Download

1 / 13

130 likes | 316 Views

LECTURE 2: THE EVOLUTION OF CORPORATE LAW AND CORPORATE BANKRUPTCY. David Skeel 26 November 2008. Simple Overview of U.S. Bankruptcy. Douglas Baird, The Elements of Bankruptcy (4 th edition 2005). Roadmap for Today.

E N D

LECTURE 2: THE EVOLUTION OF CORPORATE LAW AND CORPORATE BANKRUPTCY David Skeel 26 November 2008

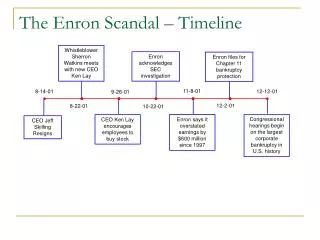

Simple Overview of U.S. Bankruptcy • Douglas Baird, The Elements of Bankruptcy (4th edition 2005)

Roadmap for Today • Simple theory of relationship between corporate law and corporate bankruptcy • Emphasis on US, but application is general

The Evolutionary Theory • Assumption: corporate law and corporate bankruptcy = connected • Key factors: 1) concentrated vs. diffuse stock and debt; 2) manager driven vs. manager displacing bankr

Concentrated vs. diffuse stock and debt • Concentrated stock goes with concentrated debt (and diffuse with diffuse) • Reason: Monitoring • Controlling shareholders could take advantage of diffuse debt • Thus, firms with controlling shareholders usually have bank lender • But bank lending is costly, so firms with diffuse shareholders issue diffuse debt (bonds)

The Link between Capital Structure and Bankruptcy • 1) Concentrated stock and debt go with manager-displacing bankruptcy • Why? • Manager-displacing bankruptcy enhances creditors’ leverage

The Link Between Capital Structure and Bankruptcy (cont’ed) • Diffuse stock and debt (and market-based governance) go with manager-driven bankruptcy • Why? • Failure doesn’t necessarily reflect non-viability of the business • Thus, need reorganization-oriented approach (and managers not removed)

Why Are Alternative Frameworks Unstable? • Concentrated debt/stock with manager-driven bankruptcy • Problem: manager-driven bankruptcy would undermine creditor monitoring

Why are Alternative Approaches Unstable? • Diffuse stock/debt with manager- displacing bankruptcy • Problems: • Managers would face Scylla and Charybdis of takeovers and displacement in bankruptcy • Response: 1) seek out blockholders; or 2) alter the bankruptcy framework (US in 1950s/60s; UK in 1980s/1990s)

Implications in Europe • Shift to shareholder capitalism would create pressure for manager driven bankruptcy • Notice the push back against the 13th Directive • Shopping for bankruptcy location could undermine the corporate framework (best solution is ex ante commitment: in US, place of incorp)

Conclusions • Corporate governance and bankruptcy go together • Reforms should take both into account