Download

1 / 50

520 likes | 901 Views

Chapter 9 Pension Funds. Background Types Assets Regulation Social Security. Background. defined by function -- payment of retirement benefits tax treatment -- tax exempt earnings & contributions or benefits. Pension plan sponsor. private or public employers unions individuals.

E N D

Chapter 9 Pension Funds • Background • Types • Assets • Regulation • Social Security

Background • defined by • function -- payment of retirement benefits • tax treatment -- tax exempt earnings & contributions or benefits

Pension plan sponsor • private or public employers • unions • individuals

Pension plan administrator • employer • insurance company • investment company • commercial banks

Federal law • does NOT require pension plans • but regulates existing pension plans

I. Types • Defined benefit plans • Defined contribution plans • Hybrid plans

Defined benefit plans • employer promised employee monthly payments during retirement -- life contingent -- choice of survivor benefits

How is payment determined? • formula • salary -- average last several years -- average of best years • years of service with sponsor

Vesting • minimum years of service necessary to receive benefits • complex federal rules about vesting • 5-7 years max for full vesting

Advantages • (for employee) • limited investment risk • payments promised reguardless of portfolio return • but sponsor bankruptcy could affect payment size

no risk of outliving assets • payments life contingent, NOT lump sum

Disadvantages • lack of portability from job to job • largest benefits accrue after 20 years • DB plans encourage loyalty

lack of control • how pension funds are invested • is sponsor investing enough? -- is pension fully funded?

example: • salary base • average of best 5 years • pay % of salary, based on years of service • 5 years, 25% • 20 years, 60% • 30 years, 85%

Defined Contribution Plans • employee/individual contributes funds • employer may match contributions • employee chooses among investment options • range of choice varies among sponsors

amount accumulated at retirement depends on investment performance • lump sum at retirement • decision about spending • possible purchase an annuity

types of DC plans • employer sponsored • 401(k), 403(b), 414(h), 457 • $12,000 contribution limit 2003 • individual • IRA, Roth IRA • $3000 contribution limit 2003

Advantages (employee) • portability • value accumulates steadily • balance rolled over to new plans • cash value build up • cash out (tax penalty) • borrow against • survivor benefits

Disadvantages • employee bears investment risk • retiree risks outliving assets

example • I contribute 3% of gross salary (pretax) • SUNY matches 9% • I choose investments through TIAA-CREF • growth, index, international, bonds, etc. • quarterly statements

Cash balance plan • hybrid plan • features of both DB, DC plans • fixed employer contribution • % of salary (5%) • guaranteed annual return on balance • Treasury rate

DB features • employer bears investment risk • must make up difference if actual return lower than promised return • but keeps potential surplus

DC features • each employee monitors own account • vested benefits portable

controversy • conversion from DB to CB • younger employees better off • older employees often worse off -- DB plans get most of value in last 5-10 years of service

example • IBM 1999 • announced conversion to CB • older employees stood to lose over 50% of expected benefits • after EEOC inquiry, lawsuits, IBM allowed older workers to choose their plan

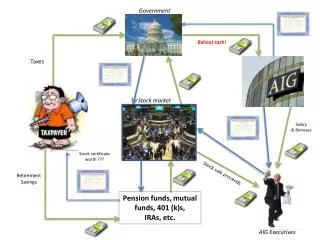

II. Assets • Defined benefit plans • 75% U.S. stocks, bonds • unions less likely to hold international assets

corporate defined contribution plans • hold over 25% of assets as own company stock -- Enron 60% -- Anheuser Bush, Coca Cola, McDonald’s over 74% • big lack of diversification -- but easier to match 401(k) contributions w/ stock than w/cash

401ks invested heavily in company stock have led to huge losses • Enron, Lucent, Xerox

III. Regulation • tax treatment • tax exempt contributions -- DB, 401k, IRA, CB • tax deferred earnings -- all • tax exempt withdrawals -- Roth IRA

early withdrawal of funds (DC, CB) • before age 59.5 • taxable AND extra 10% penalty -- exceptions for -- medical bills -- education -- disability -- home buyers

ERISA (1974) • set funding standards • DB plans must be fully funded not “pay-as-you-go” • sponsors must set aside funds for employees, not pay obligations out of current income

set vesting standards • 5-7 years max for full vesting • federal insurance for DB pensions • PBGC • vested benefits up to a limit • no COLA • trustee to over 2500 plans

guidelines for pension fund mgmt. • both DB, DC plans • plan must provide prudent, investing options • Enron lawsuit -- must show stock was not a prudent option

How long can employer keep 401k contributions before investing? • old rule: 90 days • since 1997: 15 days after end of month of payday

IV. Social Security • established 1935 • DB plan supported by payroll tax • 6.2% employee & employer • tax wages up to $87,000

benefits based on • age of retirement • # years worked • income • annual COLAs based on CPI

SS is pay-as-you-go • retirees today paid with current payroll taxes • right now payroll tax revenue > benefits this surplus is “invested” in Treasury IOUs

Problems w/ SS • U.S. population is aging • too many collecting benefits relative to how many paying taxes • 3.4 payer-to-receiver today • 2 payer-to-receiver in 2030

today revenue > benefits • by 2015 benefits > revenues • draw on Treasury IOUs • by 2040 assets exhausted • must supplement with other tax revenue

Solutions? • increase retirement age • already increased from 65 to 67 for those born after 1960 • increase payroll tax • regressive tax • already risen from 2% to 12.4%

investing surplus in assets other than Treasury IOUs • higher return BUT higher risk • government stock ownership is problematic -- corporate control -- price volatility

Private retirement accounts • allow % of payroll tax for workers to invest in choice of investments • how to deal with risk? • do workers have investment savvy? • disability/survivor benefits? • how to transition?