Download

1 / 24

770 likes | 1.42k Views

Chapter 4 Process Costing. Both systems assign material, labor and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use the same manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods.

E N D

Both systems assign material, labor and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use the same manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods. The flow of costs through the manufacturing accounts is basically the same in both systems. Similarities Between Job-Order and Process Costing

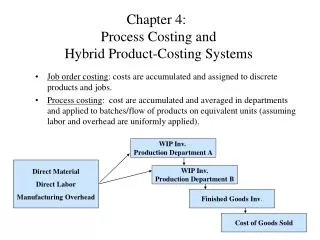

Process costing is used when a single product is produced on a continuing basis or for a long period of time. Job-order costing is used when many different jobs having different production requirements are worked on each period. Process costing systems accumulate costs by department. Job-order costing systems accumulated costs by individual jobs. Process costing systems compute unit costs by department. Job-order costing systems compute unit costs by job on the job cost sheet. Differences Between Job-Order and Process Costing

Process Costing and Direct Labor DirectMaterials Direct labor costsmay be smallin comparison toother product costs in processcost systems. Mfg. Ovhd. Dollar Amount DirectLabor Type of Product Cost

Process Costing and Direct Labor DirectMaterials Direct labor costsmay be smallin comparison toother product costs in processcost systems. Conversion Dollar Amount Type of Product Cost Direct labor and manufacturing overhead may becombined into one product cost called conversion.

Example A – JanuaryNo Beginning/No Ending Inventory Work in process, January 1: 0 units Manufacturing Costs in Beginning Inventory: $0 Production started during January: 1,000 units Production completed during January: 1,000 units Costs added to production in January: $50,000 Work in process, January 31: 0 units Manufacturing Costs in Ending Inventory: $0 Manufacturing Costs transferred out in January: ?

Example A – FebruaryNo Beginning/Some Ending Inventory Work in process, February 1: 0 units Manufacturing Costs in Beginning Inventory: $0 Production started during February: 1,000 units Production completed during February: 800 units Costs added to production in February $45,000 Work in process, February 28 (50% complete): 200 units Manufacturing Costs in Ending Inventory: ? Manufacturing Costs transferred out in February: ?

Equivalent Units of Production Equivalent units are the product of the number of partially completed units and the percentage completion of those units. Partially completed units are thus expressed in terms of a smaller number of fully completed units

+ = 1 Equivalent Units of Production Two half completed products are equivalent to one completed product. So, 10,000 units 70 percent completeare equivalent to 7,000 complete units.

Quick Check For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period? a. 10,000 b. 11,500 c. 13,500 d. 15,000

Calculating and Using Equivalent Units of Production To calculate the cost perequivalent unit for the period: Cost perequivalent unit Costs for the periodEquivalent units of productionfor the period =

Quick Check Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period? a. $1.84 b. $2.40 c. $2.76 d. $2.90

Example A – MarchSome Beginning/Some Ending Inventory Work in process, March 1 (50% complete): 200 units Manufacturing Costs in Beginning Inventory: $5,000 Production started during March: 1,500 units Production completed during March: 1,200 units Costs added to production in March $65,000 Work in process, March 31 (40% complete): 500 units Manufacturing Costs in Ending Inventory: ? Manufacturing Costs transferred out in March: ?

Equivalent Units of ProductionWeighted-Average Method The weighted-average method . . . Blends together costs from prior and current periods. Determines equivalent units of production for a department by adding together the number of units transferred out plus the equivalent units in ending Work in Process Inventory. Ignores percentage completion of the Beginning Inventory

Weighted-Average Method • For each category of cost (material and conversion) in each processing department the following calculations are made:

Production Report Example • Double Diamond Skis uses process costing to determine unit costs in its Shaping and Milling Department. • Double Diamond uses the weighted average cost procedure. • Using the following information for the month of May, let’s prepare a production report for Shaping and Milling.

Production Report Example Work in process, May 1: 200 units Materials: 55% complete $ 9,600 Conversion: 30% complete 5,575 Production started during May: 5,000 units Production completed during May: 4,800 units Costs added to production in May: Materials cost $ 368,600 Conversion cost 350,900 Work in process, May 31: 400 units Materials 40% complete Conversion 25% complete Manufacturing Costs in Ending Inventory: ? Manufacturing Costs transferred out in May: ?

Production Report Example Section 1: Quantity Schedule with Equivalent Units

Production Report Example Section 2: Compute cost per equivalent unit

Production Report Example Section 3: Cost Reconciliation 4,800 units @ $149.00

Production Report Example Section 3: Cost Reconciliation 160 units @ $76.25 100 units @ $72.75 All costs accounted for