Download

1 / 28

280 likes | 464 Views

Chapter 15 Dividends. Background. Dividends as a Basis for Value Dividends are important in determining stock value Individual investors buy stocks expecting dividends and price appreciation

E N D

Background • Dividends as a Basis for Value • Dividends are important in determining stock value • Individual investors buy stocks expecting dividends and price appreciation • From the whole market view, today’s stock price is the present value of an infinite stream of dividends • Focus on the individual view

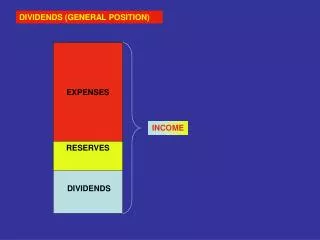

Understanding the Dividend Decision • The Discretionary Nature of Dividends • Board of Directors determines the dividend • Can be more than earnings or nothing • The Dividend Decision • Whether to pay cash dividends or retain earnings for growth • Current income • Deferred income

The Dividend Controversy • Does paying or not paying dividends affect stock price? • Do stockholders prefer current or deferred income? • Three arguments regarding investors’ preferences for or against dividends • Dividend Irrelevance • Dividend Preference • Dividend Aversion

Dividend Irrelevance • Most theorists say dividends matter very little to stock price • Value of eliminated early dividends is offset by growth-created value in the future • In valuation equation loss of D1, D2 …. is made up by gains in later Di (i = 1, 2,…n) and Pn

Concept Connection Example 15-3 Tailoring the Income Stream The Winters are retirees with most of their savings invested in 10,000 shares of Ajax Corporation (AJAX). AJAX sells for $10 per share and pays an annual dividend of $0.50 per share. This year AJAX eliminated the dividend, but began to grow at 5% a year due to the reinvested earnings. How can the Winters maintain their income and their position in AJAX?

Concept Connection Example 15-3 Tailoring the Income Stream Original value of the Winters’ AJAX shares $10 10,000 shares = $100,000. Eliminated dividend 10,000 shares $0.50 = $5,000. After one year of 5% growth, AJAX should sell for $10 × 1.05 = $10.50. To maintain their income the Winters must sell $5,000 $10.50 = 476shares After which they would have 10,000 – 476 = 9,524 shares Worth $10.50 x 9,524 = $100,002.

Dividend Irrelevance • Transaction costs • The more significant the transactions costs, the less valid the irrelevance theory becomes • Income taxes • Dividends are taxed as ordinary income • Appreciation is taxed as a capital gain • The View from Within the Company • Dividends represent a cash outflow • Firms prefer not paying dividends if it avoids selling new stock

Dividend Preference • Investors prefer immediate cash to uncertain future benefits • Poor management may waste the funds rather than using effectively for growth • Inconsistency in theory: • If investors are worried about management not using resources effectively, why did they invest in the firm in the first place?

Dividend Aversion • Investors prefer future capital gains to current dividends because of tax rates • Price appreciation taxed as capital gain • Dividends taxed as ordinary income • Argument hinges on current tax rates on dividend income vs. capital gains income • Capital gains taxes are not paid until stock is sold so taxes are deferred

Other Theories and Ideas • The Clientele Effect • Investors choose stocks for dividend policy so any change in payments policy is disruptive • The Residual Dividend Theory • Dividends are paid from earnings only after viable projects are funded • The Signaling Effect of Dividends • Cash dividends signal management’s confidence • The Expectations Theory • A refinement of the signaling effect • Dividends that fail to fulfill stockholders’ expectations send a negative message even if the payment is good

Legal and Contractual Restrictions on Dividends Legal Restrictions • Dividends can’t be paid out of contributed capital – must come from retained earnings • Insolvent firms can’t pay dividends Contractual Restrictions • Loan indentures and covenants may limit dividend payments to protect creditors’ interests • Cumulative feature of preferred stock limits dividend payments

Dividend Policy • Dividend policy: Rationale for determining dividend payouts • Payout ratio • States dividends as a fraction of earnings • Stability • The constancy of dividends over time • A stable dividend is non-decreasing • A dividend with a stable growth rate increases at a fairly constant growth rate

Alternate Policies • Target Payout Ratio • Firm selects a long-run target payout ratio • Stable Dividends Per Share • A constant dividend is paid regardless of earnings • Small Regular Dividend with a Year-End Extra if Earnings Permit • An effort to avoid the signaling effect

The Mechanics of Dividend Payments • Each quarterly dividend has key dates: • Declaration Date: Date the board authorizes the dividend • Date of Record: Date by which you must be an owner to receive the dividend • Payment Date: Date on which the dividend will actually be paid – check in the mail • Ex-Dividend Date: Date from which new stock buyers no longer receive the dividend

Dividend Reinvestment Plans • Large companies offer automatic dividend reinvestment plans (DRIPs) to stockholders • Instead of receiving cash dividends, the stockholder receives additional shares • The payment is taxable • Don’t confuse with stock dividend

Stock Splits and Dividends • Stock Split • Stockholders issued new shares in proportion to current holdings • No change in proportionate ownership of company • Reverse splits also possible • Stock Dividend • Similar to stock split • Called a stock dividend if the number of new shares is less than or equal to 20% of previously outstanding shares

Rationale for Stock Splits and Stock Dividends Stock Split • Trading Range Argument for splits • Splits keep stock prices in a trading range: accessible to small investors • Stock usually split when prices are increasing • May give false impression that price increase is from split Stock Dividend • Giving Something that Doesn’t Cost Anything • Stock dividends are an attempt at signaling • Employed to send a positive message • Doesn’t really give shareholders anything

Effect On Price And Value • Splits and stock dividends increase shares outstanding without changing economic value of the underlying company • Have no real economic effect

Stock Repurchases • Alternative to Dividend • Firms with cash on hand can pay dividends or repurchase their own stock • Repurchase reduces the number of shares outstanding and increases EPS • Remaining shares will increase in value if the market maintains the P/E ratio after the repurchase

Concept Connection Example 15-6 Stock Repurchases The Johnson Company has 2,500,000 shares of common stock outstanding, net income of $5 million, and a P/E ratio of 10. EPS = $5,000,000 / 2,500,000 = $2.00 per share; Market price = $2.00 x 10 = $20. Johnson has $1 million in cash to distribute to stockholders. • Per share dividend $1,000,000 / 2,500,000 = $0.40 per share • If Johnson repurchases shares instead it will retire $1,000,000 / $20 = 50,000 shares leaving 2,450,000 shares outstanding

Stock Repurchases • The new EPS will be • $5,000,000 / 2,450,000 = $2.04 per share. • If the P/E ratio remains unchanged, the stock price will be $2.04 x 10 = $20.40 A price appreciation equal to the dividend

Stock Repurchases • Methods of Repurchasing Shares • Buy on open market – easiest method • Tender offer – buy shares at a set price offered to interested stockholders • Negotiated deal – buy from a large investor who owns a block of stock

Other Repurchase Issues • Opportunistic Repurchase • Stock is temporarily undervalued • Repurchase to Dispose of Excess Cash • Distributes cash without a signaling effect

Other Repurchase Issues • Taxes • Occasional stock repurchases can benefit stockholders because capital gains tax rates may be lower than ordinary rates • Repurchases to Restructure Capital • Borrowing money to repurchase stock raises leverage level and debt ratio