Download

1 / 32

350 likes | 377 Views

This chapter explores how banks maximize profits, with a focus on balance sheets, asset and liability management, credit and interest-rate risk, and off-balance sheet activities. Learn about liquidity, asset, liability, and capital adequacy management. Discover the impact of bank capital on profitability and how a capital crunch can cause a credit crunch.

E N D

Chapter 9 Banking and the Management of Financial Institutions

Preview • This chapter examines how banks attempt to maximize their profits. • Although the discussion that follows focuses primarily on commercial banks, many of the same principles apply to other financial intermediaries as well.

Learning Objectives • Summarize the features of a bank balance sheet. • Apply changes to a bank’s assets and liabilities on a T-account. • Identify ways in which banks can manage their assets and liabilities to maximize profit.

Learning Objectives • List the ways in which banks deal with credit risk. • Apply gap and duration analysis and identify interest-rate risk. • Examine off-balance sheet activities.

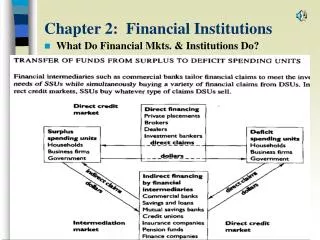

The Bank Balance Sheet • Liabilities: • Checkable deposits • Nontransaction deposits • Borrowings • Bank capital

The Bank Balance Sheet • Assets: • Reserves • Cash items in process of collection • Deposits at other banks • Securities • Loans • Other assets

Table 1 Balance Sheet of All Commercial Banks (items as a percentage of the total, June 2014)

Basic Banking • Cash Deposit: • Opening of a checking account leads to an increase in the bank’s reserves equal to the increase in checkable deposits.

Basic Banking Check Deposit: When a bank receives additional deposits, it gains an equal amount of reserves; when it loses deposits, it loses an equal amount of reserves.

Basic Banking • Making a profit: • Asset transformation: selling liabilities with one set of characteristics and using the proceeds to buy assets with a different set of characteristics • The bank borrows short and lends long and make profits from the process of asset transformation

General Principles of Bank Management • Liquidity Management • Asset Management • Liability Management • Capital Adequacy Management • Credit Risk • Interest-rate Risk

Liquidity Management and the Role of Reserves • Excess reserves: • Suppose a bank’s required reserves are 10%. • If a bank has ample excess reserves, a deposit outflow does not necessitate changes in other parts of its balance sheet.

Liquidity Management and the Role of Reserves • Shortfall: • Reserves are a legal requirement and the shortfall must be eliminated. • Excess reserves are insurance against the costs associated with deposit outflows.

Liquidity Management and the Role of Reserves • Borrowing: • Cost incurred is the interest rate paid on the borrowed funds

Liquidity Management and the Role of Reserves • Securities sale: • The cost of selling securities is the brokerage and other transaction costs.

Liquidity Management and the Role of Reserves • Federal Reserve: • Borrowing discount loans from the Fed also incurs interest payments based on the discount rate.

Liquidity Management and the Role of Reserves • Reduce loans: • Reduction of loans is the most costly way of acquiring reserves. • Calling in loans antagonizes customers. • Other banks may only agree to purchase loans at a substantial discount.

Asset Management Three goals: • Seek the highest possible returns on loans and securities. • Reduce risk. • Have adequate liquidity.

Asset Management Four Tools: • Find borrowers who will pay high interest rates and have low possibility of defaulting. • Purchase securities with high returns and low risk. • Lower risk by diversifying. • Balance need for liquidity against increased returns from less liquid assets.

Liability Management • Recent phenomenon due to rise of money center banks • Expansion of overnight loan markets and new financial instruments (such as negotiable CDs) • Checkable deposits have decreased in importance as source of bank funds.

Capital Adequacy Management • Bank capital serves as a cushion to the bad shocks and helps prevent bank failure. • The amount of capital affects return for the owners (equity holders) of the bank. • Regulatory requirement

Capital Adequacy Management How Bank Capital Helps Prevent Bank Failure:

How the Amount of Bank Capital Affects Returns to Equity Holders In order to know whether a bank is managed well, proper measures of bank profitability are needed.

Capital Adequacy Management • Trade-off between safety and returns to equity holders: • Benefits the owners of a bank by making their investment safe • Costly to owners of a bank because the higher the bank capital, the lower the return on equity • Choice depends on the state of the economy and levels of confidence

Application: How a Capital Crunch Caused a Credit Crunch During the Global Financial Crisis • Shortfalls of bank capital led to slower credit growth: • Huge losses for banks from their holdings of securities backed by residential mortgages. • Losses reduced bank capital • Banks could not raise much capital on a weak economy, and had to tighten their lending standards and reduce lending.

Managing Credit Risk • Screening and Monitoring: • Screening • Specialization in lending (e.g. to local firms or to firms in a particular industry) • Monitoring and enforcement of restrictive covenants • Long-term customer relationships • Loan commitments • Collateral and compensating balances • Credit rationing

Managing Interest-Rate Risk • If a bank has more rate-sensitive liabilities than assets, a rise in interest rates will reduce bank profits and a decline in interest rates will raise bank profits.

Gap and Duration Analysis • Basic gap analysis: (rate sensitive assets - rate sensitive liabilities) x interest rates = in bank profit • Maturity bucked approach: • Measures the gap for several maturity subintervals • Standardized gap analysis: • Accounts for different degrees of rate sensitivity

Off-Balance-Sheet Activities • Loan sales (secondary loan participation) • Generation of fee income. Examples: • Servicing mortgage-backed securities • Creating SIVs (structured investment vehicles) which can potentially expose banks to risk, as it happened in the global financial crisis

Off-Balance-Sheet Activities • Trading activities and risk management techniques: • Financial futures, options for debt instruments, interest rate swaps, transactions in the foreign exchange market and speculation • Principal-agent problem arises

Off-Balance-Sheet Activities • Internal controls to reduce the principal-agent problem: • Separation of trading activities and bookkeeping • Limits on exposure • Value-at-risk • Stress testing