Download

1 / 15

180 likes | 531 Views

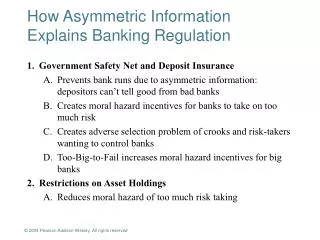

Banking Regulation. Chap. 11. Review: Asymmetric Information. Before transaction … ADVERSE SELECTION After transaction …. MORAL HAZARD. Types of Banking Regulation. Restrictions on bank’s assets. Government safety net (FDIC). Capital requirements.

E N D

Banking Regulation Chap. 11 Maclachlan, Money & Banking Spring 2006

Review: Asymmetric Information Before transaction … ADVERSE SELECTION After transaction …. MORAL HAZARD Maclachlan, Money & Banking Spring 2006

Types of Banking Regulation • Restrictions on bank’s assets. • Government safety net (FDIC). • Capital requirements. • Bank supervision. • Assessment of risk management. 6. Disclosure requirements. 7. Consumer protection. 8. Restrictions on competition. Maclachlan, Money & Banking Spring 2006

1. Government Safety Net Emergency legislation March 1933. Bank failures 1930-33: 2000/year 1934-1981: 15/year When bank fails, two things can happen … PAY OFF or PURCHASE & ASSUMPTION “Too Big to Fail” (relate to consolidation) Maclachlan, Money & Banking Spring 2006

FDIC Improvement Act (1991) • Limited brokered deposits. • Renounced too-big-to-fail. • Supervision of foreign banks in U.S. • Risk based premiums Maclachlan, Money & Banking Spring 2006

2. Restrictions on Assets No securities related activities except … Treasurys, municipals, government agency securities Foreign exchange Derivatives Commercial paper underwriting Maclachlan, Money & Banking Spring 2006

3. Capital Requirements Leverage ratio = capital/assets > 5% Basel Accord: capital = 8% of risk adjusted assets (assets are weighted by risk factor) Regulatory arbitrage Maclachlan, Money & Banking Spring 2006

4. Bank Supervision Three layers of supervision for nationally chartered bank: 1863 Comptroller of Currency 1913 Federal Reserve 1933 FDIC Maclachlan, Money & Banking Spring 2006

CAMELS Capital adequacy Asset quality Management Earnings Liquidity Sensitivity to market risk Maclachlan, Money & Banking Spring 2006

5. Assessment of Risk Management Looking at quality of assets is not enough. Diversification and hedging reduce risk. Examiners look at oversight, policies, risk measurement and monitoring, internal controls. Maclachlan, Money & Banking Spring 2006

6. Disclosure Requirements Allows large depositors and investors to accurately assess risk. Maclachlan, Money & Banking Spring 2006

7. Consumer Protection Consumer Protection Act of 1969 “Truth in Lending”: Disclosure of APR and total finance charges. Equal Credit Opportunity Act 1974 Community Reinvestment Act 1977 (prevents redlining) Maclachlan, Money & Banking Spring 2006

8. Restrictions on Competition McFadden Act 1927-1994 Glass Steagall 1933-1999 Maclachlan, Money & Banking Spring 2006

Financial Institutions Reform, Recovery, and Enforcement Act (1989) • FSLIC closed down. • Resolution Trust Corporation to close down S&L’s and pay off depositors. • Total cost to taxpayer: $150 billion. Maclachlan, Money & Banking Spring 2006

Innovation & Regulation How is bank regulation related to the following innovations? Commercial paper Adjustable rate mortgages Securitization MMMF’s Sweep accounts Maclachlan, Money & Banking Spring 2006