Download

1 / 20

210 likes | 438 Views

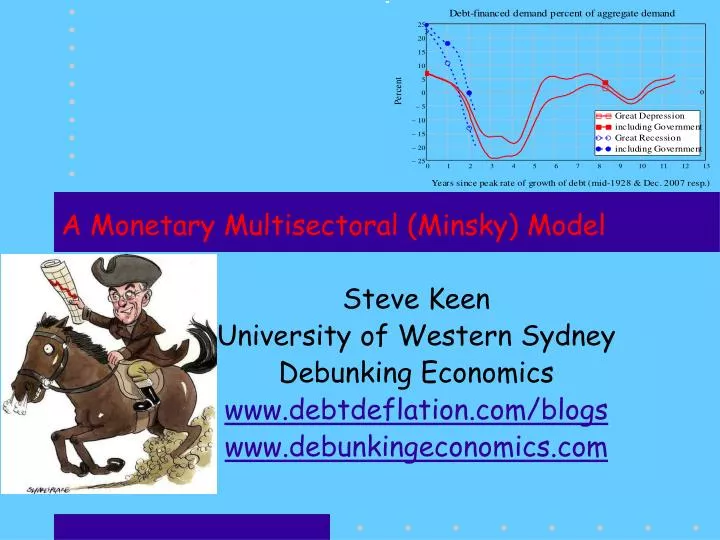

A Monetary Multisectoral (Minsky) Model. Steve Keen University of Western Sydney Debunking Economics www.debtdeflation.com/blogs www.debunkingeconomics.com. The Bankruptcy of Neoclassical Economics. Before the crisis…

E N D

A Monetary Multisectoral (Minsky) Model Steve Keen University of Western Sydney Debunking Economics www.debtdeflation.com/blogs www.debunkingeconomics.com

The Bankruptcy of Neoclassical Economics • Before the crisis… • The state of macro is good…” (Oliver Blanchard: founding editor, AER: Macro) • After the crisis… • It is important to start by stating the obvious, namely, that the baby should not be thrown out with the bathwater…” (Blanchard Dell'Ariccia et al. 2010; emphasis added) • Reality • Neoclassical macroeconomics is a baby that should never have been conceived

The Bankruptcy of Neoclassical Economics • Neoclassical theory wrong from first principles: • Treats complex monetary exchange as barter • Assumes macroeconomy is stable • Ignores social class • Treats entire economy a single agent • Obliterates uncertainty • “Rational” as capacity to foresee the future; • Uses empirically falsified “money multiplier” model of money creation; and • Ignores credit and debt.

A tentative, but not-bankrupt, alternative • A new macroeconomics must do the exact opposite: • Economy as inherently monetary; • Model the economy dynamically; • Social classes rather than isolated agents; • Rational but not prophetic behavior; • Endogenous creation of money by banking sector; and • Credit and Debt have pivotal roles • Two instances • Monetary Minsky Great Moderation/Recession model • Dynamic Monetary Multisectoral model • Base models: • Monetary Circuit Theory (Graziani 1989; Keen 2008) • Goodwin Growth Cycle (Goodwin 1967)

Monetary Circuit Theory • Basic process of endogenous money creation • Entrepreneur approaches bank for loan • Bank grants loan & creates deposit simultaneously • Alan Holmes, Senior Vice-President New York Fed, 1969: • “In the real world, banks extend credit, creating deposits in the process, and look for the reserves later.” (1969, p. 73) Assets Liabilities • New loan puts additional spending power into circulation • Modeling this using strictly monetary framework:

Monetary Circuit Theory • Input financial relations in matrix: • Symbolic derivation of system of coupled ordinary differential equations

Monetary Circuit Theory • Symbolic substitutions generate model

Goodwin Growth Cycle model • Inherently cyclical growth (Goodwin 1967, Blatt 1983) • Capital K determines output Y via the accelerator: • Y determines employment L via productivity a: • L determines employment rate l via population N: • l determines rate of change of wages w via Phillips Curve • Integral of w determines W (given initial value) • Y-W determines profits P and thus Investment I… • Closes the loop:

Explicit Monetary Minsky Model • Coupled with Goodwin model to yield final system

Explicit Monetary Minsky Model • Single sector model (not yet calibrated to data) can generate “Great Moderation and Great Recession”

Multi-sectoral extension • Stylized version of monetary flows table:

