Download

1 / 10

100 likes | 307 Views

MiFID II: I mpact on company financing in Belgium. Jean-Paul SERVAIS Chairman FSMA Chair ESMA Investor Protection & Intermediaries Standing Committee Brussels Exchange Forum 25 April 2014. Overview. Timeline for MiFID II MiFID II impact on (Belgian) markets SME Growth Markets

E N D

MiFID II: Impact on company financing in Belgium • Jean-Paul SERVAIS • Chairman FSMA • Chair ESMA Investor Protection & Intermediaries Standing Committee • Brussels Exchange Forum 25 April 2014

Overview • Timeline for MiFID II • MiFID II impact on (Belgian) markets • SME Growth Markets • Best execution • Recent Belgian reforms to improve access to capital Brussels Exchange Forum

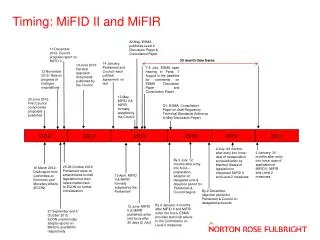

1. Timeline MiFID II/MiFIR (level 1): political agreement on 14 January 2014 vote at the European Parliament on 15 April 2014 Level 2 measures will specify MiFID II/MiFIR (ESMA's consultation papers expected before the summer) MiFID II (levels 1 and 2)/MiFIR: full application expected on1 January 2017 Brussels Exchange Forum

2. MiFID II impact on (Belgian) markets Belgian markets, issuers & investors benefit from the objectives of the MiFID I & II reforms: General objectives of MiFID I & II - Strengthening the integration, liquidity and efficiency of the European financial markets, which contribute to higher execution quality, lower costs, narrower spreads and a lower capital cost, to the advantage of investors and issuers, and indirectly of the European economy - Strong EU position in global competition and consolidation Brussels Exchange Forum

2.MiFID II impact on (Belgian) markets (2) Specific objectives of MiFID II/MiFIR: - enhanced transparency on equity markets, including pan-European consolidation of transparency data - more competition and reduced (post-)trading costs - derivatives reforms aimed at safer and more transparent markets in line with G20 - stricter rules for high frequency trading - other measures to restore investor confidence after the financial crisis - enhanced market integrity by strengthening (enforcement) powers of competent authorities Brussels Exchange Forum

3. SME Growth Markets in MiFID II • MiFID II offers the legal option to create a multilateral trading facility (MTF) dedicated to SMEs, based on pan-European standards • SME under MiFID II = company that has an average market capitalisation of less than EUR 200,000,000 • At least 50% of the issuers on an SME growth market have to be SMEs. The MTF operator has to apply for registration of this SME market with its regulator Brussels Exchange Forum

3. SME Growth Markets in MiFID II (2) • Advantages: - facilitating access to capital - development of specialist markets for SMEs - raise visibility for SMEs • Further ESMA level 2 work to set out common regulatory standards How to deal with companies issuing only bonds? Will bond issuers be taken into account for the 50% criterion? If yes, how? ESMA to consult on several possible alternative options Brussels Exchange Forum

4. Best execution Best execution rules: strengthened on the basis of ESMA advice Execution quality data to be disclosed by execution venues at least annually Top five execution venues (in terms of trading venues) to be disclosed at least annually (for each class of financial instruments) by investment firms Better information to clients about the firm's best execution policy Market transparency and best execution result in modifications to order routing; linked to MiFID's goal of effective competition between trading systems Brussels Exchange Forum

5. Recent Belgian reforms to improve access to capital Abolition of mandatory quarterly reporting & extension of publication deadline for half-yearly reporting Early implementation of directive 2013/50 by Royal Decree of 26 March 2014 in order to: - reduce the administrative burden associated with obligations linked to admission to trading on a regulated market for SMEs, in view of improving their access to capital; - reduce short-term pressure on issuers and give investors an incentive to adopt a longer-term vision. Brussels Exchange Forum

5. Recent Belgian reforms to improve access to capital (2) Crowdfunding: new exemption to the "Prospectus Law" in order to facilitate the launching of certain forms of alternative financing. Each investor is limited to investing a maximum of 1000 Euros in the instruments offered, the total amount of the offer must be less than 300,000 Euros, and all documents relating to the public offer must mention the total amount as well as the maximum amount per investor. FSMA accelerated procedure for approving prospectuses for "plain vanilla" bond offerings(in 2013: 5 out 8 bond offerings took place according to this procedure open to companies subject to ongoing supervision of financial information by the FSMA) Measures to enhance FSMA surveillance and enforcement powers to contribute to market integrity Brussels Exchange Forum