Download

1 / 21

210 likes | 332 Views

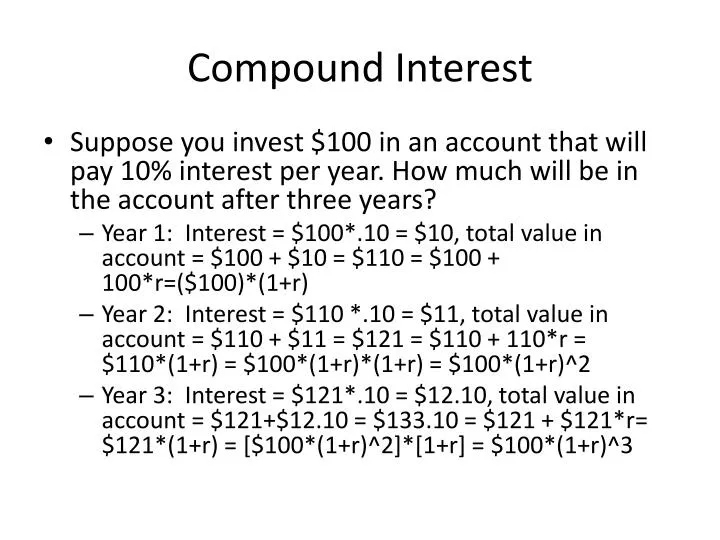

Compound Interest. Suppose you invest $100 in an account that will pay 10% interest per year. How much will be in the account after three years? Year 1: Interest = $100*.10 = $10, total value in account = $100 + $10 = $110 = $100 + 100*r=($100)*(1+r)

E N D

Compound Interest • Suppose you invest $100 in an account that will pay 10% interest per year. How much will be in the account after three years? • Year 1: Interest = $100*.10 = $10, total value in account = $100 + $10 = $110 = $100 + 100*r=($100)*(1+r) • Year 2: Interest = $110 *.10 = $11, total value in account = $110 + $11 = $121 = $110 + 110*r = $110*(1+r) = $100*(1+r)*(1+r) = $100*(1+r)^2 • Year 3: Interest = $121*.10 = $12.10, total value in account = $121+$12.10 = $133.10 = $121 + $121*r= $121*(1+r) = [$100*(1+r)^2]*[1+r] = $100*(1+r)^3

Compound Interest • Generalizing we get: • FV= PV(1 + r)t • Finding PVs is discounting, and it’s the reverse of compounding.

Compound Interest • Let’s suppose that you decide to save $50 per month starting at age 18 and ending at age 65. • How much money would you have in your savings account? • Total amount saved • 47 years * 12 months * $50 = $28,200 • Is that how much money you will have in the future?

Compound Interest • How much money would you have in your savings account if you earned • 4%? • 8%? • 12%? • http://www.lei.ncee.net/interactives/compound/

Compound Interest • The principle of compounding means that you earn interest on interest • Three things to consider • Invest early • Invest often • Have patience

Compound Interest • Finding PVs is discounting, and it’s the reverse of compounding.

Compound Interest • PV = value today of a future cash flow or series of cash flows= Equilibrium value of an investment • price at which investors are indifferent between buying and selling a security • Opportunity cost rate = the rate of return on the best available alternative investment of equal risk

What’s the PV of $100 due in 3 years if r = 10%? Finding PVs is discounting, and it’s the reverse of compounding. 0 1 2 3 10% 100 PV = ?

Present value 3 1 ö æ ÷ PV = $100 = ç ø è 1.10 ( ) = $100 0.7513 = $75.13.

Amortization • Construct an amortization schedule for a $1,000, 10% annual rate loan with 3 equal payments of $402.11.

Step 1: Find interest charge for Year 1. INTt = Beg balt (r) INT1 = $1,000(0.10) = $100. Step 2: Find repayment of principal in Year 1. Repmt = PMT - INT = $402.11 - $100 = $302.11.

Step 3: Find ending balance after Year 1. End bal = Beg bal - Repmt = $1,000 - $302.11 = $697.89. Repeat these steps for Years 2 and 3 to complete the amortization table.

BEG PRIN END YR BAL PMT INT PMT BAL 1 $1,000 $402 $100 $302 $698 2 698 402 70 332 366 3 366 402 37 366 0 TOT 1,206.34 206.34 1,000 Interest declines. Tax implications.

Project Example Information • You are looking at a new project and you have estimated the following cash flows: • Year 0: CF = -165,000 • Year 1: CF = 63,120; • Year 2: CF = 70,800 • Year 3: CF = 91,080; • Your required return for assets of this risk is 12%.

Net Present Value • The difference between the market value of a project and its cost • How much value is created from undertaking an investment? • The first step is to estimate the expected future cash flows. • The second step is to estimate the required return for projects of this risk level. • The third step is to find the present value of the cash flows and subtract the initial investment.

NPV – Decision Rule • If the NPV is positive, accept the project • A positive NPV means that the project is expected to add value to the firm and will therefore increase the wealth of the owners. • Since our goal is to increase owner wealth, NPV is a direct measure of how well this project will meet our goal.

Computing NPV for the Project • Using the formulas: • NPV = 63,120/(1.12) + 70,800/(1.12)2 + 91,080/(1.12)3 – 165,000 = 12,627.42 • Do we accept or reject the project?

Internal Rate of Return • This is the most important alternative to NPV • It is often used in practice and is intuitively appealing • It is based entirely on the estimated cash flows and is independent of interest rates found elsewhere

IRR – Definition and Decision Rule • Definition: IRR is the return that makes the NPV = 0 • Decision Rule: Accept the project if the IRR is greater than the required return

Computing IRR For The Project • If you do not have a financial calculator, then this becomes a trial and error process • Calculator • Enter the cash flows as you did with NPV • Press IRR and then CPT • IRR = 16.13% > 12% required return • Do we accept or reject the project?

NPV Profile For The Project IRR = 16.13%