Download

1 / 14

140 likes | 274 Views

BANKING AND FINANCIAL REFORM IN CHINA Howard Davies. CHINA HAS FOUR INTER-RELATED “NIGHTMARES”. Inefficient SOEs losing money and being forced to close or borrow from the banks Banks being technically bankrupt because of the bad loans made to state enterprises

E N D

BANKING AND FINANCIAL REFORM IN CHINA Howard Davies

CHINA HAS FOUR INTER-RELATED “NIGHTMARES” • Inefficient SOEs losing money and being forced to close • or borrow from the banks • Banks being technically bankrupt because of the bad • loans made to state enterprises • Loose credit stimulating inflation (in the mid-1990s) • Mass unemployment could result from rapid closure of • SOEs.

OBJECTIVES • To outline the major features of the Chinese banking • system before reform • To identify the problems associated with such a system • To examine the purpose of banking reform • To examine the changes which have taken place • To review the current situation

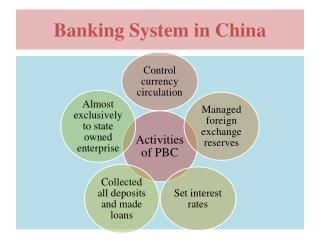

The Chinese Banking System Before Reform • A mono-bank system: the People’s Bank of China • controlled the other banks, with the Ministry of • Finance as the responsible authority • Banks “gave” funds to enterprises in support of the • production plan • - non-repayable grants • - low-interest or no-interest loans to priority industries • - no consideration of efficiency in the use of scarce • capital

Problems with That System? • Banks are passive funds providers • No conservation of scarce resources • No “financial intermediation” • Source of the “soft budget constraint” • PBoC unable to monitor performance of industries • controlled by powerful Ministries • Limited tools for macro-economic control • THE BANKING SYSTEM DID NOT FULFIL • THE ROLE WHICH IT HAS IN MARKET ECONOMIES

Purpose of Banking Reform? • Re-establish financial intermediation - those who wish to • lend linked to those who wish to borrow • Force enterprises to become more efficient - harden the • budget constraint • Facilitate foreign trade and investment - provide FIEs with • the banking facilities they expect • Provide tools for macro-economic control - interest rates, • credit conditions instead of rationing

MAJOR CHANGES MADE I • Establishment or re-instatement of “specialised • commercials banks” • - Bank of China - foreign trade and exchange (1979) • - Agriculture Bank of China (1979) • - People’s Construction Bank (1979) • - China International Trust and Investment Company • (CITIC, 1979)

MAJOR CHANGES MADE II • 1984 - People’s Bank of China becomes the central bank • and the Industrial and Commercial Bank takes over its • ordinary banking operations • A major proliferation of regional level development banks, • industrial banks, housing savings banks, trust companies, • finance companies, leasing companies, credit co-operatives • Huge growth of loans and deposits - 20 + % p.a.

Problems With The Developing New System? • Difficult to control money and credit • Growth of speculative activities by banks (failure of GITIC • 1999) • Banks dependent on PBoC for funds • Banks under-capitalised (8% is the BIS norm) • Non-performing loans (20% completely irrecoverable, plus • 50% to be written off?) • SOE losses still have to be funded • “Triangular” debt problem

How Did This Happen? • Poorly defined contractual relationships between • government, banks and enterprises • Soft budget constraints at both levels - banks and • enterprises • Poor accounting practices

What Is Being Done? • 1994 - establishment of three “policy banks” to take • “soft-funding” responsibility away from specialised banks • - State Development Bank • . for Infra-structure and finance for priority industries • - Import-Export Bank • . for finance of equipment import for up-grading industries • - Agricultural Development Bank • . to fund state procurement of agricultural products at • market prices

How Is That Being Built On? • 1995 - Central Banking Law and Commercial Banking • Law • Commercial banks restricted to be banking business • Banks should lend against collateral and on the viability • of projects • Non-policy banks to become more commercial • - more autonomy • - more accountable/greater incentives • - more rational price for credit • - harden budget constraints for both banks and enterprises

What Are the Remaining Problems? • Banks may be too large to fail (but GITIC?) - threats not • credible • Bankruptcies only implemented on a limited scale • State Council can still demand that loans are made • Difficult to distinguish between policy loans and • commercial loans • Banks still under-capitalised • SOEs still making losses • Development banks and ITICs may have been making • even worse lending decisions as better banks develop

The Current Situation? • Collapsing ITCs raises the question “how many will be • allowed to fail?” • Powerful interests could lose from full commercialisation • Full commercialisation could lead to explosive • unemployment • FEELING FOR THE STONES, NOT GRASPING THE • NETTLE, WHICH MAY BE WISE • MORE GROWTH NEEDED!