse