Download

1 / 40

410 likes | 660 Views

Monetary Theory and Policy. Demand and supply of money The supply of money and the equilibrium interest rate The monetary transmission mechanism The Quantity theory of money The record of monetary policy. The money market.

E N D

Monetary Theory and Policy • Demand and supply of money • The supply of money and the equilibrium interest rate • The monetary transmission mechanism • The Quantity theory of money • The record of monetary policy

The money market Earlier we said that the interest rate (i) influences aggregate spending—specifically investment and consumption. However, we have yet to develop a theory of the interest rate The interest rate is governed by the demand and supply of money.

Why do agents hold money? To make planned expenditures/payments To be prepared for unexpected expenditures/payments. To store wealth.

The interest rate (i) measuresthe opportunity cost of holding money The higher the interest rate, the more interest I give up by holding my wealth in money-- as opposed to an interest-bearing asset.

Demand for money The money demand, Dm, slopes downward. As the interest rate falls, other things constant, so does the opportunity cost of holding money; the quantity of money demanded increases. Interest rate Dm 0 Quantity of money

The supply of money We assume that the Fed (or central banks generally) determines the supply of money

Because the money supply is determined by the Federal Reserve, it can be represented by a vertical line. b a S’m Sm Interest rate At point a, the intersection of the money supply, Sm, and the money demand, Dm, determines the market interest rate, i. i i’ Following an increase in the money supply to S’m, the quantity of money supplied exceeds the quantity demanded at the original interest rate, i. Dm Quantity of money 0 M M’ People attempt to exchange money for bonds or other financial assets. In doing so, they push down the interest rate to i’, where quantity demanded equals quantity supplied. This new equilibrium occurs at point b. Effect of an increase in the money supply

(c) Aggregate demand (b) Demand for investment (a) Supply and demand for money b b b S’m Sm a a a Interest rate Interest rate Price level i i P i’ i’ Dm AD’ DI AD 0 0 0 Money Real GDP Y I M Y’ I’ M’ Investment An increase in the money supply drives the interest rate down to i'. This sets off the spending multiplier process, so the aggregate output demanded at price level P increases from Y to Y ‘ With the cost of borrowing lower, the amount invested increases from I to I‘. Effects of an increase in the money supply on interest rates, investment, and aggregate demand

Chain of cause and effect M↑→i↓→I↑→AD↑→Y↑

The transmission mechanism Fed open market purchase injects reserves into the banking system Commercial banks, thrifts, etc. expand loans and deposits The money supply increases The equilibrium interest rate decreases Consumption and investment increase Real GDP, employment, and (perhaps ) the price level increase

Potential output At a, the economy is producing less than its potential in the short run, resulting in a contractionary gap of $0.2 trillion. a LRAS Price level b SRAS130 If the Federal Reserve increases the money supply by just the right amount, the aggregate demand curve shifts rightward from AD to AD’. A short-run and long-run equilibrium is established at b, with the pride level at 130 and output at the potential level of $14.0 trillion 130 125 AD’ AD Real GDP (trillions of dollars) 0 13.8 14.0 Contractionary gap Expansionary monetary policy to correct a contractionary gap

Fed "target" rate The FOMC sets a target for the “federal funds” rate, which is the rate that banks charge other banks for “borrowed” reserves.

Rate increased to slow red-hot economy Rate increase to head off inflation Global financial crisis prompts rate cuts Rate cuts to limit impact of mortgage defaults on economy Rate cuts to combat recession Since the early 1990s, the Fed has pursued monetary policy primarily through changes in the federal funds rate, the rate that banks charge one another for borrowing and lending excess reserves overnight. Recent ups and downs in the federal funds rate

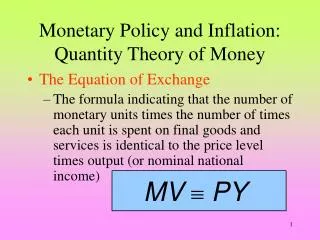

The Equation of Exchange • Where • M is the quantity of money • V is the velocity of circulation • P is the price level • Y is real GDP

What is velocity (V)? Velocity (V) is the average number of times per year a unit of money is spent for new goods and services. Let (P Y) is nominal GDP. Let P = 1.25; Y = $8 trillion; and M= $2 trillion. Thus: Or, V = 5

Money and Aggregate Demand in LR • Velocity depends on • Customs and convention of commerce • Innovations facilitate exchange • Higher velocity • Frequency • The more often workers get paid • Higher velocity • Stability (store of value) • The better store of value • Lower velocity

Equation of Exchange is Always True The equation simply states that what is spent for new goods and services (M V) is equal to the market value of new goods and services produced (P Y).

Illustration Using the numbers on a preceding slide, we can see that and thus

“Monetarist” interpretation of the equation of exchange The monetarists believe that price level changes (hence inflation) can be explained by changes in quantity of money “Inflation is always and everywhere a monetary phenomenon.”

Example Assume that V = 5 and is constant. Y is $8 trillion (also assumed to be constant). Initially, let M = $2 trillion

Our basic equation can be rearranged as follows: Now solve for the price level (P): Now let the money supply increase to $2.4 trillion. Notice that: Thus we have: Notice that:

Hence a 20 percent increase in the money supply causes the price level to increase by 20 percent. Monetarists put the blame for inflation squarely at the doorstep of the monetary authorities (in the U.S., the FED).

Potential output LRAS a b The quantity theory of money predicts that if velocity is stable, then an increase in the supply of money in the long run results in a higher price level, or inflation. Because the long-run aggregate supply curve is fixed, increases in the money supply affect only the price level, not real output. Price level 140 130 AD’ AD Real GDP (trillions of dollars) 0 14.0 In the long run, an increase in the money supply results in a higher price level, or inflation

The velocity of M1 (a) Velocity of M1 M1 velocity fluctuated so much during the 1980s that M1 growth was abandoned as a short-run policy target.

The velocity of M2 (b) Velocity of M2 M2 velocity appears more stable than M1 velocity, but both are now considered by the Fed as too unpredictable for short-run policy use.

Record indicates that nations with high rates of monetary growth also suffer high rates of inflation • A decade of annual inflation and money growth in 85 countries (average annual percent)

An increase in the price level or in real GDP, with velocity stable, shifts rightward the money demand curve from Dm to D'm. e e’ e’’ S’m Sm If the Federal Reserve holds the money supply at Sm, the interest rate rises from i (at point e) to i ' (at point e'). i’ Interest rate Alternatively, the Fed could hold the interest rate constant by increasing the supply of money to S'm. The Fed may choose any point along the money demand curve D'm. i Dm D’m Quantity of money 0 M M’ Targeting interest rate vs. targeting the money supply

The Fed pulled on the string big time beginning in 1979—it was an anti-inflation strategy under Chairman Paul Volcker

Modeling Contractionary Monetary Policy Price Level Potential GDP AS AD2 AD1 0 Y1 Real GDP

Conventional 30 year www.economagic.com

Monthly payments on a $110,000 30 year mortgage note 1 Does not include prorated insurance or property taxes.

Data in thousands of units www.economagic.gov

More recently, the Fed raised the federal funds rate six times between May 1999 and May 2000—from 4.75% to 6.5 %. Evidently unemployment was getting “too low.”

The FOMC reversed course in July 2000 and cut the funds rate 17 times, to a low of 1.00 percent in July 2003.

Inflation Monster Beginning in 2004, and until summer of 2007, the FED was mainly concerned about inflation.