Download

1 / 16

160 likes | 176 Views

This article explores the implications of lending by multinational banks for financial stability and integration. It examines the positive impact on banking efficiency and access to finance, as well as the negative effects on local business and credit cycles. The role of parent support and the transmission of financial shocks across borders are also discussed. The article concludes with a call for a better understanding of the variation between and within multinational banks for more effective supervision.

E N D

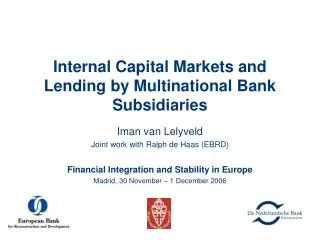

Powerful parents? The dark and the bright side of multinational banking • Ralph De Haas • EBRD Banca d’Italia, June 10th 2013 Lending by multinational banks and implications for financial stability and integration

European banking integration: view from above Source: Bankscope, bank websites

European banking integration: view from the ground Red dots – only domestic banks Blue dots – only foreign banks Green dots – domestic and foreign banks Source: Beck, Degryse, De Haas and Van Horen (2013)

Czech Republic: foreign banks rule Source: Beck, Degryse, De Haas and Van Horen (2013)

Poland: a more mixed picture Source: Beck, Degryse, De Haas and Van Horen (2013)

The bright side of multinational banking • Positive impact on banking efficiency (Fries and Taci 2005) • In the medium term, positive impact on access to finance (Giannetti and Ongena 2012) • More stable than cross-border credit (Peek and Rosengren 2000) • Parental support via internal capital markets (Cetorelli and Goldberg 2012)stabilizes economies during local banking crises (De Haas and Van Lelyveld 2006/2010)

The dark side of multinational banking • Exacerbates local business and credit cycles (Morgan et al. 2004) • Boom in Emerging Europe: 2004-2007 (De Haas, Korniyenko, Loukoianova, and Pivovarsky 2012) • Regional U.S. housing booms (Loutskina and Strahan 2011) • Transmits financial shocks across borders • From Japan to the U.S. (Peek and Rosengren 1997/2000) • From Western to Emerging Europe (Popov and Udell 2010; Ongena, Peydro, Van Horen 2013) • Globally: during 2008/09, MNB subs deleveraged faster than domestic banks, in particular wholesale-funded subsidiaries and subsidiaries of wholesale-funded parents (De Haas and Van Lelyveld 2013)

Some things we learned • Multinational banking: double-edged sword • Why? ICMs are two-way streets • Substitution and support effects • Composition debt funding matters • ‘Sticky’ (insured) retail vs. ‘flighty’ wholesale (Kamil and Rai 2011) • FX vs. LC wholesale funding: swap markets can break down(Ivashina, Scharfstein, and Stein 2013)

Variation across multinational banks? • Large literature on differences between domestic and foreign banks (Claessens and Van Horen 2013) • We know less about differences between and within multinational banks in terms of funding and business models • Banking Environment and Performance Survey (BEPS II) • Detailed face-to-face surveys with >600 bank CEOs across 32 EBRD countries of operation • Quantitative follow-up surveys filled out by >300 of these banks • Collection of detailed information on the geographical location of 137,575 bank branches owned by 1,840 banks

ICMs as two-way streets Source: De Haas and Kirschenmann, 2013

Powerful parents: credit-growth drivers Source: De Haas and Kirschenmann, 2013

Push for market share Source: De Haas and Kirschenmann, 2013

Use of centralised Treasuries Source: De Haas and Kirschenmann, 2013

Business models matter... Source: De Haas and Kirschenmann, 2013

Open questions • What explains variation between and within MNBs? • Business models (“the Spanish model”) vs. host-country conditions (Latin America vs. Emerging Europe)? • Role “traditional” ICM (liquidity and dividend flows) vs. economic capital allocation and credit growth/market share target-setting • Centralised vs. decentralised risk management • Homogeneous branches vs. heterogeneous subsidiaries A better understanding of this variation is particularly important for (tailor-made) supervision rather than (broad-brushed) regulation