Download

1 / 2

20 likes | 80 Views

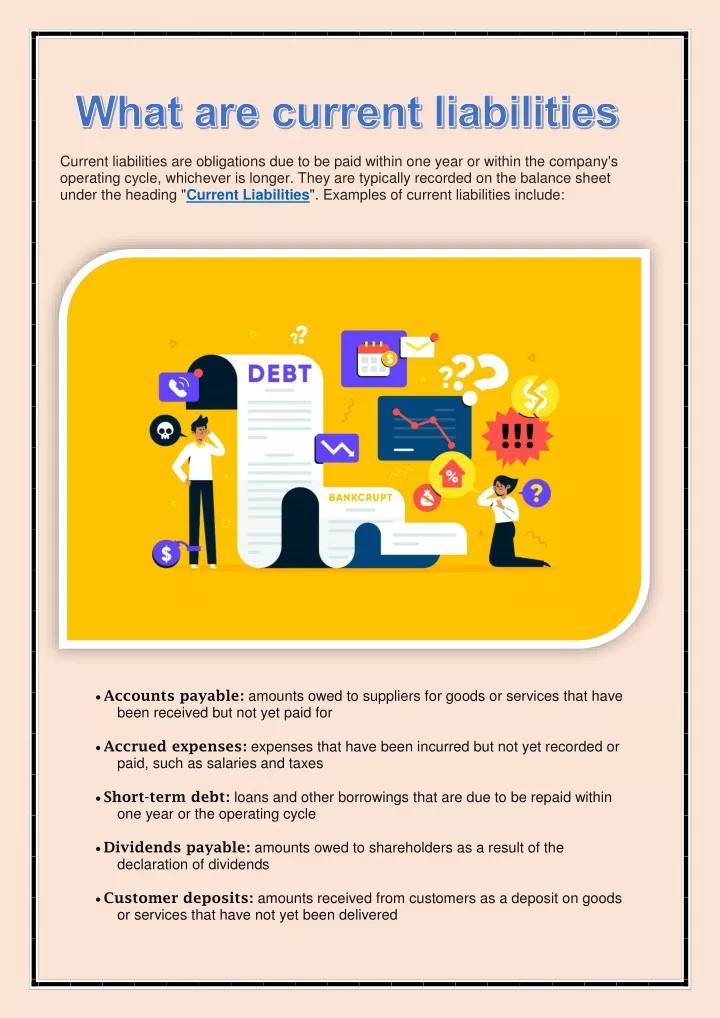

<br>Current liabilities are obligations due to be paid within one year or within the company's operating cycle, whichever is longer. They are typically recorded on the balance sheet under the heading "Current Liabilities". Examples of current liabilities include:<br>

E N D

Current liabilities are obligations due to be paid within one year or within the company's operating cycle, whichever is longer. They are typically recorded on the balance sheet under the heading "Current Liabilities". Examples of current liabilities include: Accounts payable: amounts owed to suppliers for goods or services that have been received but not yet paid for Accrued expenses: expenses that have been incurred but not yet recorded or paid, such as salaries and taxes Short-term debt: loans and other borrowings that are due to be repaid within one year or the operating cycle Dividends payable: amounts owed to shareholders as a result of the declaration of dividends Customer deposits: amounts received from customers as a deposit on goods or services that have not yet been delivered

How do companies determine the amount of their current liabilities? Companies determine the amount of their current liabilities by adding up all of their obligations due to be paid within one year or within the operating cycle, whichever is longer. This includes explicit obligations, such as accounts payable and short- term debt, and implicit obligations, such as warranties and guarantees. How do companies account for current liabilities in their financial statements? Current liabilities are typically recorded on the balance sheet at their present value, which is the amount the company expects to pay when the liability is settled. The present value is calculated by discounting the expected future payments using a discount rate that reflects the time value of money. How do companies classify their current liabilities as either current or non-current on the balance sheet? Current liabilities are classified as either current or non-current on the balance sheet based on their expected settlement date. Obligations to be settled within one year or the operating cycle, whichever is longer, are classified as current liabilities. Obligations to be settled after one year or the operating cycle are classified as non-current liabilities. How do changes in a company's current liabilities affect its financial statements? Changes in a company's current liabilities can affect its financial statements in several ways. For example, an increase in current liabilities may indicate that the company has incurred additional obligations or has experienced a slowdown in its cash collections. This may increase the company's working capital, which is the difference between its current assets and current liabilities. On the other hand, a decrease in current liabilities may indicate that the company has made progress in paying off its obligations or has experienced an improvement in its cash collections. This may lead to a decrease in the company's working capital. How do companies disclose their current liabilities in their footnotes? Companies must disclose information about their current liabilities in the footnotes to their financial statements. This may include details about the nature and terms of the liabilities, any collateral or security provided, and any significant contingencies or uncertainties related to the liabilities. The footnotes may also provide information about any off-balance sheet financing arrangements or guarantees that are not reflected on the balance sheet.