Download

1 / 3

30 likes | 190 Views

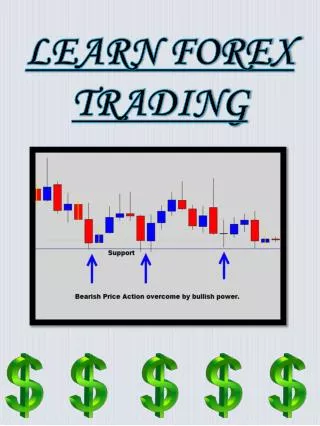

If you are looking forward to saving money or growing your savings account, one of the best ways is by making regular deposits. Once you’ve made up your mind to save money, it is important that you avoid making unnecessary transactions as this will not only debit your savings account, but also diminish your interest returns, which moreover discourages you from building the account. You can even start up with currency trading and start learning more about the financial market.

E N D

4 Budgeting Tips to Grow Your Savings Account Faster You’ve budgeted for food, clothing, bills, mortgage, and loan payments. Now what? What do you do with the extra money in your monthly budget? The simple answer: Save it. Saving money is one of the most effective strategies for developing long-term financial freedom. But it’s easier said than done. Here are four effective ways anyone can start saving and grow their nest egg faster. Make Regular Deposits It might sound simplistic, but regular deposits are critical for growing your savings account. You have to feed your account to help it grow. Here’s how: Start by adding a new line in your monthly budget for savings. Then, set up an automatic transfer from your checking to saving account, or do it each month manually. Either way, it’s important that you make it a bi-weekly or monthly habit. For one, if that money isn’t set aside, you’re much more likely to spend it. Plus, growing your savings over time requires you to develop the “savings habit.”It needs to be a part of your monthly budgeting routine, and regular deposits will help you get in the habit.

Don’t Touch Your Savings After you get in the habit of saving, the next step is avoiding transferring money out. As your savings begins to grow, it’s tempting to want to spend this money. But not touching these funds is absolutely critical to growing your balances over time and earning interest. Regularly debiting your savings account will diminish your interest returns and discourage you from building the account. One strategy you can use is labeling your accounts, whether in your online banking statements or your budgeting apps. For example, you might call your savings account “New Car” or “Retirement.” By doing this, you’ll be less likely to spend the money, because you can visualize the progress you are making. As You Pay Off Debt, Use That Money for Savings Each month, you’ll have scheduled payments for various debts like a credit card or auto loan. As you pay off these debts, continue to budget for them, but put that money directly into your savings account. Your savings will grow at a much faster clip, and you won’t have to find extra money within your budget to do it. Don’t Be Afraid to Invest Building up savings is smart for developing long-term financial freedom, but as you add to your savings account, you can also begin to think about investing a portion of that money. Investing can help you grow your wealth faster, and

enable you to put investment gains into your savings account. As a general rule, you should have six months of expenses on hand. That should be your first goal. But milestone, you can earmark some of these funds for investments. There are many different options, but something as uncomplicated as stock or foreign currency trading can be a quick way to grow your wealth. However, currency trading is a high-risk market, so in- depth knowledge of trading and an understanding of responsibly is essential before starting out. Fortunately, there are great courses that can teach you foreign exchange trading – from companies like Learn to Trade – that will quickly turn you into a master forex trader. once you’ve reached that how to trade Saving money each month can be a challenge, but the hardest part is getting started. Once you develop the habit and start making regular payments, you’ll begin to reap the rewards and be on your way to financial freedom. Presented By Presented By