Download

1 / 6

70 likes | 89 Views

Understand perpetual and periodic inventory systems, cost valuation methods, and cost flow considerations. Learn how to determine inventory and profit using practical examples.

E N D

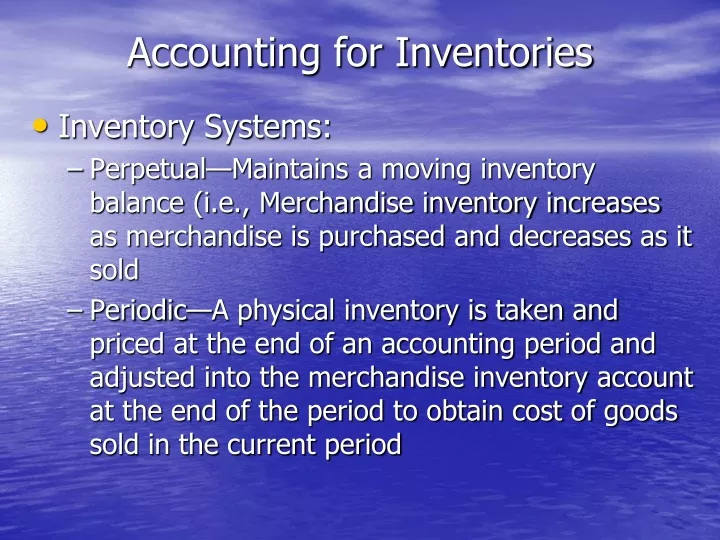

Accounting for Inventories • Inventory Systems: • Perpetual—Maintains a moving inventory balance (i.e., Merchandise inventory increases as merchandise is purchased and decreases as it sold • Periodic—A physical inventory is taken and priced at the end of an accounting period and adjusted into the merchandise inventory account at the end of the period to obtain cost of goods sold in the current period

Inventory Valuation Methods • Cost • Inventory is valued at what the business paid for it (includes cash discounts, freight-in, and returns allowed) • Lower of Cost or Market • Current replacement cost is compared with the purchase price of each item in inventory; then the lower of the amount on an aggregate basis is used for inventory valuation

Flow of Cost Considerations • Specific Identification—Cost of specific items purchased follow those items as they are sold • First-in; first-out (applies to cost of goods sold) • First purchase prices apply to first goods sold; Most recent purchase prices apply to what is left in ending inventory • Last-in; first-out (applies to cost of goods sold) • First purchase prices apply to ending inventory; Most recent purchase prices apply to first goods sold • Weighted average • Average cost of purchases is determined and the same price per unit is applied to both cost of goods sold and ending inventory

Example of Cost Flows • Specific Identification • 1st purchase item A @ $50; 2nd purchase item A @ $100 • 1st sale is item A is the second purchase; CGS would be $100 and ending inventory would be $50 • First-In, First-Out same example • Cost of goods sold would be $50 and ending inventory would be $100

Example of Cost Flows, Continued • Last-In, First-Out • Cost of goods sold would be $100 and ending inventory would be $50 • Weighted Average • ($50 + 100)/2 = $75 average cost • Cost of goods sold would be $75 (one item @ $75) • Ending inventory would be $75 (one item @ $75

Inventory And Profit Determination • An important equation in this pricing process is— • Beginning inventory + purchases = Total available for sale • Total available for sale = Cost of Goods Sold + Ending Inventory • So one can calculate the cost of goods sold first or the ending inventory first and subtract from total available for sale to get the other amount