Multi-sectoral extension • Profit now net of intersectoral input purchases: • Each sector modeled as Goodwin cycle • Financial flows matrix captures intersectoral dependencies

Multi-sectoral extension • “Conjecture: The repeated development of an unstable state of the economy is … an unavoidable consequence of, the local instability of the state of balanced growth.” (Blatt 1983, p. 161)

Multi-sectoral extension • “The usual image of the business cycle was of a wavelike movement, and the waves of the sea were the accepted metaphor… The reality in the nineteenth and early twentieth centuries was, in fact, much closer to the teeth of a ripsaw which go up on a gradual plane on one side and drop precipitately on the other…” (Galbraith 1975, p. 104)

Multi-sectoral extension • Model fundamentally monetary: physical cycles cause and caused by cycles in finance

Addendum: Reforming economic education • Making real dynamics sexy & accessible • Free prototype QED “Quesnay Economic Dynamics” • Inspired by Godley SAM approach • Extended to continuous time • Ideally suited to financial flows

Explicit Monetary Minsky Model • Freely available at www.debtdeflation.com/blogs/qed • Advanced versions under development • Mathematica version for arbitrary number of sectors available soon • New economic dynamic monetary modeling program “Minsky” available by early 2012

Conclusion: Kuznets was correct… • According to … modern followers [of past economists], static economics is a direct stepping stone to the dynamic system… • According to other economists, the body of economic theory must be cardinally rebuilt, if dynamic problems are to be discussed efficiently… • … as long as static economics will remain a strictly unified system based upon the concept of equilibrium, … its analytic part will remain of little use to any system of dynamic economics… • the static scheme in its entirety, in the essence of its approach, is neither a basis, nor a stepping stone towards a proper discussion of dynamic problems. Kuznets, S. (1930, pp. 422-428, 435-436; emphasis added)

References • Bezemer, D. J. (2009). ““No One Saw This Coming”: Understanding Financial Crisis Through Accounting Models.” Groningen, The Netherlands, Faculty of Economics University of Groningen. • Blatt, J. M. (1983). Dynamic economic systems : a post-Keynesian approach. Armonk, N.Y, M.E. Sharpe. • Bezemer, D. J. (2010). "Understanding financial crisis through accounting models." Accounting, Organizations and Society35(7): 676-688. • Biggs, M., T. Mayer, et al. (2010). "Credit and Economic Recovery: Demystifying Phoenix Miracles." SSRN eLibrary. • Blanchard, O., G. Dell'Ariccia, et al. (2010). "Rethinking Macroeconomic Policy." Journal of Money, Credit, and Banking 42: 199-215. • Goodwin, R. (1967). A growth cycle. Socialism, Capitalism and Economic Growth. C. H. Feinstein. Cambridge, Cambridge University Press: 54-58. • Graziani, A. (1989). "The Theory of the Monetary Circuit." Thames Papers in Political Economy Spring: 1-26. • Holmes, A. R. (1969). Operational Constraints on the Stabilization of Money Supply Growth. Controlling Monetary Aggregates. F. E. Morris. Nantucket Island, The Federal Reserve Bank of Boston: 65-77.

References • Keen, S. (1995). "Finance and Economic Breakdown: Modeling Minsky's 'Financial Instability Hypothesis.'." Journal of Post Keynesian Economics17(4): 607-635. • Keen, S. (2008). Keynes’s ‘revolving fund of finance’ and transactions in the circuit. Keynes and Macroeconomics after 70 Years. R. Wray and M. Forstater. Cheltenham, Edward Elgar: 259-278. • Kuznets, S. (1930). "Static and Dynamic Economics." The American Economic Review 20(3): 426-441. • Kydland, F. E. and E. C. Prescott (1990). "Business Cycles: Real Facts and a Monetary Myth." Federal Reserve Bank of Minneapolis Quarterly Review14(2): 3-18. • Minsky, H. P. (1982). Can "it" happen again? : essays on instability and finance. Armonk, N.Y., M.E. Sharpe. • Schumpeter, J. A. (1934). The theory of economic development : an inquiry into profits, capital, credit, interest and the business cycle. Cambridge, Massachusetts, Harvard University Press. • Solow, R. M. (2001) “From Neoclassical Growth Theory to New Classical Macroeconomics”, in J. H. Drèze (ed.), Advances in Macroeconomic Theory. New York, Palgrave • Solow, R. (2008). "The State of Macroeconomics." The Journal of Economic Perspectives22(1): 243-246.