Download

1 / 12

120 likes | 137 Views

Explore the significance of collecting precise household liability details and net worth for financial analysis and crisis assessment. Dive into U.S. home mortgage debt, house prices, consumer credit trends, and financial obligations ratios to grasp the comprehensive picture of household finances.

E N D

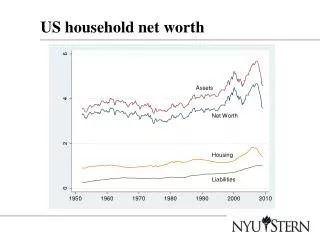

Importance of Measuring Household Liability Details and Net Worth Working Party on Financial Statistics OECD Paris, France October 13, 2008 Susan Hume McIntosh Sr. Economist and Special Project Coordinator Federal Reserve Board Washington, DC 20551 smcIntosh@frb.gov

Background on Data Collection • SNA approach is to collect short-term and long-term loans • OECD collects data on financial and nonfinancial assets of households • Liabilities split into mortgages, consumer credit, and other debt could be more useful • U.S. financial accounts present this split • Useful in analyzing current crisis

U.S. Home Mortgage Debt • Mortgages not written down until lender charges-off the loan • Charge-off treated as a flow • Better approach might be to treat charge-off as an ”other volume changes” • MBS are recorded at book value • Mortgages on investment properties and construction loans are recorded in the nonfinancial noncorporate sector

U.S. House Prices • Benchmarked to the 1999 American Housing Survey • Perpetual inventory method using OFHEO purchase-only price index • Investigating using Case-Shiller national price index or national index from Loan Performance

Consumer Credit • Continued borrowing in the form of consumer credit • Recently heavy reliance on revolving credit • Nonrevolving credit driven by auto sales remains very weak • Tells different story than mortgage debt growth

What Does All This Mean • Collection of financial statistics is important • More liability details could help • Data on securitization vehicles would also be useful • A full household balance sheet should be a goal