Download

1 / 35

350 likes | 398 Views

Oligopoly. Oligopoly. For a Market to be Described as Oligopolistic, it must satisfy the following conditions: Few Sellers Mutual Interdependence The Firm’s products may be identical or unique ( Homogeneous or Differentiated) The are Barriers to Entry (like monopoly)

E N D

Oligopoly • For a Market to be Described as Oligopolistic, it must satisfy the following conditions: • Few Sellers • Mutual Interdependence • The Firm’s products may be identical or unique (Homogeneous or Differentiated) • The are Barriers to Entry (like monopoly) • non-price competition

Monopolistic Competition Where Does Oligopoly “fit in?” Perfect Competition Monopoly Oligopoly

Oligopoly Model • Oligopoly is a market in which a small number of firms supply the entire market and where natural barriers to entry prevent other firms from entering • Examples: beer, breakfast cereals, automobiles, long-distance telephones, airplanes, database software,...

Concentration Ratios • One Way to Determine Whether a Market is Oligopolistic is to look at a Concentration Ratio • A Concentration Ratio Let’s Us Know if the Whole Industry’s Sales are Dominated by the Sales of a Few Firms.

Oligopolies and Collusion • Overt Collusion • OPEC Cartel • Covert Collusion • Electrical Equipment • Price Fixing • Tacit Collusion • Price Leadership

Models of Oligopoly No Standard Model due to... Diversity Interdependence 1 - Kinked Demand Curve 2 - Collusive Pricing 3 - Price Leadership

Kinked Demand Curve • Each Oligopolist believes that if it raises its price, other firms will keep their prices constant, so the quantity demanded will fall by a large amount(demand is elastic). • Each firm also believes that if it cuts its price, other firms will cut their prices too, so the quantity demanded will rise by a small amount(demand is inelastic).

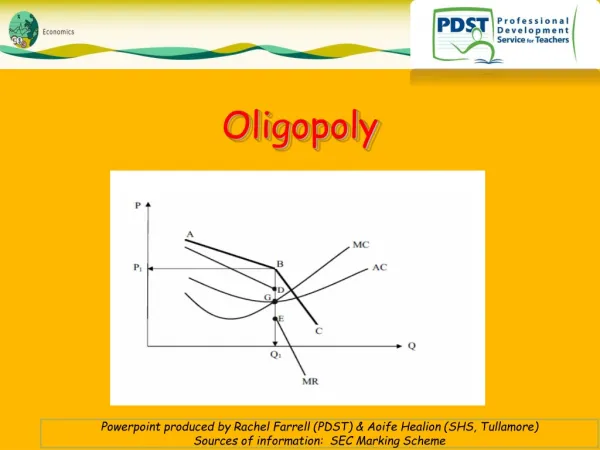

Kinked Demand Curve Effectively creating a kinked demand curve This is an attempt to explain the “sticky prices” in oligopoly industries. P P D2 D1 Q Quantity

The Kinked Demand Curve Theory • The current price is P • And at this price, the firm is selling the quantity Q P

The Kinked Demand Curve Theory • The marginal revenue curve from “b” down. • The marginal revenue curve for a price increase runs from “a” up.

The Kinked Demand Curve Theory • Between a and b, there is no marginal revenue curve • Cost can increase considerably without causing the firm to increase price. • So long as the MC curve passes through the break in the MR curve, the firms keeps its price and quantity constant.

The Kinked Demand Curve Theory • Summary: • The demand curve has a kink at the current price • The marginal revenue curve is discontinuous • Price is sticky and remains at the kink point unless a large enough change in marginal cost occurs • The elasticity of demand indicates a decrease in TR for any price change.

Cartels and Collusion Oligopoly is conducive to collusion If a few firms face identical or highly similar demand and costs... They will seek joint profit maximization...

