Download

1 / 16

160 likes | 172 Views

Explore the components, functions, and impact of the financial system in an international context. Learn about intermediaries, institutions, liquidity, and risk management.

E N D

Financial Markets: International Context:MN10403 Semester 2, 2009/10 Lecturer: Richard Fairchild.

Introduction to the Financial System • The components of the Financial System. • What a Financial System Does. • Financial Intermediaries. • The key features of financial markets. • The users of the system, and the benefits they receive.

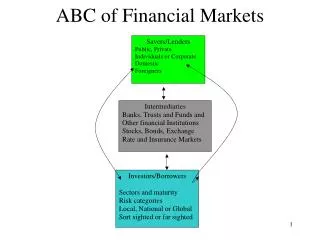

Financial System • A set of markets. • Individuals and institutions trading in those markets. • Supervisory bodies responsible for regulation (eg FSA). • End-users: People and Firms wishing to borrow and lend.

Borrowers and Lenders • Deal directly with each other. • Trade in organised markets => • Lenders buy liabilities issued by borrowers. • Newly issued liability: issuer (borrower) receives funds directly from lender. • Or a lender will buy an existing liability from another lender => secondary transaction.

Intermediaries • Alternatively, borrowers and lenders may trade with each other through institutions or intermediaries. • Lender has a non-tradable asset (eg bank or building society account) • Intermediaries create liabilities: loans to borrowers • Intermediaries also trade in markets: issuing and buying securities

Function of financial system • Helping funds flow from lenders to borrowers. • Other functions: • Means of making payments. • Insuring risk-averse individuals. • Cheap and efficient way for investors to re-arrange their portfolios.

Financial System and economic growth • Efficient borrowing and lending makes it easier for firms to raise finance and invest in economic growth. • Efficient payment system encourages trade and exchange. • Quantity of money in circulation => aggregate demand (to be examined later).

Increasing complexity in financial decision-making. • Lots of new financial products (financial innovation). • =>Increased asymmetric information and moral hazard. • =>Increased number of scandals • => Increase in Financial Regulation.

Financial Institutions as firms. • Financial Institutions can be analysed using Economist’s “theory of the firm.” • Productive firm using inputs to produce outputs. • Financial firm borrows from customers, and lends the money out: they create liquidity. • Assumption: profit-maximisers: charging interest to borrowers higher than that paid to lenders.

Financial Institutions as Intermediaries. • Intermediation: Go-between between borrowers and lenders. • Surplus sectors or units => deficit sectors or units • Financial Intermediaries Create assets for savers/liabilities for borrowers more efficiently than if the parties had to deal with each other directly: eg mortgage on a house.

Creation of assets and liabilities • Financial Intermediation => • More assets and liabilities than under direct lending alone. • And lending and borrowing have become easier => lower transactions costs of lending and borrowing. • Financial intermediaries are able to manage risk more efficiently than individuals.

Economics concept • For any given interest rate, the equilibrium level of borrowing and lending will be higher with financial intermedation.

Liquidity • Speed and convenience with which an asset can be converted into money of a certain value. • Under financial intermediation, lenders can recall their loan more quickly and with greater certainty. • Liquidity: 3 dimensions: time, risk, and cost.

Maturity transformation • Intermediaries must satisfy conflicting needs of borrowers and lenders. • Maturity transformation. • Accept deposits of a given maturity, transform them into loans of a much different maturity. • Eg: building societies: accept deposits of a short maturity (liability): lend them to house buyers up to 25 years (asset).

Maturity Transformation • How can financial intermediaries do this safely (ie lending money on for a long period, when the lenders may want their money back at short notice)? • Size. • => large number of depositors => statistically, net flows will be more stable.

Risk Transformation. • Reduction in risk achieved by diversification of lending and by screening of borrowers. • Risk reduction. • Default risk. • Capital risk. • Income risk.