Download

1 / 9

90 likes | 268 Views

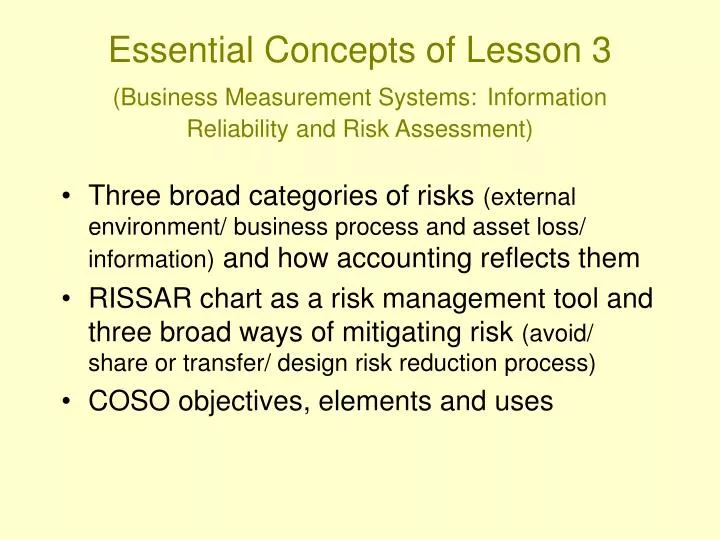

Essential Concepts of Lesson 3 (Business Measurement Systems: Information Reliability and Risk Assessment). Three broad categories of risks (external environment/ business process and asset loss/ information) and how accounting reflects them

E N D

Essential Concepts of Lesson 3(Business Measurement Systems:Information Reliability and Risk Assessment) • Three broad categories of risks (external environment/ business process and asset loss/ information) and how accounting reflects them • RISSAR chart as a risk management tool and three broad ways of mitigating risk (avoid/ share or transfer/ design risk reduction process) • COSO objectives, elements and uses

Assuring information display: financial audits Real world condition of firm Test of details IC criteria (COSO) Accounting and compliance system Expected “true” value Analytical procedures Accounting criteria (GAAP) Recorded financial statements Audited financials Auditor’s report

Internal Control is a process, effected by an entity’s board of directors, management and other personnel designed to provide reasonable assurance regarding the achievement of objectives in the following categories • effectiveness and efficiency of operations • reliability of financial information • compliance with laws and regulations (COSO 1994)

Internal control components • Control environment - overall context of control process • Risk assessment - identification, sourcing and sizing of threats • Control activities - policies and procedures to reduce likelihood that risk will exceed acceptable limits • Information and communication - systematic transfer of information within and outside the entity • Monitoring - analysis of functioning of other components of internal control

Excusez-Moi Flower ExpressInternal Control Overview-Delivery Express Plan/predict: Ap, Bp, sp, Xp Budgeting: Implement budget and record results: Yr= S recorded delivery expenses = a + bX + u + m = A + BX + d Operations: Assess: Volume differences: X vs. Xp Model changes: A, B, s, vs. predicted Possible misstatement: each d and Sd Audit: Details of transactions at random Internal auditing: Internal Information Risk

Budget: Ap + Bp Xp = Total Costp Estimate Ap + Bp Xact = Total Costact Estimate Recorded: Total recorded cost = S invoices recorded = a + b Xact + u + m Compare: Ap + Bp Xp with A + B Xact to evaluate prediction model, then calculate: Total recorded cost - (Aadj + Badj Xact ) = d = est. (u+m) for each outlet and sum E-MFE

Independence and consulting “And don't forget that many of PWC's clients chose the firm for its independence--something that may be compromised by a tie to HP. Although IBM and other consultants . . . often suggest hardware made by competitors, rival consulting firms are licking their chops. ``People will be asking . . . whether this changes the nature of the advice they're receiving,'' says Richard Boulton, managing partner for Arthur Andersen's business-consulting unit.” Business Week, Sept. 25, 2000, p. 52