Collusive Pricing Model • The Cartel Model: • The Oligopolists Get Together (Since There are So Few of Them) and Act As If They Were One Monopolist. • Collectively Produce the Monopolistic Quantity (establish quotas) - Thus Maximizing Profit as a group. • Example: OPEC

Cartel Model • Collusive agreement --a cartel--is an agreement between two (or more) producers to restrict output in order to raise prices and make bigger profits (act like a monopoly). • Strategies for a firm in a cartel • complywith the agreement • cheaton the agreement

Problems With Cartels • 10 sellers produce oils 150 barrels/day (Total 1,500 b/day) • If each firm is in perfect competitive market • Each firm will get normal profit • But if they decide to collude as one monopoly such as OPEC

Maximizing OPEC Profits Market Single producer $ $ MC MC AC 20 20 MR D= AR MR Q Q 1,500 150 Firm Oil (Barrels/Day) Oil (Barrels/Day)

Maximizing OPEC Profits Single producer Market If one seller cheats $ $ MC MC AC 30 30 a b 22 20 20 MR D= AR MR Q 1,000 Q Qcheater = 180 Qquota =100 1,500 1,800 150 Firm Oil (Barrels/Day) Oil (Barrels/Day)

Problems With Cartels • Generally, They Are Not Legal(Price Fixing) • They Are Difficult to Organize and Monitor • Can’t Force New Firms to Join • Usually there is Cheating

The Incentive to Cheat On A Cartel • If the Cartel Maintains the Monopoly Price, The Individual Member of the Cartel Can Act Like a Price Taker(They Can Sell the Quota amount at the Market Price) • As a Price Taker, They Maximize Profit Where MC = MR. • This Quantity is Greater Than the Cartel Wants the Individual Firm to Produce. • All Firms in the Cartel Do This and the Cartel Falls Apart

Obstacles to Collusion • Demand & Cost Differences • Number of Firms • Cheating • Recession • Potential Entry (or new)Entry • Legal Obstacles: Antitrust

Dominant Firm Price Leadership • One dominant firm (largest or lowest cost) and several other rival firms • Dominant firm determines price to maximize profit • Other firms take price and sell what they can at that price. • All firms watch output to prevent excess supply and the need to reduce price.

Dominant Firm Oligopoly A dominant firm oligopoly may exist if one firm: • Has a big cost advantage over the other firms. • Sells a large part of the industry output. • Sets the market price. • Other firms are price takers.

Dominant Firm Oligopoly Let’s use Big-G as an example. Big-G is the dominant gas station in a city.

S10 MC a b b a MR Dominant Firm Oligopoly Ten small firms and market demand Big-G’s price and output decision 1.50 1.50 Price (dollars per gallon) 1.00 1.00 D 0.50 0.50 XD 10 0 0 20 20 10 Quantity (thous. of gal./week) Quantity (thous. of gal./week)

G A M E T H O E R Y

GAME THEORY AND THE ECONOMICS OF COOPERATION • Game theoryis the study of how people behave in strategic situations. • Strategic decisions are those in which each person, in deciding what actions to take, must consider how others might respond to that action.

GAME THEORY AND THE ECONOMICS OF COOPERATION • Because the number of firms in an oligopolistic market is small, each firm must act strategically. • Each firm knows that its profit depends not only on how much it produces but also on how much the other firms produce.

The Prisoners’ Dilemma • The prisoners’ dilemma provides insight into the difficulty in maintaining cooperation. • Often people (firms) fail to cooperate with one another even when cooperation would make them better off.

The Prisoners’ Dilemma • The prisoners’ dilemma is a particular “game” between two captured prisoners that illustrates why cooperation is difficult to maintain even when it is mutually beneficial.

Nisit gets 8 years Nisit gets 20 years Dom gets 8 years Dom goes free Nisit goes free Nisit gets 1 year Dom gets 20 years Dom gets 1 year The Prisoners’ Dilemma Nisit’ s Decision Confess Remain Silent Confess Dom’s Decision Remain Silent

Oligopolies as a Prisoners’ Dilemma • The dominant strategy is the best strategy for a player to follow regardless of the strategies chosen by the other players. • Cooperation is difficult to maintain, because cooperation is not in the best interest of the individual player.

WU gets $1,500 profit WU gets $1,600 profit MKC gets $2,000 profit MKC gets $1,600 profit WU gets $2,000 profit WU gets $1,800 profit MKC gets $1,500 profit MKC gets $1,800 profit Figure shows Warm Up and Monkey Club play Oligopoly Game Warm Up 350 person 300 person 350 person Monkey ‘s Club 300 person