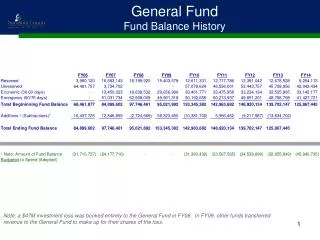

Download

1 / 21

220 likes | 548 Views

Inter-Fund Transfers Within SCO Fund 0948 Legal Basis vs. GAAP. October 24-25, 2007 Sherry Pickering and Lily Wang. Inter-Fund Activity Problem Statement - Issues with Inconsistency . Activity Recorded as: Expenditure Transfer (e.g. abatement) Transfers In/Out Revenue and Expense

E N D

Inter-Fund Transfers Within SCO Fund 0948 Legal Basis vs. GAAP October 24-25, 2007 Sherry Pickering and Lily Wang

Inter-Fund ActivityProblem Statement - Issues with Inconsistency • Activity Recorded as: • Expenditure Transfer (e.g. abatement) • Transfers In/Out • Revenue and Expense • The same transactions were recorded in a variety of ways between • Campus to Campus, or • Within Campus Ledger

Inter-Fund ActivityProblem Statement - Issues with Consistency (cont) • This is an issue because it • makes it difficult to training new staff • Increases the complexity and analysis in GAAP preparation. It can be a struggle to locate the entries that make up a set of transactions that need a GAAP reclassification

EO 1000 - Sends Us Back to School • Accounting Principles will be applied to ensure a consistent approach is used to record inter-fund activity. • Variations from this policy should be examined and reevaluated to apply the appropriate treatment

Back to Basics • Each Fund is a fiscal and accounting entity. • Transactions that must be recognized in more than one fund may be classified as: • Revenue or Expense if an external party was involved • Expense incurred on behalf of another • Periodic transfers made to shift resources - transfers

Revenue & Expense if an external party was involved… • Activity that Provides a Service to Another Fund • EO 753/1000 Cost Recovery • Federal Administrative Allowance • In both of these cases, departments funded by the operating fund provide various administrative services to the recipient fund. Had these same services been provided to a third party, the operating fund would record a revenue and the external party would record an expense.

EO 753/1000 Cost Recovery • Allowable direct costs incurred by the CSU Operating Fund are allocated and recovered. • Allowable and allocable indirect costs incurred by the CSU Operating Fund are identified in a cost recovery plan that and recovers them on a consistent methodology from “user” funds and programs. • Will be recorded in CSU Fund 485 • A unique FIRMS object code will be used to identify this revenue • A GAAP adjustment will be needed to eliminate double counting of revenues and expenses.

Cost Recovery Example • Plan allocates a service providing department cost to Housing program. • Service providing department would otherwise be funded from State General Fund/Student Fees • Housing assessed 20% of cost to service providing department

Expense Incurred on Behalf of Another • This occurs when there is a lack of adequate information at the time the transaction was recorded, an error or an incidental non-recurring service was performed • Pay vendor from a central fund and allocate to users. • Utility Bills • Energy Rebate – Offsets original cost • ProCard • Travel Vendors • Correction – Item was originally recorded to the wrong Fund/Dept.

ProCard Example • Contract stipulates ProCard vendor will receive payment net 10. • Not feasible to route the bill for signature, coding and back-up to meet that time constraint. • Payment is made from a central account & allocated to users based on campus policy. • Original Payment • Dr. 660003 - fund 485 • Cr. 108090 - fund 485 • Reclassifying Entry • Dr. 660003 - fund 531 • Cr. 108090 - fund 531 • Dr. 108090 - fund 485 • Cr. 660003 - fund 485

Non-Reciprocal Transfers • Transferring money to an ongoing program from another source • Debt Service Payments - Periodic movement of funds to DIRF • CERF Open University - Student pays CERF fee & program support funds moved to operating fund • Lottery Discretionary - Campus moves lottery funds to operating fund to purchase items to enhance a classroom experience • IRA-Athletics - Student pays IRA fee @ registration - funds moved to operating fund for intramural volleyball team organized by the athletics department

Non-Reciprocal Transfers & Fund 485 (cont) • A CSU Fund gives or receives value from/to another fund without directly giving or receiving equal value in exchange • May be recorded under the following criteria: • Costs cannot be readily and separately identified for services that have been provided • To supplement an existing program already operating in CSU Fund 485

CERF Open University Example • Meets the criteria to transfer into CSU fund 485 • To supplement an existing program already operating in 485

Reporting Inter-Fund Activity in GAAP GASB Statement 34, paragraph 112, offers guidance on how interfund activity should be classified and reported. • Reciprocal interfund activity • Nonreciprocal interfund activity • Interfund transfers • Interfund reimbursements

Reciprocal Interfund Activity • Service provided and used should be reported as revenue in the fund that provided the service and expense in the fund that used the service.

Example of Reciprocal Interfund Activity • Auxiliary Enterprise is assessed a charge for services provided by the operating fund. • A GAAP adjustment is required to eliminate the double counting of revenues and expenditures.

Nonreciprocal Interfund Activity • Interfund transfers - transfer of goods to another fund without expectation in return and repayment. • Interfund reimbursements - repayment from the fund responsible for the expense to the fund that initially paid for them.

Example of Nonreciprocal Interfund Activity - Transfers • To supplement an existing program already operating in fund 485. • No GAAP adjustment is needed. Transfers eliminate one-another.

Example of Nonreciprocal Interfund Activity - Reimbursements • ProCard vendor with a net 10 days. • Not feasible to route the bill for signature, coding and back-up to meet payment constraint. • Payment is made from a central account & allocated to users based on campus policy. • Original Payment • Dr. 660003 - fund 485 • Cr. 108090 - fund 485 • Reclassifying Entry • Dr. 660003 - fund 531 • Cr. 108090 - fund 531 • Dr. 108090 - fund 485 • Cr. 660003 - fund 485 • No GAAP adjustment is needed. Original expense is eliminated through the reimbursement.

What About Reimbursed Activities (RA)? • Most activity previously recorded in RA now fall under one of the interfund activity. • Reimbursed Activities has been re-defined: • May be utilized only in CSU Operating Fund 485 and in Revolving Fund 499. • Activity charged to RA shall be billed to a single outside entity or multiple funding sources. • Must equal zero by fiscal year-end. • Expenditures will not generate CSU compensation budget increases. • Must not be used for campus regular, on-going activities.